Global Oral Care 2025: From Volume Expansion to Value Extraction

Date : 2026-03-03

Reading : 157

In 2025, the global oral care industry has undergone a definitive paradigm shift, pivoting away from sheer volume expansion toward aggressive value extraction. Confronted by cyclical headwinds—including persistent inflation and geopolitical supply chain disruptions—FMCG titans are actively executing a strategic triad: portfolio pruning, irresistible premiumization, and digital overhaul. According to HDIN Research, this structural evolution dictates that future market dominance will no longer rely solely on distribution ubiquity, but rather on technological superiority and clinical validation.

Figure 2025 Consumer Giants Benchmark Performance, Segments, and Sustainability

Strategic Pivots: Navigating Inflation and Cyclical Headwinds

Strategic Pivots: Navigating Inflation and Cyclical Headwinds

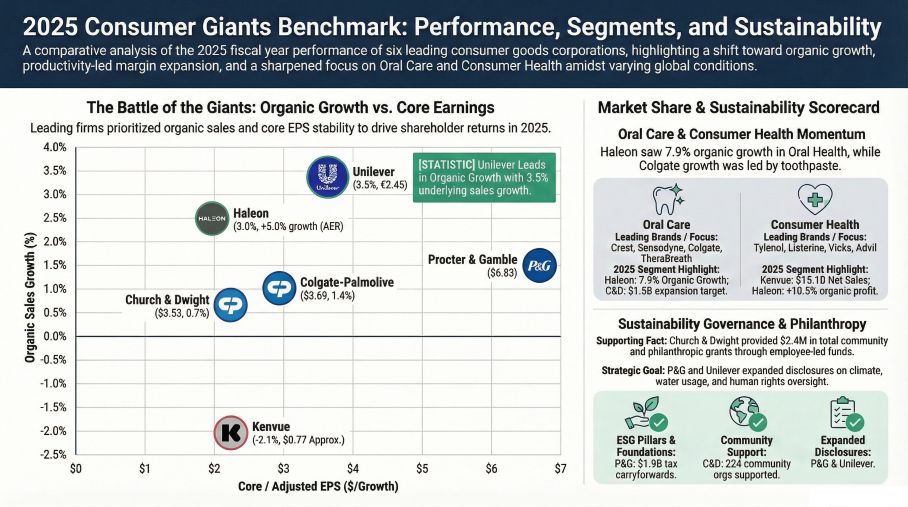

In a volatile macroeconomic environment, consumer bifurcation has severely tested corporate elasticity. Rising inflation has triggered notable trade-down behavior, pushing consumers toward private labels and pressuring premium tool brands like Church & Dwight’s Waterpik. To counteract these cyclical headwinds, industry leaders are leveraging surgical pricing and aggressive productivity programs to protect margins.

Haleon leveraged its clinical science heritage to command strong pricing power, culminating in an industry-leading 7.9% organic growth within its oral health division. Concurrently, giants like Unilever and Kenvue implemented massive structural cost-reduction initiatives. Unilever’s €670 million savings program optimized management efficiency, elevating its operating margin by 60 basis points, while Kenvue’s "Our Vue Forward" initiative generated over $350 million in annualized pre-tax cost savings to subsidize further brand investments.

Sector Positioning: Capital Allocation and Cross-Category Synergies

A critical finding in our 2025 analysis is the "cash cow" subsidy model. Companies with significant non-oral care exposure rely on the formidable free cash flow (FCF) generated by their core divisions to fund capital-intensive oral care R&D. Procter & Gamble (P&G) and Unilever utilize the immense scale of their Fabric & Home Care and Personal Care segments to command superior supply chain bargaining power, effectively hedging against the slow growth of the mature manual toothbrush market.

However, beneath the surface of robust cash flows lie potential red flags regarding financial integrity. HDIN Research notes that the recent wave of non-cash asset impairments—such as Colgate-Palmolive’s $919 million skin health write-down and Kenvue’s structural adjustment charges—may represent a "kitchen-sinking" approach designed to reset asset bases and artificially enhance future Return on Assets (ROA).

Strategic Moats: AI Integration and Supply Chain De-Risking

Artificial Intelligence is no longer a peripheral concept; it has become the nucleus of capital expenditure. The competitive moat has shifted from basic oral hygiene to AI-driven, personalized clinical solutions. P&G is leveraging AI platforms like the Oral-B iO App for real-time consumer feedback, while Unilever utilizes "Digital Twins" to simulate formulations, effectively reducing SKUs and raw material costs without compromising product efficacy. Colgate has explicitly embedded AI into its 2030 strategy to accelerate omnichannel demand generation.

