The 2026 Inflection Point: Transitioning from R&D OEM to Full-Stack eVTOL Operator

Date : 2026-03-04

Reading : 115

As the advanced air mobility (AAM) sector approaches its commercialization dawn, Joby Aviation is orchestrating a critical transition from a research-intensive original equipment manufacturer (OEM) to a vertically integrated urban air mobility (UAM) operator. According to HDIN Research's deep-dive analysis of Joby's 2025 Form 10-K, the company has established a formidable global footprint anchored in the U.S. and the UAE. Propelled by the strategic acquisition of Blade and a massive liquidity fortress of approximately $2.7 billion post-early-2026 financing, Joby is aggressively engineering its capital structure to support a 2026 commercial launch. However, converting early-mover advantages into sustainable unit economics will require navigating severe regulatory, infrastructural, and manufacturing headwinds.

Figure Joby Aviation: FY2025 Performance & The Path to 2026 Commercialization

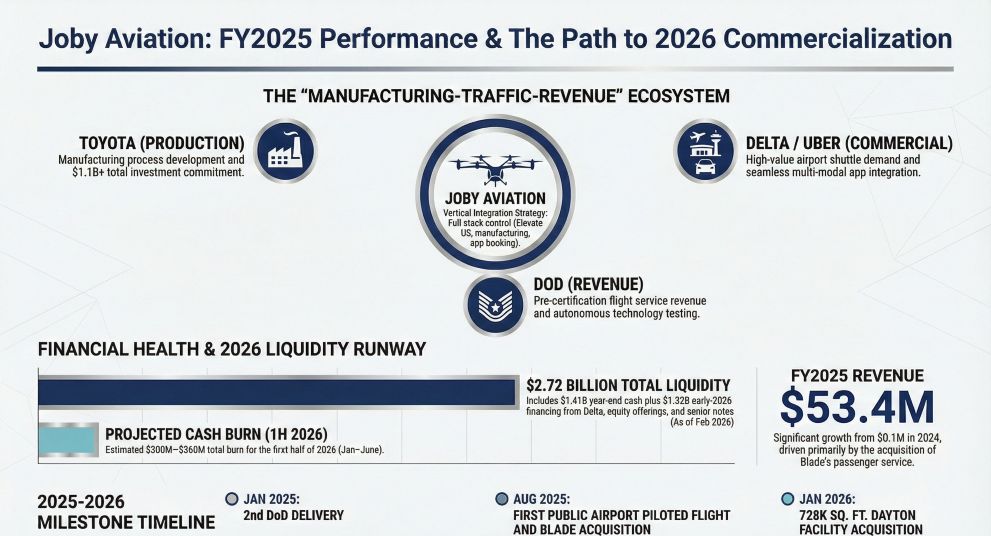

Strategic Pivots: Forging an Unassailable Ecosystem

Strategic Pivots: Forging an Unassailable Ecosystem

Joby’s sector positioning is defined by a "manufacturing-traffic-infrastructure" trinity, carefully de-risked through blue-chip alliances. This strategic moat effectively addresses the fundamental challenges of scaling a novel transportation network:

* Manufacturing Scalability (Toyota): Solving the "how to build" equation, Toyota’s $650 million cumulative investment and deep integration into Joby’s manufacturing layout ensure automotive-grade reliability. The January 2026 acquisition of a 728,000-square-foot facility in Vandalia, Ohio, marks the essential leap from low-rate prototyping in California to high-rate industrial production.

* Customer Acquisition & Software Ecosystem (Uber & Blade): The integration of Uber’s demand-aggregation platform drastically lowers customer acquisition costs (CAC). Furthermore, the August 2025 acquisition of Blade’s passenger operations immediately secured key airspace access in New York and generated $34.8 million in passenger revenue. This operational "sandbox" allows Joby to stress-test its proprietary *Elevate OS* platform ahead of its eVTOL integration.

