2025 AI Chip Giants: Strategic Moats, Cyclical Headwinds, and Sector Positioning

Date : 2026-03-02

Reading : 460

The 2025 fiscal year marks a definitive watershed in the global semiconductor landscape, driven entirely by an unprecedented surge in AI infrastructure spending. A granular financial penetration analysis by HDIN Research reveals an extreme polarization among the big three: NVIDIA has achieved systemic dominance through vertical integration, AMD is steadily expanding its market footprint via an open ecosystem, and Intel is navigating the turbulent waters of a capital-intensive strategic pivot. The era of pure "chip-level" performance competition has officially transitioned into a high-stakes battle for ecosystem dominance and supply chain sovereignty.

Figure 2025 Semiconductor Giants Strategic & Financial Face-off

Financial Health and Capital Allocation Efficiency

Financial Health and Capital Allocation Efficiency

The divergence in financial health among the top tier is stark, heavily influenced by underlying operating models and capital allocation efficiency.

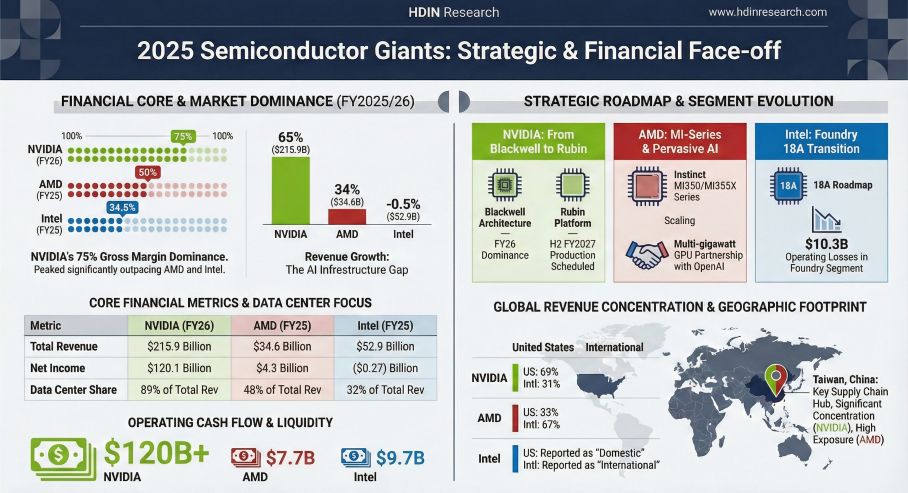

NVIDIA’s spectacular 65.5% revenue surge to $215.9 billion is not merely a volume story; it is a testament to its monopolistic pricing power. Operating on an asset-light (fabless) model, NVIDIA boasts a 71.1% gross margin and generated over $96 billion in free cash flow. This phenomenal cash conversion cycle serves as a massive war chest, allowing for aggressive $40.4 billion share buybacks and deep investments into the AI ecosystem. Furthermore, NVIDIA’s R&D efficiency is unmatched in the sector—every $1 invested in R&D yields $4.62 in top-line growth, indicating a product roadmap perfectly aligned with hyper-scale market demand.

Conversely, Intel is navigating a "profit black hole" as it doubles down on its IDM 2.0 strategy. Being the only company among the three to maintain an internal foundry model, Intel's capital expenditure consumes a staggering 46.1% of its revenue. This aggressive "build-to-compete" posture has severely compressed its free cash flow and driven its gross margins down to 34.8%.

Meanwhile, AMD continues a trajectory of solid expansion. With a 34% revenue growth propelled by its Data Center segment (up 32%), AMD exercises prudent financial leverage. While its operating margins appear temporarily compressed due to intangible asset amortization from the Xilinx acquisition, its core operating leverage remains highly competitive, validating its steady market share capture.

Strategic Pivots: From Silicon to System-Level Moats

The competitive paradigm has shifted from isolated hardware sales to integrated, rack-scale solutions.

NVIDIA has successfully transitioned from a GPU vendor to a full-stack, data-center-scale infrastructure provider. Its strategic moat is heavily fortified by its networking business (Mellanox/InfiniBand)—which saw a 142% revenue explosion—and its proprietary CUDA software ecosystem. By tightly coupling hardware with networking fabrics like NVLink for the Blackwell architecture, NVIDIA ensures immense switching costs for its enterprise clients.

AMD is positioning itself as the formidable "open ecosystem" challenger. Championing a "pervasive AI" strategy, AMD is leveraging its ROCm open software stack to dismantle closed architectures. Furthermore, its recent $4.4 billion acquisition of ZT Systems signifies a critical strategic pivot toward end-to-end AI infrastructure, enabling rapid, rack-scale deployments of its MI350X accelerators to directly challenge NVIDIA’s enterprise stronghold.

Intel is executing a defensive restructuring to secure x86 ecosystem revival and manufacturing sovereignty. Though currently enduring structural declines in traditional data center compute, Intel is pushing its "AI Everywhere" initiative by integrating NPU capabilities across its PC lineup (Core Ultra) and advancing its Gaudi 3 accelerators. Ultimately, Intel’s sector positioning hinges on sacrificing near-term profitability to successfully scale its foundry business and regain process node leadership.

Industry Outlook & Cyclical Headwinds

Despite the AI-driven supercycle, all three giants face severe cyclical headwinds dictated by macroeconomic policies and supply chain concentration.

