BeOne Medicines 2025: From Biotech Challenger to Global Big Pharma

Date : 2026-03-02

Reading : 1612

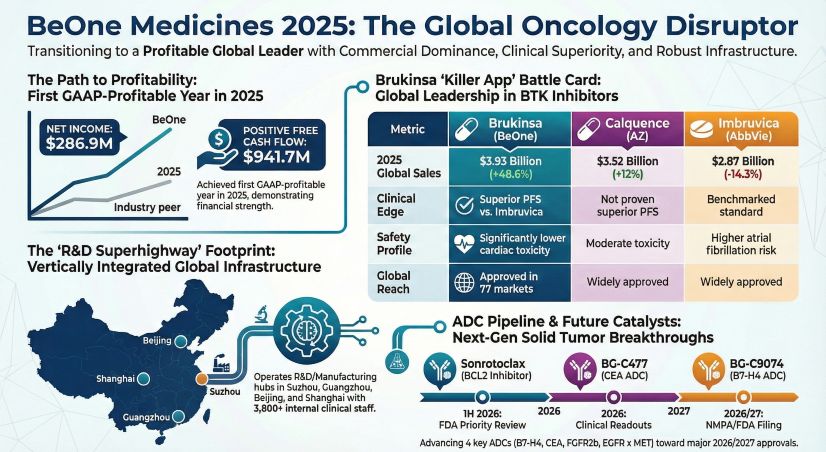

In fiscal year 2025, BeOne Medicines successfully crossed a critical industry inflection point, transitioning from a capital-reliant biotechnology firm into a self-sustaining, vertically integrated Big Pharma. Driven by its proprietary "Global R&D Superhighway," BeOne reported its first-ever GAAP full-year profit of $287 million and a positive free cash flow (FCF) of $942 million. Rather than merely a milestone of revenue scale, this financial pivot highlights a profound validation of BeOne's capital allocation efficiency and its strategic capacity to disrupt established oncology monopolies.

图 Beone Medicines 2025:全球肿瘤领域的颠覆者

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

BeOne’s 2025 financial posture reflects the aggressive release of operating leverage. Total revenue surged 40.2% to $5.34 billion, but more importantly, the strategic implications lie in the structural cost optimization.

Operational efficiency and market expansion drove a substantial margin expansion, pushing product gross margins from 84.3% to a sector-leading 87.3%. This is largely attributed to the high-margin profile of its in-house assets—specifically BRUKINSA, which accounted for 73.5% of total revenue. By retaining 100% of global rights for its core assets, BeOne mitigates the margin dilution typically associated with heavy in-licensing. Furthermore, BeOne demonstrated sophisticated balance sheet management, monetizing future IMDELLTRA royalties for $911 million in cash. While this functions as a financing liability, it significantly fortifies their liquidity cushion without diluting equity.

Simultaneously, the R&D-to-revenue ratio plummeted from 51.3% to 40.2%. This declining R&D intensity does not indicate reduced innovation, but rather proves that commercial revenue growth is radically outpacing fixed R&D infrastructure costs.

Strategic Moats & Sector Positioning

BeOne’s sector positioning is underpinned by two distinct strategic moats: clinical supremacy in the BTK inhibitor landscape and a highly internalized operational model.

* The BTK Power Shift: BRUKINSA generated $3.93 billion in global sales (a 48.6% increase), officially dethroning AbbVie/Janssen’s Imbruvica ($2.87 billion) and outpacing AstraZeneca’s Calquence ($3.52 billion). This market share capture is not merely driven by commercial expansion, but by the "Best-in-Class" clinical data from the head-to-head ALPINE study, which proved BRUKINSA's superior progression-free survival (PFS) and lower cardiac toxicity.

* Differentiated PD-1 Penetration: In a solid tumor market dominated by Merck's Keytruda ($31.68 billion) and BMS's Opdivo, BeOne’s TEVIMBRA ($737 million) has carved out a highly defensible niche. By utilizing an Fc gamma receptors engineered mechanism to minimize macrophage binding and enhance T-cell activity, TEVIMBRA is successfully penetrating specific high-incidence indications, such as second-line esophageal squamous cell carcinoma (ESCC) and first-line gastric cancers.

* The Internal R&D Engine: Unlike legacy Big Pharma peers heavily reliant on Contract Research Organizations (CROs), BeOne leverages an internal clinical team of approximately 3,800 personnel operating across six continents. This vertical integration slashes clinical development costs by up to 75% compared to industry averages, granting BeOne a formidable cost advantage in advancing its pipeline, including its next-generation BTK-CDAC (BGB-16673).

Cyclical Headwinds & Geopolitical De-Risking

Despite its robust financial health, BeOne operates in a highly volatile geopolitical and regulatory environment. To counter the cyclical headwinds generated by the impending U.S. BIOSECURE Act and broader supply chain decoupling, BeOne has enacted a "reverse localization" strategy.

