McDonald’s vs. Domino’s: Deconstructing Strategic Moats and Capital Efficiency in the QSR Sector

Date : 2026-03-02

Reading : 360

As the global Quick Service Restaurant (QSR) sector navigates shifting consumer behaviors and persistent cyclical headwinds, a fundamental divergence in survival paradigms has emerged. Based on a forensic analysis of the 2025 10-K reports, HDIN Research reveals that while McDonald’s (MCD) and Domino’s Pizza (DPZ) both boast franchise ratios exceeding 95%, their underlying growth engines are profoundly asymmetrical. McDonald's operates essentially as a highly leveraged commercial real estate investment trust (REIT) with a food brand overlay, whereas Domino’s functions as a vertically integrated, technology-driven logistics and supply chain company.

This structural divergence dictates how each giant absorbs inflation, allocates capital, and positions itself within an increasingly fragmented sector.

Financial Health: Heavy-Asset Defense vs. Vertical Integration

The fundamental difference in sector positioning between the two giants is most evident in their margin profiles and asset utilization.

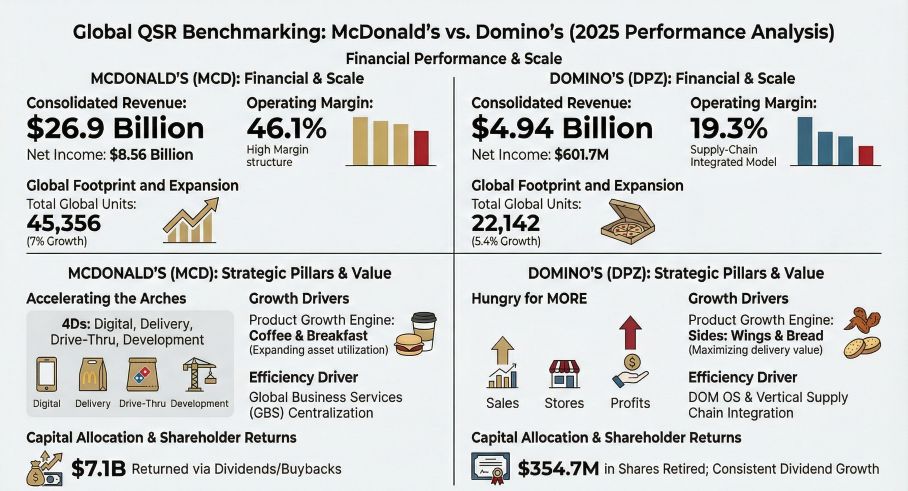

McDonald’s: The Real Estate Inflation Hedge

McDonald’s relies on a formidable capital moat underpinned by real estate. Owning 56% of the land and 80% of the buildings across its global footprint, the company generated $10.44 billion in rental income in 2025 alone—far exceeding its $6.01 billion in traditional royalty fees. This fixed-asset model provides exceptional defense during inflationary cycles. Because rent is largely tied to a percentage of franchisee sales with guaranteed minimums, McDonald's effectively hedges against inflation while achieving a sector-leading operating margin of 46.1%.

Domino’s: The Supply Chain Efficiency Engine

Conversely, Domino’s relies on a highly optimized "operational moat." Operating with extreme asset lightness at the retail level, DPZ generated 60.5% of its 2025 revenue ($2.99 billion) directly from its supply chain operations. By utilizing a formulaic "cost-plus" pricing model (such as CME spot pricing plus supply chain markup for cheese), Domino's seamlessly transfers commodity volatility to its franchisees. This results in a structurally lower gross margin but an exceptional asset turnover rate of 2.88x (compared to McDonald’s 0.45x), proving its capital allocation efficiency in supply chain maximization.

Strategic Pivots and Industry Outlook for 2026

Our analysis of management’s MD&A discussions highlights three overarching cyclical headwinds reshaping the QSR industry:

1. The Rise of "Prudent Value-ism": Both companies explicitly note that consumers are becoming increasingly discerning with disposable income. Moving into 2026, the sector's growth will hinge on the "lipstick effect"—offering extreme value alternatives to traditional dining. McDonald’s is leaning heavily into aggressive breakfast and coffee market penetration, while Domino's is driving higher average ticket sizes through high-margin side items (e.g., wings and stuffed crusts) attached to fixed delivery costs.

