2025 Global Orthopedic Industry: The Shift from Material Competition to Ecosystem Lock-In

Date : 2026-03-02

Reading : 124

The global orthopedic and spine medical device industry has fundamentally pivoted. Based on comprehensive 2025 financial disclosures, the era of competing solely on the biomechanical merits of standalone implants is over. Today, the core growth logic hinges on "ecosystem lock-in." Driven by digital surgery platforms and the rising demand for value-based care, industry titans are leveraging high-switching-cost ecosystems to defend profit margins against stringent payer policies and macro-economic volatility.

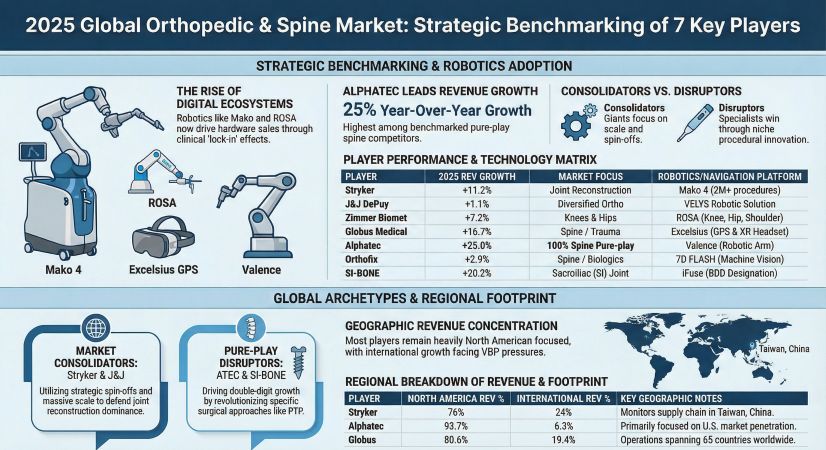

Figure 2025 Global Orthopedic & Spine Market Strategic Benchmarking of 7 Key Players

Strategic Moats: The Digital "Razor and Blade" Model

Strategic Moats: The Digital "Razor and Blade" Model

Leading device manufacturers are no longer just selling hardware; they are commercializing procedural standards. By bundling advanced robotics and navigation platforms with proprietary consumables, companies are forging impenetrable strategic moats.

* The Power of Ecosystem Lock-In: Stryker’s Mako platform remains the industry benchmark. By rolling out the Mako 4 system equipped with Q-Guidance, Stryker has expanded robotic assistance into complex revision surgeries. This capability not only captures a high-margin niche but securely locks hospitals into utilizing Stryker's proprietary implants, driving an 8.5% growth in knee operations and insulating the firm against broader market commoditization.

* Predictive Care and Workflow Efficiency: Alphatec (ATEC) and Globus Medical (GMED) are violently disrupting the spine sector through contrasting paradigms. ATEC is utilizing AI-driven predictive care via its EOS Insight platform to standardize the Prone TransPsoas (PTP) approach, significantly reducing operating room times. Conversely, Globus is building a comprehensive digital cockpit with its ExcelsiusXR augmented reality headsets, ensuring a closed-loop hardware synergy that strictly dictates consumable pull-through.

Cyclical Headwinds: Navigating Payer Pressures and VBP

Despite rapid technological innovation, the industry faces severe cyclical headwinds dictated by global payer policies. Macro ceilings, such as China’s Volume-Based Procurement (VBP) and the U.S. Medicare DRG reforms, are aggressively compressing gross margins.

* Pricing Pressures and Site-of-Care Shifts: Both Johnson & Johnson (J&J) and Zimmer Biomet have reported substantial margin impacts due to VBP-induced price drops and subsequent dealer renegotiations. Furthermore, the migration of elective surgeries from traditional hospitals to Ambulatory Surgical Centers (ASCs) is forcing manufacturers to innovate highly cost-effective, simplified surgical solutions.

* Niche Market Breakthroughs: To bypass these macro ceilings, companies must prove unparalleled clinical value. SI-BONE exemplifies this strategy. By securing a Breakthrough Device Designation (BDD) for its iFuse Bedrock Granite system, SI-BONE has successfully lobbied for Medicare NTAP subsidies. This regulatory moat allows the company to extract premium pricing in the niche sacroiliac joint fusion market, effectively shielding it from the commoditization plaguing major joint replacements.

Capital Allocation Efficiency and M&A Pivots

The financial health of the sector's top seven players reveals a stark divergence in capital allocation efficiency, categorizing the market into cash cows, aggressive consolidators, and high-burn challengers.

* Asset Optimization and Divestitures: Recognizing the drag of low-margin legacy assets, J&J is executing a strategic spin-off of its DePuy Synthes orthopedic branch to aggressively reallocate capital toward high-growth cardiovascular segments. Similarly, Stryker divested its spinal implant business to redirect investments toward high-return digital assets and tuck-in acquisitions, such as the $4.8 billion purchase of Inari Medical.

* Integration Risks and "Growth at All Costs": Globus Medical has scaled rapidly into a musculoskeletal powerhouse via the acquisitions of NuVasive and Nevro. However, its capital allocation efficiency is currently tested by severe integration pains, including potential goodwill impairment risks and a dip in robotic system installations. Meanwhile, specialists like ATEC and Orthofix operate on a "burn for growth" model. ATEC’s SG&A expenses consume over 65% of its revenue, highlighting a critical need to convert robust top-line momentum into self-sustaining free cash flow before highly leveraged balance sheets become a vulnerability.

