Airbus vs. Boeing: Navigating Asymmetrical Growth and Structural Divergence in the 2025 Duopoly

Date : 2026-03-03

Reading : 183

In the 2025 fiscal year, the global aerospace duopoly experienced a profound structural divergence. While both manufacturing giants boast formidable order backlogs exceeding $680 billion, the underlying quality of their operations reveals an asymmetrical battlefield. Airbus has leveraged a pristine balance sheet to launch an aggressive market offensive and secure next-generation technologies. Conversely, Boeing remains entrenched in a defensive strategic contraction, relying heavily on asset divestitures to preserve liquidity amidst severe cyclical headwinds and regulatory scrutiny.

Figure Aerospace Duel 2025: Airbus Operational Dominance vs Boeing's Strategic Rebound

Financial Health & Capital Allocation Efficiency: Cash vs. "Paper Wealth"

Financial Health & Capital Allocation Efficiency: Cash vs. "Paper Wealth"

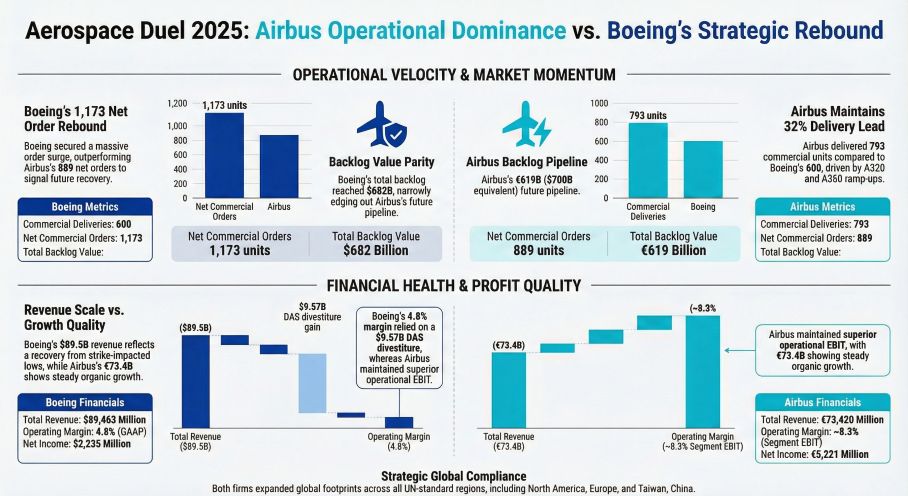

The starkest contrast between the two aerospace titans lies in their capital allocation efficiency and raw financial health. Airbus reported an impressive operating cash flow to net income (OCF/NI) ratio of 1.53, backed by a robust net cash position of $13.76 billion. This profound financial immunity has allowed Airbus to confidently resume dividend payments and fund forward-looking R&D initiatives, including hydrogen propulsion (ZEROe) and 100% Sustainable Aviation Fuel (SAF) ecosystems.

Boeing’s financial narrative requires a deeper audit. While Boeing reported a net income of $2.23 billion in 2025, HDIN Research notes this is primarily a symptom of "paper wealth." This profitability was artificially engineered by a $9.56 billion one-time gain from the divestiture of its Digital Aviation Solutions (DAS) business. Stripped of this asset sale, Boeing's core operations remain in a deep deficit, burdened by over $54 billion in total debt and an OCF/NI ratio of merely 0.48. By liquidating high-margin digital assets to survive, Boeing is sacrificing its long-term services moat for short-term liquidity preservation.

Production Resilience and Order Execution

Both companies command strategic moats through massive backlogs, but market share is no longer dictated by demand—it is now governed by production certainty.

Operational efficiency drove Airbus to deliver 793 commercial aircraft in 2025—outpacing Boeing by 32%. Despite industry-wide engine shortages, Airbus is actively scaling its A320neo family production to a targeted 75 aircraft per month by 2027, establishing an absolute generational advantage in the narrow-body sector.

Boeing’s capacity ramp-up, however, is severely restricted. Delivering 600 aircraft in 2025, Boeing’s production lines were disrupted by a 101-day labor strike and stringent FAA quality audits. Furthermore, the structural hemorrhage in its wide-body segment continues, with the flagship 777X delayed to 2027, triggering a staggering $4.89 billion in reach-forward losses in 2025 alone.

Strategic Pivots: Vertical Integration in the Supply Chain

Faced with identical cyclical headwinds—including core component shortages, labor inflation, and volatile raw material costs (e.g., titanium)—both manufacturers executed parallel defensive strategies in 2025.

The industry’s most consequential move was the joint, split acquisition of key supplier Spirit AeroSystems. This transition from "Buy" to "Make" signifies a historic pivot in supply chain philosophy. By absorbing critical fuselage and aerostructure manufacturing back internally, both Airbus and Boeing are attempting to eliminate "traveled work," fortify their supply chain moats, and strictly enforce internal quality control against an increasingly fragile global macroeconomic backdrop.

