Genori Technology: Deconstructing the Strategic Moats and Cyclical Headwinds of a Semiconductor Parts Leader

Date : 2026-03-04

Reading : 126

While Genori Technology has quietly secured the top market share in China’s direct-to-fab non-metallic semiconductor components sector, its headline-grabbing 48.47% gross margin in H1 2025 warrants deeper institutional scrutiny. Beyond the impressive revenue surge—reaching $88.74 million in 2024—the true narrative lies in how the company's vertical integration strategy and direct-to-fab supply model are reshaping its pricing power. However, as Genori pivots toward high-barrier core modules, HDIN Research's analysis reveals that upcoming capital expenditure depreciation and accounting complexities may test the company's long-term capital allocation efficiency.

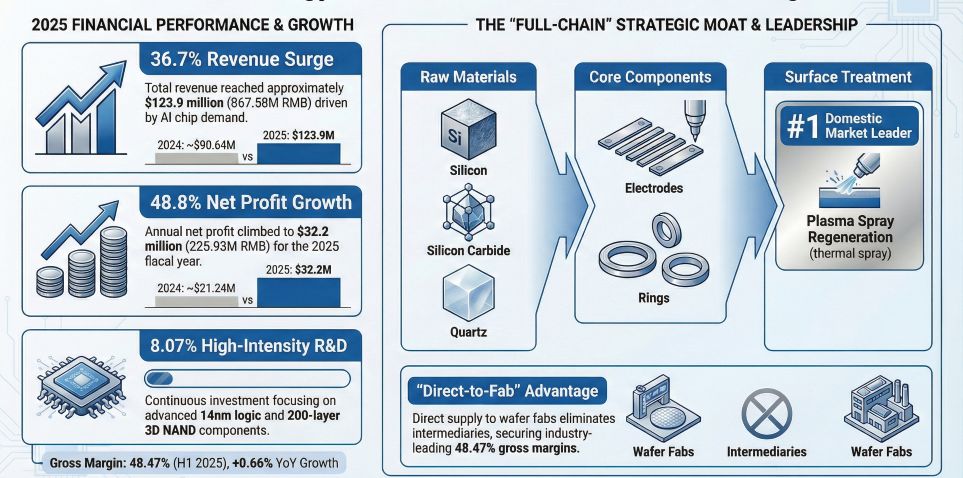

Figure Genori Technology: 2025 Annual Performance & Strategic Moat

Sector Positioning: The Direct-to-Fab Advantage

Sector Positioning: The Direct-to-Fab Advantage

Genori Technology has established a formidable presence in the domestic semiconductor equipment supply chain, ranking first among local enterprises in both quartz (8.8% market share) and silicon (4.5% market share) direct-to-fab supply in 2024.

The strategic implication here is profound: rather than acting as an OEM for Tier-1 equipment manufacturers, Genori bypasses the middlemen through a "Direct-to-Fab" model. By supplying directly to top-tier wafer foundries—penetrating 14nm logic nodes and 200+ layer 3D NAND processes—the company captures the lucrative premium of the consumable replacement market. This structural advantage explains why Genori’s comprehensive gross margin hit an industry-leading 48.47% in H1 2025, significantly outpacing peers operating under traditional OEM constraints.

Strategic Moats: Vertical Integration and Capacity Dynamics

Genori’s primary competitive moat is its comprehensive "Raw Materials + Components + Surface Treatment" vertical integration platform. By manufacturing large-diameter monocrystalline silicon ingots and CVD high-purity silicon carbide in-house, the company effectively insulates itself from upstream supply chain disruptions and raw material cost volatility.

Operationally, the firm is experiencing exceptional demand elasticity. Capacity utilization rates surged to 103.97% in H1 2025, indicating that existing production lines are operating beyond maximum theoretical limits. This acute capacity bottleneck provides the strategic rationale for its aggressive CapEx expansion, validating that the recent infrastructure investments are driven by tangible market pull rather than speculative capacity hoarding.

Financial Health: Capital Allocation Efficiency and Underlying Risks

Despite robust top-line growth, HDIN Research's stress-testing uncovers potential liquidity and earnings quality vulnerabilities. The company's accounts receivable turnover ratio decelerated to 1.52 (unannualized) in H1 2025, with AR balances accounting for over 70% of half-year revenue. With the top five customers generating over 71% of total sales, Genori faces an asymmetric bargaining dynamic. Any cyclical headwinds or geopolitical sanctions forcing downstream fabs to lower their utilization rates could trigger an immediate liquidity squeeze.

Furthermore, capital allocation efficiency requires close monitoring. A surge in "Long-Term Deferred Expenses" (reaching $20.79 million in mid-2025) suggests that significant R&D infrastructure costs—such as the construction of high-grade cleanrooms—are being capitalized and amortized over long periods. While legally compliant, this accounting treatment filters out heavy short-term cash outflows, artificially buffering the current operating profit margins.

