Hasbro’s Leveraged Transformation: How Digital IP Monetization is Rewriting the Toy Industry Playbook

Date : 2026-03-05

Reading : 68

The Lead: Hasbro’s 2025 annual report reveals a tale of two deeply divergent business models. While capital allocation efficiency and aggressive IP monetization drove a staggering 44.7% revenue surge in its digital gaming segment, severe macroeconomic and tariff-induced headwinds forced a $1.02 billion goodwill impairment in its traditional toy division. The "So What" is clear: Hasbro is no longer just a physical toy manufacturer, but a digital entertainment ecosystem leaning heavily on its strategic moats in the adult gaming demographic to fund a costly structural pivot.

Based on an in-depth analysis of Hasbro’s 2025 and early 2026 financial disclosures, HDIN Research has unpacked the underlying mechanics of this strategic transformation.

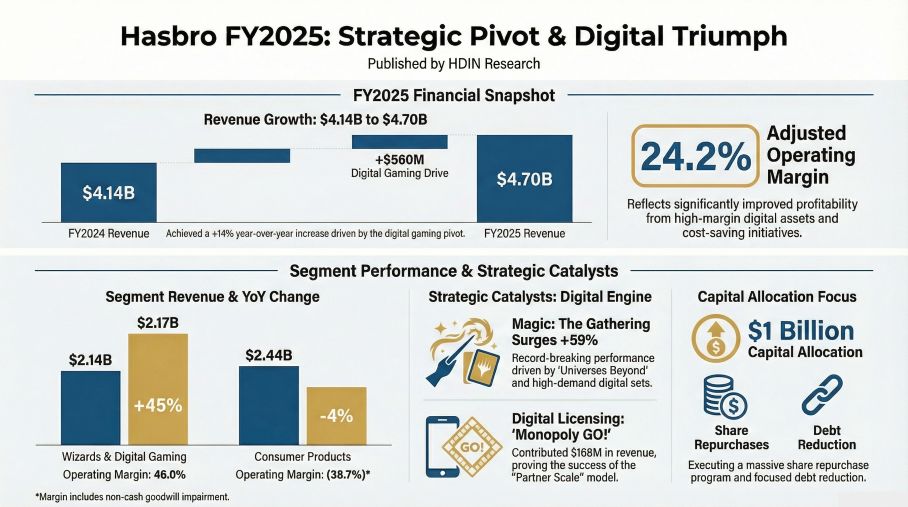

Figure Hasbro FY2025: Strategic Pivot & Digital Triumph

Strategic Pivots: The Transition to Asset-Light IP Monetization

Strategic Pivots: The Transition to Asset-Light IP Monetization

Hasbro’s "Playing to Win" strategy has effectively shifted the company’s core growth engine from high-inventory physical goods to high-margin, asset-light digital intellectual property. The Wizards of the Coast (WotC) and Digital Gaming segment generated $2.187 billion in net revenue, boasting a massive 46.0% operating margin.

This is not merely a product of organic market expansion; it is driven by a deliberate "Universes Beyond" strategy. By integrating premium external IPs—such as Final Fantasy and Marvel—into Magic: The Gathering, Hasbro has deepened its penetration into the highly lucrative "Kidult" (adult collector) demographic. Furthermore, strategic licensing partnerships have provided exceptional operational leverage. For instance, the mobile game *Monopoly Go!* (developed by Scopely) contributed $168 million in high-margin royalty revenue in 2025. This underscores how Hasbro is successfully extracting long-tail value from its proprietary IP catalog with minimal capital expenditure.

Cyclical Headwinds and the $1 Billion Structural Reset

While the digital segment thrives, the traditional Consumer Products division remains heavily exposed to cyclical headwinds. In 2025, the segment's revenue declined by 4.2% to $2.438 billion. More critically, Hasbro recorded a $1.02 billion non-cash goodwill impairment for this division.

This impairment is not a temporary blip; it is a structural reset of the balance sheet. High inflation has compressed discretionary consumer spending, while geopolitical uncertainties have severely disrupted supply chain economics. In 2025, Hasbro absorbed $44.9 million in direct tariff costs. These tariff threats fundamentally altered vendor behavior, forcing retail partners to shift from "Direct Import" to "Domestic Orders." Consequently, Hasbro was forced to internalize heightened warehousing and logistics costs, severely squeezing profit margins. To build supply chain resilience and de-risk its operations, the company is actively executing near-shoring and capacity-shifting strategies toward Mexico, Vietnam, and India.

Financial Health: AI Integration and Capital Allocation Efficiency

Despite a net loss of $322 million in 2025—largely driven by the aforementioned impairment—Hasbro's underlying cash flow mechanics show signs of disciplined recovery. The company's "Operational Excellence Program" has already delivered nearly $800 million in gross cost savings, tracking steadily toward a $1 billion target.

A key driver of this efficiency is the aggressive integration of Artificial Intelligence (AI). Hasbro is deploying AI to accelerate time-to-market via rapid prototyping and engineering design, while also leveraging AI-driven analytics for precise Direct-to-Consumer (D2C) marketing on platforms like Hasbro Pulse.

However, financial flexibility remains tightly constrained. Hasbro currently carries $3.28 billion in long-term debt, generating $163 million in annual interest expenses. A potential tailwind has emerged in early 2026: following a February 2026 Supreme Court ruling against the IEEPA tariffs, Hasbro is actively exploring retroactive refunds for the $44.9 million in tariffs paid since April 2025. While this cash injection would provide tactical relief, the company's long-term financial health hinges on sustaining digital revenue growth.

