2025 America Fertilizer Giants: Decarbonization, Automation, and Strategic Moats

Date : 2026-03-04

Reading : 612

The Americas fertilizer sector has officially exited the era of brute-force capacity expansion. Based on HDIN Research’s comprehensive analysis of FY2025 data across five industry titans—CF Industries, Nutrien, Mosaic, LSB Industries, and CVR Partners—a structural bifurcation is underway. Companies are aggressively reallocating capital to capture "green premiums" and shield themselves from cyclical headwinds. Scale alone is no longer a sufficient competitive advantage; today, the ultimate strategic moats are defined by energy-logistics-channel integration and aggressive technological pivots.

Figure 2025 Americans Fertilizer Giants: A Comparative Analysis

Strategic Pivots: The Decarbonization and Automation Imperative

Strategic Pivots: The Decarbonization and Automation Imperative

In FY2025, capital expenditure (CapEx) logic shifted dramatically toward long-term operational resilience and low-carbon energy applications.

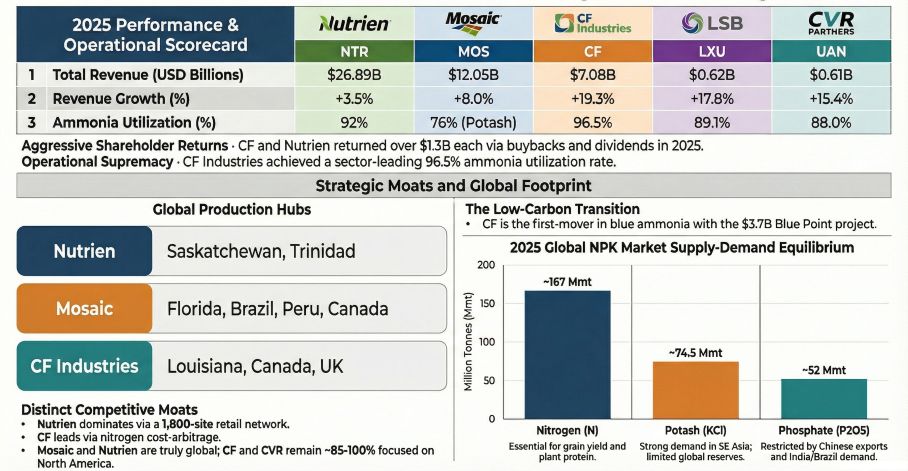

CF Industries has positioned itself as the vanguard of the clean energy transition. By allocating a significant portion of its $950 million CapEx toward decarbonization—most notably the $3.7 billion Blue Point blue ammonia joint venture—the company is actively transforming nitrogen from a traditional agricultural input into a zero-carbon maritime and power-generation fuel. This pivot allows CF to capitalize on Section 45Q tax credits and bypass the cyclical headwinds of agricultural markets.

Conversely, Nutrien has focused its technological investments on upstream asset optimization. By achieving a 49% automated extraction rate in its potash mines, Nutrien has significantly driven down controllable cash costs, fortifying its cost leadership while enhancing operational safety.

Sector Positioning: Vertical Integration vs. Niche Arbitrage

The FY2025 landscape highlights a stark contrast in how market share is defended through structural positioning.

Nutrien maintains a Americas retail hegemony. With a network of over 1,800 retail locations and a proprietary financing arm, the company has effectively built a captive market. This downstream vertical integration acts as a powerful buffer against commodity price volatility, ensuring stable product distribution even during agricultural downturns. Similarly, Mosaic leverages its vertical integration in phosphates—capturing value from rock mining in Florida and South America to Americas logistics—allowing it to dominate 72% of North American concentrated phosphate production.

Meanwhile, smaller players are carving out highly defensible niche moats. LSB Industries has strategically pivoted away from volatile agricultural spot markets toward industrial applications. By securing long-term, natural gas cost pass-through contracts for industrial-grade ammonium nitrate (ANS), LSB successfully locks in processing margins regardless of raw material price spikes. CVR Partners relies on a unique feedstock arbitrage model, utilizing petroleum coke gasification—the only facility of its kind in North America—to insulate its cost structure during periods of extreme natural gas volatility.

Capital Allocation Efficiency and Financial Health

High cash-conversion efficiency characterized the sector's top-tier players in FY2025, driving aggressive shareholder return programs and portfolio optimizations.

CF Industries demonstrated unparalleled capital allocation flexibility, repurchasing $1.35 billion in shares (reducing outstanding shares by 10%) while simultaneously funding massive green energy projects. This was driven by a sector-leading operating margin of 32.5%, anchored by North America's structural natural gas cost advantage.

Nutrien also showcased adept balance sheet management by divesting non-core minority stakes—such as its holdings in Sinofert and Profertil—to repatriate roughly $900 million. This disciplined capital recycling allows the company to double down on high-yield North American assets. In contrast, Mosaic’s capital allocation remains heavily weighted toward asset integrity and environmental compliance, with $796 million directed toward land reclamation and phosphogypsum stack closures, reflecting the high implicit costs of legacy phosphate assets.

