2025 Global Generics Industry Analysis: The Strategic Pivot from Scale to Value

Date : 2026-03-05

Reading : 222

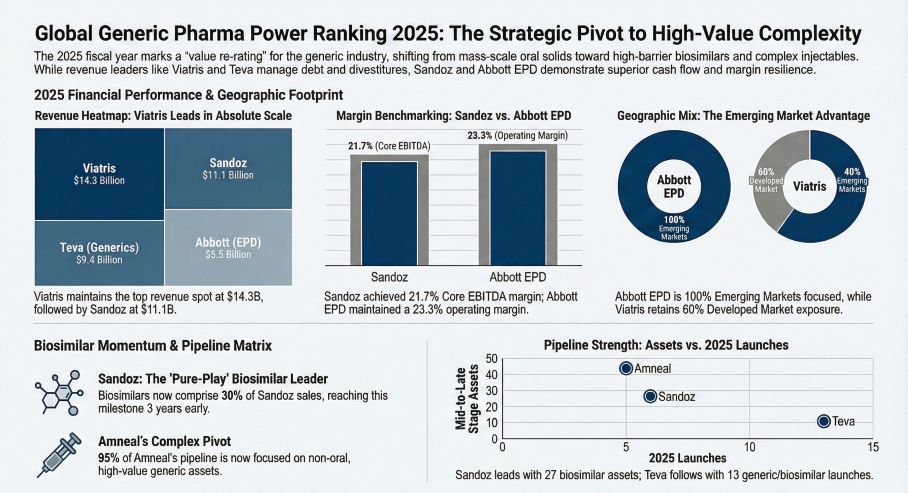

According to the latest financial audit by HDIN Research, leading pharmaceutical entities are aggressively decoupling from low-margin oral solid dosages to fortify positions in biosimilars and complex injectables. Our analysis of FY2025 data from major players—including Sandoz, Teva, and Abbott (EPD)—reveals that operational resilience and capital allocation efficiency have replaced revenue scale as the primary determinants of valuation.

Figure Global Generic Pharma Power Ranking 2025: The Strategic Pivot to High-Value Complexity

The Rise of Technical Moats: Biosimilars and Complex Generics

The Rise of Technical Moats: Biosimilars and Complex Generics

The commoditization of traditional generics has forced a structural migration toward assets with high technical and regulatory barriers. The market is no longer rewarding breadth of portfolio, but rather depth of technical capability.

* Sandoz’s “Pure Play” Advantage: Following its spinoff, Sandoz has leveraged its vertical integration to achieve a 30% revenue contribution from biosimilars ahead of schedule. Their $1.1 billion investment in Slovenia represents a strategic "capacity moat," insulating them from the supply chain volatilities plaguing competitors.

* Amneal’s Complex Pivot: Amneal Pharmaceuticals has effectively exited the "race to the bottom" by orienting 95% of its pipeline toward non-oral complex generics (injectables, ophthalmics). This "First-to-File" strategy is not merely about speed; it is about engineering capability serving as a barrier to entry against lower-cost overseas manufacturers.

Financial Health: The Great Deleveraging and Asset Repricing

The macroeconomic environment of 2025 has punished companies carrying historical debt loads while rewarding those with pristine balance sheets. HDIN Research identifies a stark bifurcation in financial resilience:

* Capital Allocation Efficiency: Abbott (EPD) and Sandoz have emerged as "Cash Conversions Leaders." Abbott’s negligible leverage ratio (0.4x Net Debt/EBITDA) allows for opportunistic cross-sector acquisitions, while Sandoz generates superior operating cash flow relative to net income.

* Valuation Reality Checks: Conversely, the industry is witnessing a "clearing event" for historical over-optimism. Viatris’s $2.94 billion goodwill impairment signals a painful but necessary recalibration of asset values in response to higher discount rates and pricing erosion. Similarly, highly leveraged entities like Bausch Health are seeing operating cash flows consumed almost entirely by debt service, limiting their ability to reinvest in R&D.

Navigating Policy Headwinds: The IRA and VBP Effect

External regulatory pressures are reshaping geographic and product strategies. The *Inflation Reduction Act* (IRA) in the US and *Volume-Based Procurement* (VBP) in China have effectively capped the upside for mature assets.