Industry Outlook: The 2027 R&D Gamble

Hasbro is fundamentally redefining its sector positioning. To capture market share in the heavy-gaming space, the company escalated its product development expenditures to $386 million in 2025. Hasbro now operates four internal studios developing AAA and AA titles, including the highly anticipated *EXODUS* and *WARLOCK: DUNGEONS & DRAGONS*, slated for 2027.

While this expands Hasbro's strategic moats, it introduces elevated capitalization risks. If these games fail to achieve "technological feasibility" or market traction, Hasbro faces the peril of future mega-write-offs.

HDIN Viewpoint

From an institutional perspective, HDIN Research assesses Hasbro’s current state as a "leveraged transformation." Management has successfully cleared the physical inventory backlog that plagued the industry in recent years, but they are still purging the balance sheet of legacy premium valuations.

Hasbro's future valuation will increasingly mirror that of a software and IP-licensing firm rather than a traditional manufacturer. The digital gaming operations are generating the necessary free cash flow to subsidize the structural overhaul of the physical supply chain. Moving forward, market participants must look beyond top-line revenue and critically monitor two metrics: the interest coverage ratio amidst high debt loads, and the developmental milestones of its internal AAA game studios. Only by translating heavy R&D CapEx into recurring digital cash flows can Hasbro permanently insulate itself from macroeconomic retail volatility.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on an in-depth analysis of Hasbro’s 2025 and early 2026 financial disclosures, HDIN Research has unpacked the underlying mechanics of this strategic transformation.

Figure Hasbro FY2025: Strategic Pivot & Digital Triumph

Strategic Pivots: The Transition to Asset-Light IP MonetizationHasbro’s "Playing to Win" strategy has effectively shifted the company’s core growth engine from high-inventory physical goods to high-margin, asset-light digital intellectual property. The Wizards of the Coast (WotC) and Digital Gaming segment generated $2.187 billion in net revenue, boasting a massive 46.0% operating margin.

This is not merely a product of organic market expansion; it is driven by a deliberate "Universes Beyond" strategy. By integrating premium external IPs—such as Final Fantasy and Marvel—into Magic: The Gathering, Hasbro has deepened its penetration into the highly lucrative "Kidult" (adult collector) demographic. Furthermore, strategic licensing partnerships have provided exceptional operational leverage. For instance, the mobile game *Monopoly Go!* (developed by Scopely) contributed $168 million in high-margin royalty revenue in 2025. This underscores how Hasbro is successfully extracting long-tail value from its proprietary IP catalog with minimal capital expenditure.

Cyclical Headwinds and the $1 Billion Structural Reset

While the digital segment thrives, the traditional Consumer Products division remains heavily exposed to cyclical headwinds. In 2025, the segment's revenue declined by 4.2% to $2.438 billion. More critically, Hasbro recorded a $1.02 billion non-cash goodwill impairment for this division.

This impairment is not a temporary blip; it is a structural reset of the balance sheet. High inflation has compressed discretionary consumer spending, while geopolitical uncertainties have severely disrupted supply chain economics. In 2025, Hasbro absorbed $44.9 million in direct tariff costs. These tariff threats fundamentally altered vendor behavior, forcing retail partners to shift from "Direct Import" to "Domestic Orders." Consequently, Hasbro was forced to internalize heightened warehousing and logistics costs, severely squeezing profit margins. To build supply chain resilience and de-risk its operations, the company is actively executing near-shoring and capacity-shifting strategies toward Mexico, Vietnam, and India.

Financial Health: AI Integration and Capital Allocation Efficiency

Despite a net loss of $322 million in 2025—largely driven by the aforementioned impairment—Hasbro's underlying cash flow mechanics show signs of disciplined recovery. The company's "Operational Excellence Program" has already delivered nearly $800 million in gross cost savings, tracking steadily toward a $1 billion target.

A key driver of this efficiency is the aggressive integration of Artificial Intelligence (AI). Hasbro is deploying AI to accelerate time-to-market via rapid prototyping and engineering design, while also leveraging AI-driven analytics for precise Direct-to-Consumer (D2C) marketing on platforms like Hasbro Pulse.

However, financial flexibility remains tightly constrained. Hasbro currently carries $3.28 billion in long-term debt, generating $163 million in annual interest expenses. A potential tailwind has emerged in early 2026: following a February 2026 Supreme Court ruling against the IEEPA tariffs, Hasbro is actively exploring retroactive refunds for the $44.9 million in tariffs paid since April 2025. While this cash injection would provide tactical relief, the company's long-term financial health hinges on sustaining digital revenue growth.

Industry Outlook: The 2027 R&D Gamble

Hasbro is fundamentally redefining its sector positioning. To capture market share in the heavy-gaming space, the company escalated its product development expenditures to $386 million in 2025. Hasbro now operates four internal studios developing AAA and AA titles, including the highly anticipated *EXODUS* and *WARLOCK: DUNGEONS & DRAGONS*, slated for 2027.

While this expands Hasbro's strategic moats, it introduces elevated capitalization risks. If these games fail to achieve "technological feasibility" or market traction, Hasbro faces the peril of future mega-write-offs.

HDIN Viewpoint

From an institutional perspective, HDIN Research assesses Hasbro’s current state as a "leveraged transformation." Management has successfully cleared the physical inventory backlog that plagued the industry in recent years, but they are still purging the balance sheet of legacy premium valuations.

Hasbro's future valuation will increasingly mirror that of a software and IP-licensing firm rather than a traditional manufacturer. The digital gaming operations are generating the necessary free cash flow to subsidize the structural overhaul of the physical supply chain. Moving forward, market participants must look beyond top-line revenue and critically monitor two metrics: the interest coverage ratio amidst high debt loads, and the developmental milestones of its internal AAA game studios. Only by translating heavy R&D CapEx into recurring digital cash flows can Hasbro permanently insulate itself from macroeconomic retail volatility.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com