HDIN Viewpoint: Financial Red Flags and Macro Ceilings

While the FY2025 operational metrics present a robust industry outlook, HDIN Research advises institutional investors to maintain a healthy skepticism regarding underlying financial reporting and macro constraints.

1. Asset Retirement Obligation (ARO) Sensitivities: We note that certain potash and phosphate operators utilize extremely long duration assumptions for AROs—in Nutrien’s case, up to 520 years for specific mines. Investors must recognize that minute adjustments to discount rates on these ultra-long timelines can be utilized by management to artificially deflate balance sheet liabilities.

2. Derivatives and Earnings Quality: Because players like CF Industries do not apply hedge accounting to all natural gas derivatives, non-cash Mark-to-Market (MTM) fluctuations flow directly into the income statement. Core EBITDA assessments must strip out this noise to reveal true operational profitability.

3. Macro Headwinds: The impending enforcement of the EU’s Carbon Border Adjustment Mechanism (CBAM) in 2026, alongside ongoing antitrust investigations by the USDA and DOJ regarding market manipulation in agricultural inputs, serve as definitive macro ceilings that could restrict future pricing power and export margins.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click the link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Americans Fertilizer Giants: A Comparative Analysis

Strategic Pivots: The Decarbonization and Automation ImperativeIn FY2025, capital expenditure (CapEx) logic shifted dramatically toward long-term operational resilience and low-carbon energy applications.

CF Industries has positioned itself as the vanguard of the clean energy transition. By allocating a significant portion of its $950 million CapEx toward decarbonization—most notably the $3.7 billion Blue Point blue ammonia joint venture—the company is actively transforming nitrogen from a traditional agricultural input into a zero-carbon maritime and power-generation fuel. This pivot allows CF to capitalize on Section 45Q tax credits and bypass the cyclical headwinds of agricultural markets.

Conversely, Nutrien has focused its technological investments on upstream asset optimization. By achieving a 49% automated extraction rate in its potash mines, Nutrien has significantly driven down controllable cash costs, fortifying its cost leadership while enhancing operational safety.

Sector Positioning: Vertical Integration vs. Niche Arbitrage

The FY2025 landscape highlights a stark contrast in how market share is defended through structural positioning.

Nutrien maintains a Americas retail hegemony. With a network of over 1,800 retail locations and a proprietary financing arm, the company has effectively built a captive market. This downstream vertical integration acts as a powerful buffer against commodity price volatility, ensuring stable product distribution even during agricultural downturns. Similarly, Mosaic leverages its vertical integration in phosphates—capturing value from rock mining in Florida and South America to Americas logistics—allowing it to dominate 72% of North American concentrated phosphate production.

Meanwhile, smaller players are carving out highly defensible niche moats. LSB Industries has strategically pivoted away from volatile agricultural spot markets toward industrial applications. By securing long-term, natural gas cost pass-through contracts for industrial-grade ammonium nitrate (ANS), LSB successfully locks in processing margins regardless of raw material price spikes. CVR Partners relies on a unique feedstock arbitrage model, utilizing petroleum coke gasification—the only facility of its kind in North America—to insulate its cost structure during periods of extreme natural gas volatility.

Capital Allocation Efficiency and Financial Health

High cash-conversion efficiency characterized the sector's top-tier players in FY2025, driving aggressive shareholder return programs and portfolio optimizations.

CF Industries demonstrated unparalleled capital allocation flexibility, repurchasing $1.35 billion in shares (reducing outstanding shares by 10%) while simultaneously funding massive green energy projects. This was driven by a sector-leading operating margin of 32.5%, anchored by North America's structural natural gas cost advantage.

Nutrien also showcased adept balance sheet management by divesting non-core minority stakes—such as its holdings in Sinofert and Profertil—to repatriate roughly $900 million. This disciplined capital recycling allows the company to double down on high-yield North American assets. In contrast, Mosaic’s capital allocation remains heavily weighted toward asset integrity and environmental compliance, with $796 million directed toward land reclamation and phosphogypsum stack closures, reflecting the high implicit costs of legacy phosphate assets.

HDIN Viewpoint: Financial Red Flags and Macro Ceilings

While the FY2025 operational metrics present a robust industry outlook, HDIN Research advises institutional investors to maintain a healthy skepticism regarding underlying financial reporting and macro constraints.

1. Asset Retirement Obligation (ARO) Sensitivities: We note that certain potash and phosphate operators utilize extremely long duration assumptions for AROs—in Nutrien’s case, up to 520 years for specific mines. Investors must recognize that minute adjustments to discount rates on these ultra-long timelines can be utilized by management to artificially deflate balance sheet liabilities.

2. Derivatives and Earnings Quality: Because players like CF Industries do not apply hedge accounting to all natural gas derivatives, non-cash Mark-to-Market (MTM) fluctuations flow directly into the income statement. Core EBITDA assessments must strip out this noise to reveal true operational profitability.

3. Macro Headwinds: The impending enforcement of the EU’s Carbon Border Adjustment Mechanism (CBAM) in 2026, alongside ongoing antitrust investigations by the USDA and DOJ regarding market manipulation in agricultural inputs, serve as definitive macro ceilings that could restrict future pricing power and export margins.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click the link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com