Simultaneously, tariff policies and trade restrictions have forced an unprecedented de-risking of the global supply chain. Strategic manufacturing relocation is paramount. Church & Dwight has strategically halted the import of the vast majority of its Waterpik products from China into the US to circumvent tariff risks. Meanwhile, Kenvue is navigating an estimated $130 million annualized cost increase tied to 2025 executive orders, demanding highly aggressive supply chain optimization to shield gross margins.

HDIN Viewpoint

From an institutional investor perspective, HDIN Research advises a heavy weighting toward players exhibiting high operating leverage and unassailable scientific moats. Haleon and P&G emerge as the clear industry victors. Haleon's clinical heritage (sensory and gum health) provides unparalleled defense against inflation, while P&G's "irresistible superiority" framework continuously extracts super-premium margins from a saturated market.

Conversely, companies operating as "transitioning laggards," such as Kenvue and Church & Dwight, require prudent observation. Investors must closely monitor their margin repair trajectories and market share stabilization in North America as they navigate the costly turbulence of tariff-induced supply chain restructuring and post-spinoff integration.

Presentation download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Consumer Giants Benchmark Performance, Segments, and Sustainability

Strategic Pivots: Navigating Inflation and Cyclical HeadwindsIn a volatile macroeconomic environment, consumer bifurcation has severely tested corporate elasticity. Rising inflation has triggered notable trade-down behavior, pushing consumers toward private labels and pressuring premium tool brands like Church & Dwight’s Waterpik. To counteract these cyclical headwinds, industry leaders are leveraging surgical pricing and aggressive productivity programs to protect margins.

Haleon leveraged its clinical science heritage to command strong pricing power, culminating in an industry-leading 7.9% organic growth within its oral health division. Concurrently, giants like Unilever and Kenvue implemented massive structural cost-reduction initiatives. Unilever’s €670 million savings program optimized management efficiency, elevating its operating margin by 60 basis points, while Kenvue’s "Our Vue Forward" initiative generated over $350 million in annualized pre-tax cost savings to subsidize further brand investments.

Sector Positioning: Capital Allocation and Cross-Category Synergies

A critical finding in our 2025 analysis is the "cash cow" subsidy model. Companies with significant non-oral care exposure rely on the formidable free cash flow (FCF) generated by their core divisions to fund capital-intensive oral care R&D. Procter & Gamble (P&G) and Unilever utilize the immense scale of their Fabric & Home Care and Personal Care segments to command superior supply chain bargaining power, effectively hedging against the slow growth of the mature manual toothbrush market.

However, beneath the surface of robust cash flows lie potential red flags regarding financial integrity. HDIN Research notes that the recent wave of non-cash asset impairments—such as Colgate-Palmolive’s $919 million skin health write-down and Kenvue’s structural adjustment charges—may represent a "kitchen-sinking" approach designed to reset asset bases and artificially enhance future Return on Assets (ROA).

Strategic Moats: AI Integration and Supply Chain De-Risking

Artificial Intelligence is no longer a peripheral concept; it has become the nucleus of capital expenditure. The competitive moat has shifted from basic oral hygiene to AI-driven, personalized clinical solutions. P&G is leveraging AI platforms like the Oral-B iO App for real-time consumer feedback, while Unilever utilizes "Digital Twins" to simulate formulations, effectively reducing SKUs and raw material costs without compromising product efficacy. Colgate has explicitly embedded AI into its 2030 strategy to accelerate omnichannel demand generation.

Simultaneously, tariff policies and trade restrictions have forced an unprecedented de-risking of the global supply chain. Strategic manufacturing relocation is paramount. Church & Dwight has strategically halted the import of the vast majority of its Waterpik products from China into the US to circumvent tariff risks. Meanwhile, Kenvue is navigating an estimated $130 million annualized cost increase tied to 2025 executive orders, demanding highly aggressive supply chain optimization to shield gross margins.

HDIN Viewpoint

From an institutional investor perspective, HDIN Research advises a heavy weighting toward players exhibiting high operating leverage and unassailable scientific moats. Haleon and P&G emerge as the clear industry victors. Haleon's clinical heritage (sensory and gum health) provides unparalleled defense against inflation, while P&G's "irresistible superiority" framework continuously extracts super-premium margins from a saturated market.

Conversely, companies operating as "transitioning laggards," such as Kenvue and Church & Dwight, require prudent observation. Investors must closely monitor their margin repair trajectories and market share stabilization in North America as they navigate the costly turbulence of tariff-induced supply chain restructuring and post-spinoff integration.

Presentation download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com