By redomiciling to Switzerland and centralizing its 2025 core capital expenditures into a new 8,000-liter biologics manufacturing facility in Hopewell, New Jersey, BeOne is physically and legally insulating its U.S. supply chain from its Chinese operations (which still account for 31.4% of total revenue). However, legal headwinds remain a persistent threat. The company is actively managing a patent challenge (ANDA) from Zydus regarding BRUKINSA, as well as an ongoing trade secret dispute with AbbVie concerning its pipeline asset BGB-16673. Managing these legal expenses and safeguarding IP will be paramount to preserving long-term valuation.

HDIN Viewpoint

HDIN Research analysts assert that BeOne Medicines is no longer competing as a regional Biotech, but as an aggressive, global oncology challenger. Its "Global R&D Superhighway" has definitively proven its capacity to generate high-margin structural returns. While AstraZeneca acts as the aggregator in the ADC space and Roche defends the IO combo domain, BeOne is deploying an asymmetric, low-cost R&D strategy to achieve comprehensive market penetration. Moving forward, the true test of BeOne's valuation premium will hinge not on market access, but on its ability to navigate geopolitical friction and successfully commercialize its next wave of novel therapies, such as the BCL2 inhibitor Sonrotoclax.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

图 Beone Medicines 2025:全球肿瘤领域的颠覆者

Financial Health & Capital Allocation EfficiencyBeOne’s 2025 financial posture reflects the aggressive release of operating leverage. Total revenue surged 40.2% to $5.34 billion, but more importantly, the strategic implications lie in the structural cost optimization.

Operational efficiency and market expansion drove a substantial margin expansion, pushing product gross margins from 84.3% to a sector-leading 87.3%. This is largely attributed to the high-margin profile of its in-house assets—specifically BRUKINSA, which accounted for 73.5% of total revenue. By retaining 100% of global rights for its core assets, BeOne mitigates the margin dilution typically associated with heavy in-licensing. Furthermore, BeOne demonstrated sophisticated balance sheet management, monetizing future IMDELLTRA royalties for $911 million in cash. While this functions as a financing liability, it significantly fortifies their liquidity cushion without diluting equity.

Simultaneously, the R&D-to-revenue ratio plummeted from 51.3% to 40.2%. This declining R&D intensity does not indicate reduced innovation, but rather proves that commercial revenue growth is radically outpacing fixed R&D infrastructure costs.

Strategic Moats & Sector Positioning

BeOne’s sector positioning is underpinned by two distinct strategic moats: clinical supremacy in the BTK inhibitor landscape and a highly internalized operational model.

* The BTK Power Shift: BRUKINSA generated $3.93 billion in global sales (a 48.6% increase), officially dethroning AbbVie/Janssen’s Imbruvica ($2.87 billion) and outpacing AstraZeneca’s Calquence ($3.52 billion). This market share capture is not merely driven by commercial expansion, but by the "Best-in-Class" clinical data from the head-to-head ALPINE study, which proved BRUKINSA's superior progression-free survival (PFS) and lower cardiac toxicity.

* Differentiated PD-1 Penetration: In a solid tumor market dominated by Merck's Keytruda ($31.68 billion) and BMS's Opdivo, BeOne’s TEVIMBRA ($737 million) has carved out a highly defensible niche. By utilizing an Fc gamma receptors engineered mechanism to minimize macrophage binding and enhance T-cell activity, TEVIMBRA is successfully penetrating specific high-incidence indications, such as second-line esophageal squamous cell carcinoma (ESCC) and first-line gastric cancers.

* The Internal R&D Engine: Unlike legacy Big Pharma peers heavily reliant on Contract Research Organizations (CROs), BeOne leverages an internal clinical team of approximately 3,800 personnel operating across six continents. This vertical integration slashes clinical development costs by up to 75% compared to industry averages, granting BeOne a formidable cost advantage in advancing its pipeline, including its next-generation BTK-CDAC (BGB-16673).

Cyclical Headwinds & Geopolitical De-Risking

Despite its robust financial health, BeOne operates in a highly volatile geopolitical and regulatory environment. To counter the cyclical headwinds generated by the impending U.S. BIOSECURE Act and broader supply chain decoupling, BeOne has enacted a "reverse localization" strategy.

By redomiciling to Switzerland and centralizing its 2025 core capital expenditures into a new 8,000-liter biologics manufacturing facility in Hopewell, New Jersey, BeOne is physically and legally insulating its U.S. supply chain from its Chinese operations (which still account for 31.4% of total revenue). However, legal headwinds remain a persistent threat. The company is actively managing a patent challenge (ANDA) from Zydus regarding BRUKINSA, as well as an ongoing trade secret dispute with AbbVie concerning its pipeline asset BGB-16673. Managing these legal expenses and safeguarding IP will be paramount to preserving long-term valuation.

HDIN Viewpoint

HDIN Research analysts assert that BeOne Medicines is no longer competing as a regional Biotech, but as an aggressive, global oncology challenger. Its "Global R&D Superhighway" has definitively proven its capacity to generate high-margin structural returns. While AstraZeneca acts as the aggregator in the ADC space and Roche defends the IO combo domain, BeOne is deploying an asymmetric, low-cost R&D strategy to achieve comprehensive market penetration. Moving forward, the true test of BeOne's valuation premium will hinge not on market access, but on its ability to navigate geopolitical friction and successfully commercialize its next wave of novel therapies, such as the BCL2 inhibitor Sonrotoclax.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com