* Premium Infrastructure (Delta Air Lines): Backed by Delta’s ongoing capital injections (including a $70 million warrant exercise in January 2026), Joby has secured a beachhead in the high-net-worth airport transfer market, solving critical "where to land" infrastructural bottlenecks.

Financial Health & Capital Allocation Efficiency

An analysis of Joby’s 2025 financials reveals a classic "high cash burn, pre-revenue" profile, though management has optimized its capital allocation efficiency to weather the certification cycle.

While Joby reported a 2025 net loss of $929.8 million (up 53% year-over-year), this figure masks underlying strategic investments. Research and development (R&D) constituted over 75% of operating expenses ($581 million), directly funding the FAA Stage 4 certification push. Concurrently, selling, general, and administrative (SG&A) expenses surged by 36%, reflecting the Blade integration and early commercialization groundwork.

Crucially, Joby has shielded itself against near-term liquidity crises. By raising approximately $1.3 billion in early 2026 through a public stock offering and convertible senior notes, the company extended its financial runway. Even under conservative HDIN Research estimates of a $50–$60 million monthly cash burn rate as high-rate production scales, this ~$2.7 billion liquidity pool ensures operational viability for up to 45 months, fully bridging the gap to the 2026 commercial launch.

Industry Outlook & Cyclical Headwinds

Despite holding pole position—having completed the first three stages of FAA Type Certification and crossing the 50% threshold for Stage 4 (Testing & Analysis)—Joby remains exposed to unique industry headwinds:

* Regulatory & Vertiport Bottlenecks: The FAA's late-2024 issuance of Special Federal Aviation Regulations (SFARs) for the "powered-lift" category necessitates ongoing operational adjustments. Furthermore, navigating fragmented local zoning laws for vertiports and mitigating community noise concerns remain critical barriers to network density.

* Technological & Supply Chain Vulnerabilities: Achieving profitable unit economics is highly contingent on the continuous improvement of lithium-ion battery energy density. Additionally, Joby’s supply chain, heavily reliant on aerospace-grade carbon fiber and specific battery components, remains vulnerable to geopolitical tariff shifts.

* "Soft" Backlogs: While Joby boasts a potential $1.25 billion in international orders (e.g., MOUs with Saudi Arabia's ALJ and Kazakhstan's Alatau Advance Air), these remain non-binding. Translating these into hard revenue relies entirely on global regulatory reciprocity and the successful ramp-up of the Ohio manufacturing hub.

HDIN Viewpoint: The Ultimate Race Against the Clock

HDIN Research views Joby Aviation's current trajectory as a high-stakes race between capital consumption and regulatory milestones. The company's deep vertical integration—manufacturing its own flight computers, electric propulsion units (EPUs), and battery packs—has created a profound technological moat, evidenced by its NASA-validated 65 dBA acoustic profile and its aggressive defense of intellectual property (notably, the November 2025 trade secret lawsuit against Archer Aviation).

However, institutional investors must remain vigilant regarding balance sheet volatility. With substantial liabilities tied to earnout shares and warrants (which drove $212 million in non-cash losses in 2025), Joby's bottom line is highly sensitive to equity fluctuations. Ultimately, the company has engineered an impeccable pre-commercial setup. Its valuation realization now hinges entirely on executing an undeniable paradigm shift: launching its first commercial passenger flights in Dubai or New York in 2026 without further regulatory or manufacturing delays.

Presentation download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Joby Aviation: FY2025 Performance & The Path to 2026 Commercialization

Strategic Pivots: Forging an Unassailable EcosystemJoby’s sector positioning is defined by a "manufacturing-traffic-infrastructure" trinity, carefully de-risked through blue-chip alliances. This strategic moat effectively addresses the fundamental challenges of scaling a novel transportation network:

* Manufacturing Scalability (Toyota): Solving the "how to build" equation, Toyota’s $650 million cumulative investment and deep integration into Joby’s manufacturing layout ensure automotive-grade reliability. The January 2026 acquisition of a 728,000-square-foot facility in Vandalia, Ohio, marks the essential leap from low-rate prototyping in California to high-rate industrial production.

