QuantumScape (QS) vs. Solid Power: Deciphering the Strategic Moats of the Solid-State Battery Race in 2025

Date : 2026-03-03

Reading : 1832

The commercialization of solid-state batteries (SSBs) has officially transitioned from laboratory prototypes to a high-stakes industrialization phase. Based on a penetrative analysis of the 2025 annual reports from QuantumScape (QS) and Solid Power (SLDP), HDIN Research has identified a stark divergence in how these two industry leaders are navigating cyclical headwinds and scaling challenges. Rather than engaging in a race to the bottom against low-cost, traditional lithium-ion supply chains, QS and SLDP are constructing distinct strategic moats: QS is pursuing a paradigm-shifting "Performance Leap" fueled by aggressive capital deployment, while SLDP is leveraging "Capital-Light Licensing" and process compatibility to accelerate market penetration.

Figure The Solid-State Battery Race QuantumScape vs Solid Power (2025 Year-End Report)

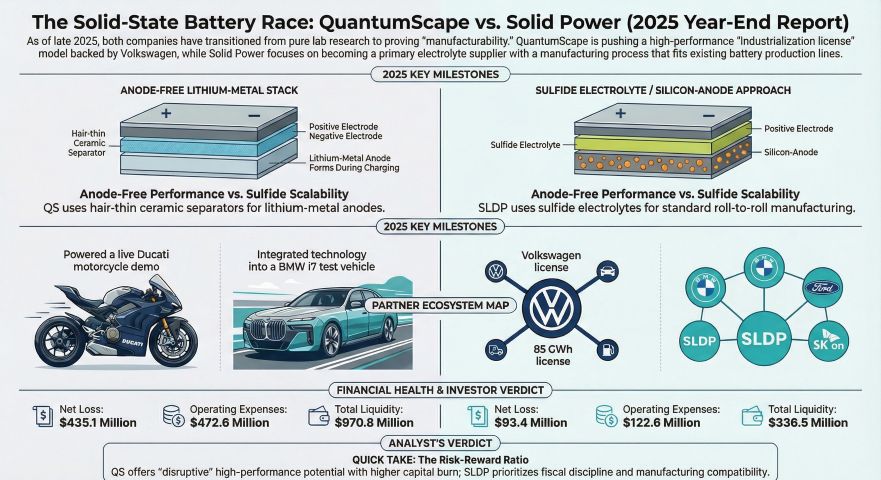

Strategic Moats: Anode-Free Disruption vs. Process Compatibility

Strategic Moats: Anode-Free Disruption vs. Process Compatibility

The core technological divergence between the two firms dictates their entirely different go-to-market strategies and commercial positioning.

QuantumScape is engineering a structural disruption. By utilizing a proprietary, dense inorganic ceramic separator, QS enables an "anode-free" lithium-metal architecture. This design theoretically eliminates the cost of traditional anode active materials and manufacturing steps, intending to create a structural cost advantage at industrial scale. With target volumetric energy densities exceeding 800 Wh/L and sub-15-minute fast charging capabilities, QS is weaponizing technological generational gaps to capture premium EV and aerospace markets, effectively sidestepping direct price wars with incumbent lithium-ion cell manufacturers. Its recent B-sample (QSE-5) integration into a Ducati V21L prototype validates this high-performance trajectory.

Conversely, Solid Power is prioritizing supply chain enablement. Utilizing a sulfide-based electrolyte paired currently with silicon-based anodes, SLDP's strategic moat lies in process compatibility. Sulfide materials allow manufacturers to utilize standard, industry-proven roll-to-roll lithium-ion equipment. By eliminating the need for bespoke, capital-intensive manufacturing platforms, SLDP drastically lowers the barriers to entry for OEMs and Tier-1 suppliers. Its recent integration into the BMW i7 test fleet underscores the viability of this pragmatic, drop-in replacement approach.

Capital Allocation Efficiency and Financial Health

A granular review of 2025 financial performance reveals two entirely different risk-reward profiles and capital allocation efficiencies.

QS operates as a hyper-intensive, R&D-driven entity. In 2025, QS recorded zero revenue while burning through $375.6 million in R&D and $36.3 million in capital expenditures (CapEx), primarily to automate its San Jose pilot line. The company's $26.6 million write-off of property and equipment illustrates the rapid, often costly iteration cycles required to scale novel ceramic processing. While QS maintains a robust liquidity buffer of $970.8 million, its survival is deeply tethered to its joint industrialization agreement with Volkswagen’s PowerCo, which aims to unlock up to 85 GWh/year of capacity and $1.3 billion in milestone-driven royalty prepayments.

SLDP, displaying superior capital allocation efficiency, operates a capital-light model. By positioning itself as an upstream electrolyte material supplier and IP licensor, SLDP generated $21.75 million in revenue in 2025, largely driven by collaborative milestones with SK On and the U.S. Department of Energy (DOE). With a substantially lower R&D spend of $72.5 million and CapEx of just $10.2 million, SLDP’s cash burn rate ($73.4 million) is a fraction of QS’s. Backed by a diverse ecosystem of partners—including BMW, SK On, and Ford—SLDP is poised to transition into an operational cash-flow-generating entity much earlier in the cycle.

Sector Positioning and Cyclical Headwinds

Both firms must navigate severe cyclical headwinds and policy risks. The sunsetting of the Section 30D tax credits under the newly enacted One Big Beautiful Bill Act (OBBBA) in late 2025 compresses the near-term demand ceiling from auto OEMs. Furthermore, SLDP faces specific vulnerabilities regarding the continuity of its $50 million DOE grant amidst shifting government mandates.