2. Structural Labor Cost Escalation: Legislative pressures, notably minimum wage hikes such as California's AB-1228, are permanently raising the floor on operating costs, forcing a pivot from manual operations to automated throughput.

3. The Technological Imperative: Digitalization has transitioned from an operational option to a survival baseline. The industry is attempting to break the "human reliance ceiling" by shifting capital expenditures (CapEx) toward AI-driven dispatching, automated fulfillment, and proprietary operating systems.

Capital Allocation Efficiency and Digital R&D

The ROI on digital CapEx reveals contrasting strategic priorities.

Domino’s exemplifies "Efficiency ROI." With a relatively modest $120 million in 2025 CapEx, the company sustains over 85% of its U.S. retail sales through digital channels. Its proprietary DOM OS and route-optimization algorithms directly translate digital friction reduction into higher delivery volume and supply chain throughput.

McDonald’s, however, leverages "Scale ROI." Committing a staggering $3.37 billion in 2025 CapEx, McDonald's is building a global consumer data mid-end. By targeting 250 million active loyalty members and $45 billion in loyalty-driven sales by 2027, MCD is investing heavily in a unified tech stack. While the initial capital outlay is massive, the long-tail monetization potential of this data across its 45,000+ global locations offers a significantly higher strategic ceiling.

HDIN Viewpoint: Institutional Risk and Audit Perspectives

From an independent audit perspective, HDIN Research advises institutional investors to look beyond top-line expansion and carefully scrutinize the accounting mechanisms smoothing these earnings.

* McDonald's Restructuring Camouflage: While MCD offers a superior financial safe harbor with comprehensive FX hedging strategies (including $2 billion in derivative nominal amounts and $15.4 billion in net investment hedges), investors must remain vigilant. McDonald's recorded $229 million in "Accelerating the Organization" restructuring charges in 2025. We assess a high probability that management may be utilizing these recurring "non-core" charges to mask operational friction and protect adjusted operating margins.

* Domino's Top-Line Inflation & Leverage Risks: Domino’s aggressive accounting of its advertising fund (DNAF) recorded $559 million as both revenue and expense in 2025. While GAAP-compliant, this artificially inflates total revenue by over 11% without contributing to the bottom line. Furthermore, DPZ's highly levered capital structure ($4.82 billion in debt) relies heavily on Asset-Backed Securities (ABS). This structure is fundamentally sound only as long as its "Fortressing" strategy—increasing store density to reduce delivery times—does not severely cannibalize existing franchisee unit economics. Additionally, DPZ’s lack of systematic foreign exchange hedging exposes its international royalties to unnecessary macroeconomic volatility.

Ultimately, McDonald's provides the defensive stability of a real estate conglomerate, insulated by rent mechanisms and aggressive buybacks. Domino's offers the high-velocity growth of a tech-enabled logistics firm, heavily dependent on franchise ecosystem health and supply chain volume.

Figure Clobal OSR Benchmarking McDonald's vs. Domino's (2025 Performance Analysis)

Presentation Download

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

This structural divergence dictates how each giant absorbs inflation, allocates capital, and positions itself within an increasingly fragmented sector.

Financial Health: Heavy-Asset Defense vs. Vertical Integration

The fundamental difference in sector positioning between the two giants is most evident in their margin profiles and asset utilization.

McDonald’s: The Real Estate Inflation Hedge

McDonald’s relies on a formidable capital moat underpinned by real estate. Owning 56% of the land and 80% of the buildings across its global footprint, the company generated $10.44 billion in rental income in 2025 alone—far exceeding its $6.01 billion in traditional royalty fees. This fixed-asset model provides exceptional defense during inflationary cycles. Because rent is largely tied to a percentage of franchisee sales with guaranteed minimums, McDonald's effectively hedges against inflation while achieving a sector-leading operating margin of 46.1%.