Sector Positioning: The Middle East and Asia-Pacific Battlegrounds

Geographic sector positioning further underscores this duopoly's divergence. In the Middle East—a critical arena for wide-body fleet renewals—Airbus captured a staggering 114% year-over-year revenue growth, rapidly absorbing market share left vulnerable by Boeing’s 777X delivery gaps.

Simultaneously, the Asia-Pacific region, anchored by the indispensable Chinese market, remains a foundational growth engine for both entities. While Airbus continues a steady endogenous expansion in the region, Boeing’s sector positioning remains highly sensitive to geopolitical crossfires and trade tariffs, presenting an asymmetrical risk to its global cost-amortization capabilities.

HDIN Viewpoint

From an institutional perspective, HDIN Research observes that the 2025 fiscal year represents a tipping point where capital efficiency dictates the trajectory of aerospace innovation. Airbus has officially transitioned back into a mature, highly profitable enterprise capable of dictating the industry's green transition. Conversely, Boeing is enduring a prolonged "ICU phase" for its balance sheet. Its strategic contraction and massive equity dilution mask underlying operational vulnerabilities. Moving forward, the true victor of this duopoly will not be decided by who secures the most orders, but by who can organically convert their backlog into pristine operating cash flow without cannibalizing their core assets.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Aerospace Duel 2025: Airbus Operational Dominance vs Boeing's Strategic Rebound

Financial Health & Capital Allocation Efficiency: Cash vs. "Paper Wealth"The starkest contrast between the two aerospace titans lies in their capital allocation efficiency and raw financial health. Airbus reported an impressive operating cash flow to net income (OCF/NI) ratio of 1.53, backed by a robust net cash position of $13.76 billion. This profound financial immunity has allowed Airbus to confidently resume dividend payments and fund forward-looking R&D initiatives, including hydrogen propulsion (ZEROe) and 100% Sustainable Aviation Fuel (SAF) ecosystems.

Boeing’s financial narrative requires a deeper audit. While Boeing reported a net income of $2.23 billion in 2025, HDIN Research notes this is primarily a symptom of "paper wealth." This profitability was artificially engineered by a $9.56 billion one-time gain from the divestiture of its Digital Aviation Solutions (DAS) business. Stripped of this asset sale, Boeing's core operations remain in a deep deficit, burdened by over $54 billion in total debt and an OCF/NI ratio of merely 0.48. By liquidating high-margin digital assets to survive, Boeing is sacrificing its long-term services moat for short-term liquidity preservation.

Production Resilience and Order Execution

Both companies command strategic moats through massive backlogs, but market share is no longer dictated by demand—it is now governed by production certainty.

Operational efficiency drove Airbus to deliver 793 commercial aircraft in 2025—outpacing Boeing by 32%. Despite industry-wide engine shortages, Airbus is actively scaling its A320neo family production to a targeted 75 aircraft per month by 2027, establishing an absolute generational advantage in the narrow-body sector.

Boeing’s capacity ramp-up, however, is severely restricted. Delivering 600 aircraft in 2025, Boeing’s production lines were disrupted by a 101-day labor strike and stringent FAA quality audits. Furthermore, the structural hemorrhage in its wide-body segment continues, with the flagship 777X delayed to 2027, triggering a staggering $4.89 billion in reach-forward losses in 2025 alone.

Strategic Pivots: Vertical Integration in the Supply Chain

Faced with identical cyclical headwinds—including core component shortages, labor inflation, and volatile raw material costs (e.g., titanium)—both manufacturers executed parallel defensive strategies in 2025.

The industry’s most consequential move was the joint, split acquisition of key supplier Spirit AeroSystems. This transition from "Buy" to "Make" signifies a historic pivot in supply chain philosophy. By absorbing critical fuselage and aerostructure manufacturing back internally, both Airbus and Boeing are attempting to eliminate "traveled work," fortify their supply chain moats, and strictly enforce internal quality control against an increasingly fragile global macroeconomic backdrop.

Sector Positioning: The Middle East and Asia-Pacific Battlegrounds

Geographic sector positioning further underscores this duopoly's divergence. In the Middle East—a critical arena for wide-body fleet renewals—Airbus captured a staggering 114% year-over-year revenue growth, rapidly absorbing market share left vulnerable by Boeing’s 777X delivery gaps.

Simultaneously, the Asia-Pacific region, anchored by the indispensable Chinese market, remains a foundational growth engine for both entities. While Airbus continues a steady endogenous expansion in the region, Boeing’s sector positioning remains highly sensitive to geopolitical crossfires and trade tariffs, presenting an asymmetrical risk to its global cost-amortization capabilities.

HDIN Viewpoint

From an institutional perspective, HDIN Research observes that the 2025 fiscal year represents a tipping point where capital efficiency dictates the trajectory of aerospace innovation. Airbus has officially transitioned back into a mature, highly profitable enterprise capable of dictating the industry's green transition. Conversely, Boeing is enduring a prolonged "ICU phase" for its balance sheet. Its strategic contraction and massive equity dilution mask underlying operational vulnerabilities. Moving forward, the true victor of this duopoly will not be decided by who secures the most orders, but by who can organically convert their backlog into pristine operating cash flow without cannibalizing their core assets.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com