To counteract these headwinds, sector positioning is critical. QS relies on a high-concentration, deep-integration model with Volkswagen, creating a "boom or bust" scenario contingent on PowerCo's ability to seamlessly ramp up new manufacturing architectures. SLDP mitigates demand shocks by structurally pivoting toward the South Korean battery ecosystem (securing supply agreements with SK On and Samsung SDI), establishing a geographical and strategic hedge against evolving global supply chain restrictions.

HDIN Viewpoint

From an institutional perspective, HDIN Research assesses that Solid Power's capital-light material supplier model offers superior near-term financial resilience. By monetizing its electrolyte supply ahead of full-scale cell commercialization, SLDP provides robust downside protection in an increasingly volatile macroeconomic EV environment.

However, QuantumScape represents the ultimate asymmetric risk asset. While its capital intensity is immense and its manufacturing yield bottlenecks remain a critical risk factor, QS possesses a deeper long-term economic moat. If QS successfully transitions its ceramic separator technology from pilot line to PowerCo’s gigafactories, its anode-free architecture will fundamentally rewrite battery BOM economics, granting QS unprecedented pricing power and establishing the benchmark for the next decade of energy storage.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure The Solid-State Battery Race QuantumScape vs Solid Power (2025 Year-End Report)

Strategic Moats: Anode-Free Disruption vs. Process CompatibilityThe core technological divergence between the two firms dictates their entirely different go-to-market strategies and commercial positioning.

QuantumScape is engineering a structural disruption. By utilizing a proprietary, dense inorganic ceramic separator, QS enables an "anode-free" lithium-metal architecture. This design theoretically eliminates the cost of traditional anode active materials and manufacturing steps, intending to create a structural cost advantage at industrial scale. With target volumetric energy densities exceeding 800 Wh/L and sub-15-minute fast charging capabilities, QS is weaponizing technological generational gaps to capture premium EV and aerospace markets, effectively sidestepping direct price wars with incumbent lithium-ion cell manufacturers. Its recent B-sample (QSE-5) integration into a Ducati V21L prototype validates this high-performance trajectory.

Conversely, Solid Power is prioritizing supply chain enablement. Utilizing a sulfide-based electrolyte paired currently with silicon-based anodes, SLDP's strategic moat lies in process compatibility. Sulfide materials allow manufacturers to utilize standard, industry-proven roll-to-roll lithium-ion equipment. By eliminating the need for bespoke, capital-intensive manufacturing platforms, SLDP drastically lowers the barriers to entry for OEMs and Tier-1 suppliers. Its recent integration into the BMW i7 test fleet underscores the viability of this pragmatic, drop-in replacement approach.

Capital Allocation Efficiency and Financial Health

A granular review of 2025 financial performance reveals two entirely different risk-reward profiles and capital allocation efficiencies.

QS operates as a hyper-intensive, R&D-driven entity. In 2025, QS recorded zero revenue while burning through $375.6 million in R&D and $36.3 million in capital expenditures (CapEx), primarily to automate its San Jose pilot line. The company's $26.6 million write-off of property and equipment illustrates the rapid, often costly iteration cycles required to scale novel ceramic processing. While QS maintains a robust liquidity buffer of $970.8 million, its survival is deeply tethered to its joint industrialization agreement with Volkswagen’s PowerCo, which aims to unlock up to 85 GWh/year of capacity and $1.3 billion in milestone-driven royalty prepayments.

SLDP, displaying superior capital allocation efficiency, operates a capital-light model. By positioning itself as an upstream electrolyte material supplier and IP licensor, SLDP generated $21.75 million in revenue in 2025, largely driven by collaborative milestones with SK On and the U.S. Department of Energy (DOE). With a substantially lower R&D spend of $72.5 million and CapEx of just $10.2 million, SLDP’s cash burn rate ($73.4 million) is a fraction of QS’s. Backed by a diverse ecosystem of partners—including BMW, SK On, and Ford—SLDP is poised to transition into an operational cash-flow-generating entity much earlier in the cycle.

Sector Positioning and Cyclical Headwinds

Both firms must navigate severe cyclical headwinds and policy risks. The sunsetting of the Section 30D tax credits under the newly enacted One Big Beautiful Bill Act (OBBBA) in late 2025 compresses the near-term demand ceiling from auto OEMs. Furthermore, SLDP faces specific vulnerabilities regarding the continuity of its $50 million DOE grant amidst shifting government mandates.

To counteract these headwinds, sector positioning is critical. QS relies on a high-concentration, deep-integration model with Volkswagen, creating a "boom or bust" scenario contingent on PowerCo's ability to seamlessly ramp up new manufacturing architectures. SLDP mitigates demand shocks by structurally pivoting toward the South Korean battery ecosystem (securing supply agreements with SK On and Samsung SDI), establishing a geographical and strategic hedge against evolving global supply chain restrictions.

HDIN Viewpoint

From an institutional perspective, HDIN Research assesses that Solid Power's capital-light material supplier model offers superior near-term financial resilience. By monetizing its electrolyte supply ahead of full-scale cell commercialization, SLDP provides robust downside protection in an increasingly volatile macroeconomic EV environment.

However, QuantumScape represents the ultimate asymmetric risk asset. While its capital intensity is immense and its manufacturing yield bottlenecks remain a critical risk factor, QS possesses a deeper long-term economic moat. If QS successfully transitions its ceramic separator technology from pilot line to PowerCo’s gigafactories, its anode-free architecture will fundamentally rewrite battery BOM economics, granting QS unprecedented pricing power and establishing the benchmark for the next decade of energy storage.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com