Geopolitical friction and export controls serve as the most significant structural ceilings to global growth. The U.S. Export Administration Regulations (EAR) have forced rapid supply chain realignments. HDIN Research notes significant financial turbulence stemming from these policies: NVIDIA recorded a massive $4.5 billion inventory provision linked to H20 product restrictions in China, while AMD faced an $800 million charge for its MI308 accelerators (with subsequent partial reversals). Investors must exercise prudent financial scrutiny regarding how these massive write-downs and subsequent reversals are utilized for earnings management.

Additionally, the sector remains highly vulnerable to geographic concentration risk. A near-total reliance on Taiwan-based foundries (TSMC/UMC) and APAC-centric advanced packaging (CoWoS) means that any geopolitical disruption could trigger an immediate systemic halt in product delivery.

HDIN Viewpoint

From an institutional perspective, HDIN Research views NVIDIA as the undisputed Alpha of the current cycle, harvesting outsized returns through a deeply entrenched software-hardware moat, though macroeconomic trade policies are beginning to act as a definitive growth ceiling. AMD represents a highly resilient, high-beta challenger, intelligently using precise M&A to bridge the system-level infrastructure gap and capture structural shifts. Intel, conversely, is at a life-or-death inflection point; its valuation is currently decoupled from near-term earnings and tethered entirely to the long-term execution of its foundry roadmap and Western supply chain re-shoring initiatives.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Semiconductor Giants Strategic & Financial Face-off

Financial Health and Capital Allocation EfficiencyThe divergence in financial health among the top tier is stark, heavily influenced by underlying operating models and capital allocation efficiency.

NVIDIA’s spectacular 65.5% revenue surge to $215.9 billion is not merely a volume story; it is a testament to its monopolistic pricing power. Operating on an asset-light (fabless) model, NVIDIA boasts a 71.1% gross margin and generated over $96 billion in free cash flow. This phenomenal cash conversion cycle serves as a massive war chest, allowing for aggressive $40.4 billion share buybacks and deep investments into the AI ecosystem. Furthermore, NVIDIA’s R&D efficiency is unmatched in the sector—every $1 invested in R&D yields $4.62 in top-line growth, indicating a product roadmap perfectly aligned with hyper-scale market demand.

Conversely, Intel is navigating a "profit black hole" as it doubles down on its IDM 2.0 strategy. Being the only company among the three to maintain an internal foundry model, Intel's capital expenditure consumes a staggering 46.1% of its revenue. This aggressive "build-to-compete" posture has severely compressed its free cash flow and driven its gross margins down to 34.8%.

Meanwhile, AMD continues a trajectory of solid expansion. With a 34% revenue growth propelled by its Data Center segment (up 32%), AMD exercises prudent financial leverage. While its operating margins appear temporarily compressed due to intangible asset amortization from the Xilinx acquisition, its core operating leverage remains highly competitive, validating its steady market share capture.

Strategic Pivots: From Silicon to System-Level Moats

The competitive paradigm has shifted from isolated hardware sales to integrated, rack-scale solutions.

NVIDIA has successfully transitioned from a GPU vendor to a full-stack, data-center-scale infrastructure provider. Its strategic moat is heavily fortified by its networking business (Mellanox/InfiniBand)—which saw a 142% revenue explosion—and its proprietary CUDA software ecosystem. By tightly coupling hardware with networking fabrics like NVLink for the Blackwell architecture, NVIDIA ensures immense switching costs for its enterprise clients.

AMD is positioning itself as the formidable "open ecosystem" challenger. Championing a "pervasive AI" strategy, AMD is leveraging its ROCm open software stack to dismantle closed architectures. Furthermore, its recent $4.4 billion acquisition of ZT Systems signifies a critical strategic pivot toward end-to-end AI infrastructure, enabling rapid, rack-scale deployments of its MI350X accelerators to directly challenge NVIDIA’s enterprise stronghold.

Intel is executing a defensive restructuring to secure x86 ecosystem revival and manufacturing sovereignty. Though currently enduring structural declines in traditional data center compute, Intel is pushing its "AI Everywhere" initiative by integrating NPU capabilities across its PC lineup (Core Ultra) and advancing its Gaudi 3 accelerators. Ultimately, Intel’s sector positioning hinges on sacrificing near-term profitability to successfully scale its foundry business and regain process node leadership.

Industry Outlook & Cyclical Headwinds

Despite the AI-driven supercycle, all three giants face severe cyclical headwinds dictated by macroeconomic policies and supply chain concentration.

Geopolitical friction and export controls serve as the most significant structural ceilings to global growth. The U.S. Export Administration Regulations (EAR) have forced rapid supply chain realignments. HDIN Research notes significant financial turbulence stemming from these policies: NVIDIA recorded a massive $4.5 billion inventory provision linked to H20 product restrictions in China, while AMD faced an $800 million charge for its MI308 accelerators (with subsequent partial reversals). Investors must exercise prudent financial scrutiny regarding how these massive write-downs and subsequent reversals are utilized for earnings management.

Additionally, the sector remains highly vulnerable to geographic concentration risk. A near-total reliance on Taiwan-based foundries (TSMC/UMC) and APAC-centric advanced packaging (CoWoS) means that any geopolitical disruption could trigger an immediate systemic halt in product delivery.

HDIN Viewpoint

From an institutional perspective, HDIN Research views NVIDIA as the undisputed Alpha of the current cycle, harvesting outsized returns through a deeply entrenched software-hardware moat, though macroeconomic trade policies are beginning to act as a definitive growth ceiling. AMD represents a highly resilient, high-beta challenger, intelligently using precise M&A to bridge the system-level infrastructure gap and capture structural shifts. Intel, conversely, is at a life-or-death inflection point; its valuation is currently decoupled from near-term earnings and tethered entirely to the long-term execution of its foundry roadmap and Western supply chain re-shoring initiatives.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com