Mattel 2025 Strategic Analysis: Navigating Cyclical Headwinds Through IP Monetization and Digital Transformation

Date : 2026-03-01

Reading : 767

Mattel is currently navigating a critical, structural transition from a traditional toy manufacturer to a high-margin, IP-driven entertainment platform. While cyclical headwinds and aggressive channel destocking compressed the company’s FY2025 net sales to $5.348 billion (a 1% YoY decline), capturing an estimated 4.4% of the $120.5 billion global toy market, the underlying narrative is one of profound strategic metamorphosis. For corporate strategists and investors, the "so what" lies not in the top-line contraction, but in how Mattel is aggressively reallocating capital toward digital gaming integration, supply chain de-risking, and long-term franchise moats to offset an increasingly concentrated retail landscape.

Figure Mattel 2025 Performance: Pivoting Toward IP-Driven Profitable Growth

Sector Positioning & Top-Line Dynamics

Sector Positioning & Top-Line Dynamics

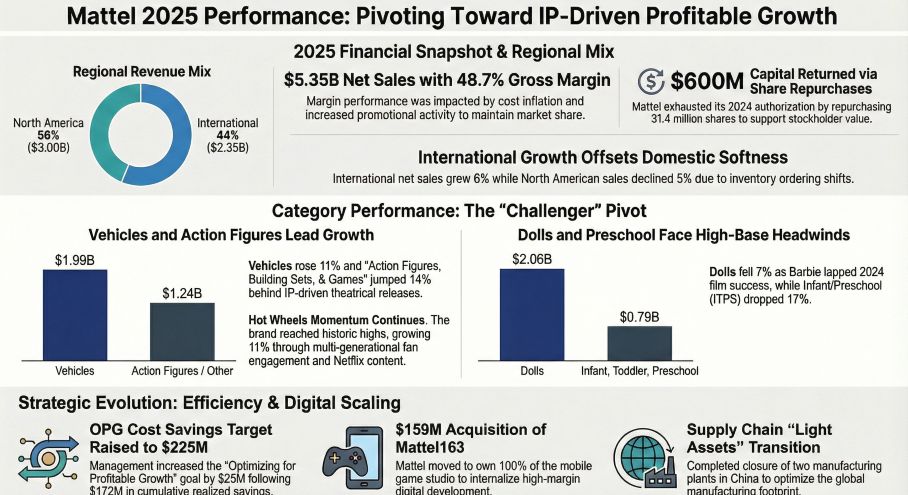

In a maturing global toy industry, sector positioning has shifted from category expansion to intense market share capture. Mattel’s 2025 performance reveals structural bifurcation across its portfolio. While legacy flagship brands like Barbie and Fisher-Price faced an 11% contraction in gross billings due to a high post-movie base effect and maturity challenges, "Challenger" categories provided robust growth engines.

Notably, the Vehicles category (driven by Hot Wheels) and Action Figures surged by 11% and 14%, respectively. Furthermore, the strategic launch of the "Mattel Brick Shop" signals a direct, margin-accretive offensive against LEGO's dominance in the highly loyal, premium adult-fan ("Kidult") segment. As competitors like Hasbro and LEGO aggressively blur the lines between physical and digital play, Mattel’s categorical pivots are vital to defending its market share against the shortening product lifecycles triggered by AI and digital entertainment.

Financial Health & Capital Allocation Efficiency

Mattel’s 2025 financial health reflects a complex tug-of-war between macroeconomic cost inflation and internal optimization. Gross margins shrank by 210 basis points to 48.7%, heavily penalized by a 160 bps hit from retail discounts and promotional allowances, as sales adjustments climbed to 13.7% of net sales.

However, the company's capital allocation efficiency and operational resilience mitigated deeper margin erosion. The "Optimizing for Profitable Growth" (OPG) program delivered a 90 bps positive offset, with management raising the ultimate annual savings target to $225 million by 2026. On the balance sheet, capital allocation remains highly skewed toward supporting EPS via aggressive share repurchases ($606 million in 2025). While this maintains shareholder yield, it sustains a high debt-to-capital ratio of 51%. Operational efficiency indicators, such as Days Sales of Inventory (DSI) and Days Sales Outstanding (DSO) creeping up to 75 days, suggest that supply chain agility remains heavily dictated by the unpredictable ordering patterns of retail giants.

Strategic Moats: Digital Play & IP Monetization

To break the low-margin curse of traditional retail dependency, Mattel is constructing robust strategic moats through content licensing and digital vertical integration. The planned 2026 buyout of the remaining 50% stake in mobile game studio Mattel163 for $159 million is a watershed moment. By internalizing digital R&D, Mattel captures the higher gross margins and recurring revenue streams characteristic of the gaming sector, creating a vital hedge against physical retail volatility.

Furthermore, Mattel is deploying an "IP entertainment platform" model as a financial amplifier. Driven by the recent cinematic success of *Jurassic World* and *Minecraft*, and anticipating the 2026 releases of the *Masters of the Universe* and *Matchbox* films, Mattel is translating singular toy transactions into multi-dimensional royalty streams.

Supply Chain Resilience & Channel Headwinds

A critical vulnerability for Mattel remains its severe retail channel dependency, with Walmart, Target, and Amazon commanding 42% of global net sales. This concentration grants retailers asymmetric bargaining power, forcing Mattel to absorb promotional costs to maintain shelf-space algorithms and visibility.