* Customer Acquisition & Software Ecosystem (Uber & Blade): The integration of Uber’s demand-aggregation platform drastically lowers customer acquisition costs (CAC). Furthermore, the August 2025 acquisition of Blade’s passenger operations immediately secured key airspace access in New York and generated $34.8 million in passenger revenue. This operational "sandbox" allows Joby to stress-test its proprietary *Elevate OS* platform ahead of its eVTOL integration.

* Premium Infrastructure (Delta Air Lines): Backed by Delta’s ongoing capital injections (including a $70 million warrant exercise in January 2026), Joby has secured a beachhead in the high-net-worth airport transfer market, solving critical "where to land" infrastructural bottlenecks.

Financial Health & Capital Allocation Efficiency

An analysis of Joby’s 2025 financials reveals a classic "high cash burn, pre-revenue" profile, though management has optimized its capital allocation efficiency to weather the certification cycle.

While Joby reported a 2025 net loss of $929.8 million (up 53% year-over-year), this figure masks underlying strategic investments. Research and development (R&D) constituted over 75% of operating expenses ($581 million), directly funding the FAA Stage 4 certification push. Concurrently, selling, general, and administrative (SG&A) expenses surged by 36%, reflecting the Blade integration and early commercialization groundwork.

Crucially, Joby has shielded itself against near-term liquidity crises. By raising approximately $1.3 billion in early 2026 through a public stock offering and convertible senior notes, the company extended its financial runway. Even under conservative HDIN Research estimates of a $50–$60 million monthly cash burn rate as high-rate production scales, this ~$2.7 billion liquidity pool ensures operational viability for up to 45 months, fully bridging the gap to the 2026 commercial launch.

Industry Outlook & Cyclical Headwinds

Despite holding pole position—having completed the first three stages of FAA Type Certification and crossing the 50% threshold for Stage 4 (Testing & Analysis)—Joby remains exposed to unique industry headwinds:

* Regulatory & Vertiport Bottlenecks: The FAA's late-2024 issuance of Special Federal Aviation Regulations (SFARs) for the "powered-lift" category necessitates ongoing operational adjustments. Furthermore, navigating fragmented local zoning laws for vertiports and mitigating community noise concerns remain critical barriers to network density.

* Technological & Supply Chain Vulnerabilities: Achieving profitable unit economics is highly contingent on the continuous improvement of lithium-ion battery energy density. Additionally, Joby’s supply chain, heavily reliant on aerospace-grade carbon fiber and specific battery components, remains vulnerable to geopolitical tariff shifts.

* "Soft" Backlogs: While Joby boasts a potential $1.25 billion in international orders (e.g., MOUs with Saudi Arabia's ALJ and Kazakhstan's Alatau Advance Air), these remain non-binding. Translating these into hard revenue relies entirely on global regulatory reciprocity and the successful ramp-up of the Ohio manufacturing hub.

HDIN Viewpoint: The Ultimate Race Against the Clock

HDIN Research views Joby Aviation's current trajectory as a high-stakes race between capital consumption and regulatory milestones. The company's deep vertical integration—manufacturing its own flight computers, electric propulsion units (EPUs), and battery packs—has created a profound technological moat, evidenced by its NASA-validated 65 dBA acoustic profile and its aggressive defense of intellectual property (notably, the November 2025 trade secret lawsuit against Archer Aviation).

However, institutional investors must remain vigilant regarding balance sheet volatility. With substantial liabilities tied to earnout shares and warrants (which drove $212 million in non-cash losses in 2025), Joby's bottom line is highly sensitive to equity fluctuations. Ultimately, the company has engineered an impeccable pre-commercial setup. Its valuation realization now hinges entirely on executing an undeniable paradigm shift: launching its first commercial passenger flights in Dubai or New York in 2026 without further regulatory or manufacturing delays.

Presentation download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com