Strategic Pivots: The ESC Transition Amid Cyclical Headwinds

To transition from a supplier of low-barrier consumable parts to a provider of high-value core modules, Genori is heavily investing in next-generation technologies like Electrostatic Chucks (ESC) and Aluminum Nitride (AlN) heaters. Backed by its new Shanghai R&D center, the company aims to break the oligopoly held by US and Japanese giants.

However, this strategic pivot introduces significant execution risk. The ESC project remains in the R&D and pilot-testing phase. Following the implementation of its $179.49 million planned investments, the peak annual depreciation of fixed assets could exceed $10 million. If commercialization of the ESC modules is delayed, the dual pressures of intense low-end price wars and surging depreciation costs could severely compress future profit margins.

HDIN Viewpoint

HDIN Research believes that Genori Technology is a textbook beneficiary of the domestic semiconductor substitution wave, leveraging an optimized business model to achieve exceptional mid-cycle profitability. Their vertical integration provides a resilient shield against supply shocks. However, the ultimate barometer of Genori’s transition from a regional parts processor to a global module powerhouse will be the successful yield and fab-certification of its ESC products over the next 12 to 24 months. Investors must weigh the company's undeniable technological momentum against the tightening cash flow cycles and upcoming CapEx depreciation cliffs.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Genori Technology: 2025 Annual Performance & Strategic Moat

Sector Positioning: The Direct-to-Fab AdvantageGenori Technology has established a formidable presence in the domestic semiconductor equipment supply chain, ranking first among local enterprises in both quartz (8.8% market share) and silicon (4.5% market share) direct-to-fab supply in 2024.

The strategic implication here is profound: rather than acting as an OEM for Tier-1 equipment manufacturers, Genori bypasses the middlemen through a "Direct-to-Fab" model. By supplying directly to top-tier wafer foundries—penetrating 14nm logic nodes and 200+ layer 3D NAND processes—the company captures the lucrative premium of the consumable replacement market. This structural advantage explains why Genori’s comprehensive gross margin hit an industry-leading 48.47% in H1 2025, significantly outpacing peers operating under traditional OEM constraints.

Strategic Moats: Vertical Integration and Capacity Dynamics

Genori’s primary competitive moat is its comprehensive "Raw Materials + Components + Surface Treatment" vertical integration platform. By manufacturing large-diameter monocrystalline silicon ingots and CVD high-purity silicon carbide in-house, the company effectively insulates itself from upstream supply chain disruptions and raw material cost volatility.

Operationally, the firm is experiencing exceptional demand elasticity. Capacity utilization rates surged to 103.97% in H1 2025, indicating that existing production lines are operating beyond maximum theoretical limits. This acute capacity bottleneck provides the strategic rationale for its aggressive CapEx expansion, validating that the recent infrastructure investments are driven by tangible market pull rather than speculative capacity hoarding.

Financial Health: Capital Allocation Efficiency and Underlying Risks

Despite robust top-line growth, HDIN Research's stress-testing uncovers potential liquidity and earnings quality vulnerabilities. The company's accounts receivable turnover ratio decelerated to 1.52 (unannualized) in H1 2025, with AR balances accounting for over 70% of half-year revenue. With the top five customers generating over 71% of total sales, Genori faces an asymmetric bargaining dynamic. Any cyclical headwinds or geopolitical sanctions forcing downstream fabs to lower their utilization rates could trigger an immediate liquidity squeeze.

Furthermore, capital allocation efficiency requires close monitoring. A surge in "Long-Term Deferred Expenses" (reaching $20.79 million in mid-2025) suggests that significant R&D infrastructure costs—such as the construction of high-grade cleanrooms—are being capitalized and amortized over long periods. While legally compliant, this accounting treatment filters out heavy short-term cash outflows, artificially buffering the current operating profit margins.

Strategic Pivots: The ESC Transition Amid Cyclical Headwinds

To transition from a supplier of low-barrier consumable parts to a provider of high-value core modules, Genori is heavily investing in next-generation technologies like Electrostatic Chucks (ESC) and Aluminum Nitride (AlN) heaters. Backed by its new Shanghai R&D center, the company aims to break the oligopoly held by US and Japanese giants.

However, this strategic pivot introduces significant execution risk. The ESC project remains in the R&D and pilot-testing phase. Following the implementation of its $179.49 million planned investments, the peak annual depreciation of fixed assets could exceed $10 million. If commercialization of the ESC modules is delayed, the dual pressures of intense low-end price wars and surging depreciation costs could severely compress future profit margins.

HDIN Viewpoint

HDIN Research believes that Genori Technology is a textbook beneficiary of the domestic semiconductor substitution wave, leveraging an optimized business model to achieve exceptional mid-cycle profitability. Their vertical integration provides a resilient shield against supply shocks. However, the ultimate barometer of Genori’s transition from a regional parts processor to a global module powerhouse will be the successful yield and fab-certification of its ESC products over the next 12 to 24 months. Investors must weigh the company's undeniable technological momentum against the tightening cash flow cycles and upcoming CapEx depreciation cliffs.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com