To counter this and mitigate geopolitical tariff risks, Mattel is executing a radical supply chain restructuring. By systematically reducing its reliance on single-source manufacturing—highlighted by the closure of two Chinese facilities across 2024 and 2025—the company is pivoting toward a decentralized footprint across Vietnam, Malaysia, and Mexico. This nearshoring and diversification strategy is essential to buffering the bottom line against policy volatility and global logistics bottlenecks.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Mattel’s 2025 fiscal year as a painful but necessary period of operational triage. The company possesses undeniable IP moats, but its short-term profitability is constrained by the sheer bargaining power of downstream retail oligopolies and a bloated inventory cycle.

The true test of Mattel’s "Brand-centric strategy" will materialize in 2026. If the full consolidation of Mattel163 and the impending cinematic releases can successfully drive high-margin direct-to-consumer (DTC) engagement, Mattel will successfully decouple its profit engine from traditional retail shelf wars. However, investors must monitor the ongoing inventory bloat; supply chain diversification must eventually translate into accelerated inventory turnover, not just isolated cost-saving metrics.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Mattel 2025 Performance: Pivoting Toward IP-Driven Profitable Growth

Sector Positioning & Top-Line DynamicsIn a maturing global toy industry, sector positioning has shifted from category expansion to intense market share capture. Mattel’s 2025 performance reveals structural bifurcation across its portfolio. While legacy flagship brands like Barbie and Fisher-Price faced an 11% contraction in gross billings due to a high post-movie base effect and maturity challenges, "Challenger" categories provided robust growth engines.

Notably, the Vehicles category (driven by Hot Wheels) and Action Figures surged by 11% and 14%, respectively. Furthermore, the strategic launch of the "Mattel Brick Shop" signals a direct, margin-accretive offensive against LEGO's dominance in the highly loyal, premium adult-fan ("Kidult") segment. As competitors like Hasbro and LEGO aggressively blur the lines between physical and digital play, Mattel’s categorical pivots are vital to defending its market share against the shortening product lifecycles triggered by AI and digital entertainment.

Financial Health & Capital Allocation Efficiency

Mattel’s 2025 financial health reflects a complex tug-of-war between macroeconomic cost inflation and internal optimization. Gross margins shrank by 210 basis points to 48.7%, heavily penalized by a 160 bps hit from retail discounts and promotional allowances, as sales adjustments climbed to 13.7% of net sales.

However, the company's capital allocation efficiency and operational resilience mitigated deeper margin erosion. The "Optimizing for Profitable Growth" (OPG) program delivered a 90 bps positive offset, with management raising the ultimate annual savings target to $225 million by 2026. On the balance sheet, capital allocation remains highly skewed toward supporting EPS via aggressive share repurchases ($606 million in 2025). While this maintains shareholder yield, it sustains a high debt-to-capital ratio of 51%. Operational efficiency indicators, such as Days Sales of Inventory (DSI) and Days Sales Outstanding (DSO) creeping up to 75 days, suggest that supply chain agility remains heavily dictated by the unpredictable ordering patterns of retail giants.

Strategic Moats: Digital Play & IP Monetization

To break the low-margin curse of traditional retail dependency, Mattel is constructing robust strategic moats through content licensing and digital vertical integration. The planned 2026 buyout of the remaining 50% stake in mobile game studio Mattel163 for $159 million is a watershed moment. By internalizing digital R&D, Mattel captures the higher gross margins and recurring revenue streams characteristic of the gaming sector, creating a vital hedge against physical retail volatility.

Furthermore, Mattel is deploying an "IP entertainment platform" model as a financial amplifier. Driven by the recent cinematic success of *Jurassic World* and *Minecraft*, and anticipating the 2026 releases of the *Masters of the Universe* and *Matchbox* films, Mattel is translating singular toy transactions into multi-dimensional royalty streams.

Supply Chain Resilience & Channel Headwinds

A critical vulnerability for Mattel remains its severe retail channel dependency, with Walmart, Target, and Amazon commanding 42% of global net sales. This concentration grants retailers asymmetric bargaining power, forcing Mattel to absorb promotional costs to maintain shelf-space algorithms and visibility.

To counter this and mitigate geopolitical tariff risks, Mattel is executing a radical supply chain restructuring. By systematically reducing its reliance on single-source manufacturing—highlighted by the closure of two Chinese facilities across 2024 and 2025—the company is pivoting toward a decentralized footprint across Vietnam, Malaysia, and Mexico. This nearshoring and diversification strategy is essential to buffering the bottom line against policy volatility and global logistics bottlenecks.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Mattel’s 2025 fiscal year as a painful but necessary period of operational triage. The company possesses undeniable IP moats, but its short-term profitability is constrained by the sheer bargaining power of downstream retail oligopolies and a bloated inventory cycle.

The true test of Mattel’s "Brand-centric strategy" will materialize in 2026. If the full consolidation of Mattel163 and the impending cinematic releases can successfully drive high-margin direct-to-consumer (DTC) engagement, Mattel will successfully decouple its profit engine from traditional retail shelf wars. However, investors must monitor the ongoing inventory bloat; supply chain diversification must eventually translate into accelerated inventory turnover, not just isolated cost-saving metrics.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com