Sector Positioning: Supply Chain Resilience

In an era of geopolitical friction and inflation, inventory management dictates true operational agility. Zimmer Biomet's heavy reliance on a bulky consignment model—exacerbated by ERP transition failures—highlights the fragility of traditional supply chains. In contrast, Orthofix’s transition toward single-use sterile packaging demonstrates superior asset flexibility, significantly reducing the logistical burdens of instrument turnover and sterilization in an increasingly cost-conscious VBP environment.

HDIN Viewpoint

At HDIN Research, our analysis indicates that the 2025 orthopedic landscape ruthlessly penalizes pure-play hardware vendors while disproportionately rewarding ecosystem architects. Hospital capital expenditure (CAPEX) is tightening; thus, the future belongs to firms capable of transitioning massive upfront robotic costs into SaaS-like or leasing models that guarantee high-margin consumable pull-through. Investors must scrutinize balance sheets for artificially inflated earnings via acquisition accounting and prioritize organizations that utilize AI and clinical data to demonstrably lower surgical revision rates. In the squeeze between VBP and DRG policies, operational efficiency and verifiable clinical evidence are the only remaining levers for premium pricing.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global Orthopedic & Spine Market Strategic Benchmarking of 7 Key Players

Strategic Moats: The Digital "Razor and Blade" ModelLeading device manufacturers are no longer just selling hardware; they are commercializing procedural standards. By bundling advanced robotics and navigation platforms with proprietary consumables, companies are forging impenetrable strategic moats.

* The Power of Ecosystem Lock-In: Stryker’s Mako platform remains the industry benchmark. By rolling out the Mako 4 system equipped with Q-Guidance, Stryker has expanded robotic assistance into complex revision surgeries. This capability not only captures a high-margin niche but securely locks hospitals into utilizing Stryker's proprietary implants, driving an 8.5% growth in knee operations and insulating the firm against broader market commoditization.

* Predictive Care and Workflow Efficiency: Alphatec (ATEC) and Globus Medical (GMED) are violently disrupting the spine sector through contrasting paradigms. ATEC is utilizing AI-driven predictive care via its EOS Insight platform to standardize the Prone TransPsoas (PTP) approach, significantly reducing operating room times. Conversely, Globus is building a comprehensive digital cockpit with its ExcelsiusXR augmented reality headsets, ensuring a closed-loop hardware synergy that strictly dictates consumable pull-through.

Cyclical Headwinds: Navigating Payer Pressures and VBP

Despite rapid technological innovation, the industry faces severe cyclical headwinds dictated by global payer policies. Macro ceilings, such as China’s Volume-Based Procurement (VBP) and the U.S. Medicare DRG reforms, are aggressively compressing gross margins.

* Pricing Pressures and Site-of-Care Shifts: Both Johnson & Johnson (J&J) and Zimmer Biomet have reported substantial margin impacts due to VBP-induced price drops and subsequent dealer renegotiations. Furthermore, the migration of elective surgeries from traditional hospitals to Ambulatory Surgical Centers (ASCs) is forcing manufacturers to innovate highly cost-effective, simplified surgical solutions.

* Niche Market Breakthroughs: To bypass these macro ceilings, companies must prove unparalleled clinical value. SI-BONE exemplifies this strategy. By securing a Breakthrough Device Designation (BDD) for its iFuse Bedrock Granite system, SI-BONE has successfully lobbied for Medicare NTAP subsidies. This regulatory moat allows the company to extract premium pricing in the niche sacroiliac joint fusion market, effectively shielding it from the commoditization plaguing major joint replacements.

Capital Allocation Efficiency and M&A Pivots

The financial health of the sector's top seven players reveals a stark divergence in capital allocation efficiency, categorizing the market into cash cows, aggressive consolidators, and high-burn challengers.

* Asset Optimization and Divestitures: Recognizing the drag of low-margin legacy assets, J&J is executing a strategic spin-off of its DePuy Synthes orthopedic branch to aggressively reallocate capital toward high-growth cardiovascular segments. Similarly, Stryker divested its spinal implant business to redirect investments toward high-return digital assets and tuck-in acquisitions, such as the $4.8 billion purchase of Inari Medical.

* Integration Risks and "Growth at All Costs": Globus Medical has scaled rapidly into a musculoskeletal powerhouse via the acquisitions of NuVasive and Nevro. However, its capital allocation efficiency is currently tested by severe integration pains, including potential goodwill impairment risks and a dip in robotic system installations. Meanwhile, specialists like ATEC and Orthofix operate on a "burn for growth" model. ATEC’s SG&A expenses consume over 65% of its revenue, highlighting a critical need to convert robust top-line momentum into self-sustaining free cash flow before highly leveraged balance sheets become a vulnerability.

Sector Positioning: Supply Chain Resilience

In an era of geopolitical friction and inflation, inventory management dictates true operational agility. Zimmer Biomet's heavy reliance on a bulky consignment model—exacerbated by ERP transition failures—highlights the fragility of traditional supply chains. In contrast, Orthofix’s transition toward single-use sterile packaging demonstrates superior asset flexibility, significantly reducing the logistical burdens of instrument turnover and sterilization in an increasingly cost-conscious VBP environment.

HDIN Viewpoint

At HDIN Research, our analysis indicates that the 2025 orthopedic landscape ruthlessly penalizes pure-play hardware vendors while disproportionately rewarding ecosystem architects. Hospital capital expenditure (CAPEX) is tightening; thus, the future belongs to firms capable of transitioning massive upfront robotic costs into SaaS-like or leasing models that guarantee high-margin consumable pull-through. Investors must scrutinize balance sheets for artificially inflated earnings via acquisition accounting and prioritize organizations that utilize AI and clinical data to demonstrably lower surgical revision rates. In the squeeze between VBP and DRG policies, operational efficiency and verifiable clinical evidence are the only remaining levers for premium pricing.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com