Domino’s: The Supply Chain Efficiency Engine

Conversely, Domino’s relies on a highly optimized "operational moat." Operating with extreme asset lightness at the retail level, DPZ generated 60.5% of its 2025 revenue ($2.99 billion) directly from its supply chain operations. By utilizing a formulaic "cost-plus" pricing model (such as CME spot pricing plus supply chain markup for cheese), Domino's seamlessly transfers commodity volatility to its franchisees. This results in a structurally lower gross margin but an exceptional asset turnover rate of 2.88x (compared to McDonald’s 0.45x), proving its capital allocation efficiency in supply chain maximization.

Strategic Pivots and Industry Outlook for 2026

Our analysis of management’s MD&A discussions highlights three overarching cyclical headwinds reshaping the QSR industry:

1. The Rise of "Prudent Value-ism": Both companies explicitly note that consumers are becoming increasingly discerning with disposable income. Moving into 2026, the sector's growth will hinge on the "lipstick effect"—offering extreme value alternatives to traditional dining. McDonald’s is leaning heavily into aggressive breakfast and coffee market penetration, while Domino's is driving higher average ticket sizes through high-margin side items (e.g., wings and stuffed crusts) attached to fixed delivery costs.

2. Structural Labor Cost Escalation: Legislative pressures, notably minimum wage hikes such as California's AB-1228, are permanently raising the floor on operating costs, forcing a pivot from manual operations to automated throughput.

3. The Technological Imperative: Digitalization has transitioned from an operational option to a survival baseline. The industry is attempting to break the "human reliance ceiling" by shifting capital expenditures (CapEx) toward AI-driven dispatching, automated fulfillment, and proprietary operating systems.

Capital Allocation Efficiency and Digital R&D

The ROI on digital CapEx reveals contrasting strategic priorities.

Domino’s exemplifies "Efficiency ROI." With a relatively modest $120 million in 2025 CapEx, the company sustains over 85% of its U.S. retail sales through digital channels. Its proprietary DOM OS and route-optimization algorithms directly translate digital friction reduction into higher delivery volume and supply chain throughput.

McDonald’s, however, leverages "Scale ROI." Committing a staggering $3.37 billion in 2025 CapEx, McDonald's is building a global consumer data mid-end. By targeting 250 million active loyalty members and $45 billion in loyalty-driven sales by 2027, MCD is investing heavily in a unified tech stack. While the initial capital outlay is massive, the long-tail monetization potential of this data across its 45,000+ global locations offers a significantly higher strategic ceiling.

HDIN Viewpoint: Institutional Risk and Audit Perspectives

From an independent audit perspective, HDIN Research advises institutional investors to look beyond top-line expansion and carefully scrutinize the accounting mechanisms smoothing these earnings.

* McDonald's Restructuring Camouflage: While MCD offers a superior financial safe harbor with comprehensive FX hedging strategies (including $2 billion in derivative nominal amounts and $15.4 billion in net investment hedges), investors must remain vigilant. McDonald's recorded $229 million in "Accelerating the Organization" restructuring charges in 2025. We assess a high probability that management may be utilizing these recurring "non-core" charges to mask operational friction and protect adjusted operating margins.

* Domino's Top-Line Inflation & Leverage Risks: Domino’s aggressive accounting of its advertising fund (DNAF) recorded $559 million as both revenue and expense in 2025. While GAAP-compliant, this artificially inflates total revenue by over 11% without contributing to the bottom line. Furthermore, DPZ's highly levered capital structure ($4.82 billion in debt) relies heavily on Asset-Backed Securities (ABS). This structure is fundamentally sound only as long as its "Fortressing" strategy—increasing store density to reduce delivery times—does not severely cannibalize existing franchisee unit economics. Additionally, DPZ’s lack of systematic foreign exchange hedging exposes its international royalties to unnecessary macroeconomic volatility.

Ultimately, McDonald's provides the defensive stability of a real estate conglomerate, insulated by rent mechanisms and aggressive buybacks. Domino's offers the high-velocity growth of a tech-enabled logistics firm, heavily dependent on franchise ecosystem health and supply chain volume.

Figure Clobal OSR Benchmarking McDonald's vs. Domino's (2025 Performance Analysis)

Presentation DownloadClick the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com