* The "Compliance" Premium: Supply chain localization is becoming a tangible asset. Amneal, with 46% of its revenue derived from US domestic production, enjoys a "compliance premium" and supply certainty. In contrast, competitors relying heavily on offshore manufacturing, such as Viatris with its Indore facility challenges, faced revenue erosion due to regulatory import bans.

* Strategic Geographic Isolation: Companies are adopting distinct strategies to mitigate policy risk. Abbott EPD has successfully insulated itself from US pricing pressure by focusing 100% on emerging markets, capitalizing on "Branded Generic" equity that bypasses the commoditized hospital tender channels dominated by VBP.

HDIN Viewpoint: Operational Transparency is Key

At HDIN Research, we caution investors to look beyond "Adjusted EBITDA" metrics. A recurring trend in 2025 is the normalization of "restructuring charges" by legacy giants like Teva and Viatris. When one-off costs become annual occurrences, they must be viewed as operational expenses rather than strategic pivots.

Furthermore, the winners of the next cycle will be determined by Compliance Governance. As the FDA intensifies scrutiny under GDUFA III, the ability to maintain a "clean" manufacturing network is no longer just a regulatory requirement—it is a competitive advantage that directly correlates with market share stability and gross margin preservation.

Download Presentation

Click the PDF download link under “Related Topics” to access the presentation of this report.

Watch Video

Click this link to watch the YouTube video summarizing the 2025 Generics Industry trends.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Global Generic Pharma Power Ranking 2025: The Strategic Pivot to High-Value Complexity

The Rise of Technical Moats: Biosimilars and Complex GenericsThe commoditization of traditional generics has forced a structural migration toward assets with high technical and regulatory barriers. The market is no longer rewarding breadth of portfolio, but rather depth of technical capability.

* Sandoz’s “Pure Play” Advantage: Following its spinoff, Sandoz has leveraged its vertical integration to achieve a 30% revenue contribution from biosimilars ahead of schedule. Their $1.1 billion investment in Slovenia represents a strategic "capacity moat," insulating them from the supply chain volatilities plaguing competitors.

* Amneal’s Complex Pivot: Amneal Pharmaceuticals has effectively exited the "race to the bottom" by orienting 95% of its pipeline toward non-oral complex generics (injectables, ophthalmics). This "First-to-File" strategy is not merely about speed; it is about engineering capability serving as a barrier to entry against lower-cost overseas manufacturers.

Financial Health: The Great Deleveraging and Asset Repricing

The macroeconomic environment of 2025 has punished companies carrying historical debt loads while rewarding those with pristine balance sheets. HDIN Research identifies a stark bifurcation in financial resilience:

* Capital Allocation Efficiency: Abbott (EPD) and Sandoz have emerged as "Cash Conversions Leaders." Abbott’s negligible leverage ratio (0.4x Net Debt/EBITDA) allows for opportunistic cross-sector acquisitions, while Sandoz generates superior operating cash flow relative to net income.

* Valuation Reality Checks: Conversely, the industry is witnessing a "clearing event" for historical over-optimism. Viatris’s $2.94 billion goodwill impairment signals a painful but necessary recalibration of asset values in response to higher discount rates and pricing erosion. Similarly, highly leveraged entities like Bausch Health are seeing operating cash flows consumed almost entirely by debt service, limiting their ability to reinvest in R&D.

Navigating Policy Headwinds: The IRA and VBP Effect

External regulatory pressures are reshaping geographic and product strategies. The *Inflation Reduction Act* (IRA) in the US and *Volume-Based Procurement* (VBP) in China have effectively capped the upside for mature assets.

* The "Compliance" Premium: Supply chain localization is becoming a tangible asset. Amneal, with 46% of its revenue derived from US domestic production, enjoys a "compliance premium" and supply certainty. In contrast, competitors relying heavily on offshore manufacturing, such as Viatris with its Indore facility challenges, faced revenue erosion due to regulatory import bans.

* Strategic Geographic Isolation: Companies are adopting distinct strategies to mitigate policy risk. Abbott EPD has successfully insulated itself from US pricing pressure by focusing 100% on emerging markets, capitalizing on "Branded Generic" equity that bypasses the commoditized hospital tender channels dominated by VBP.

HDIN Viewpoint: Operational Transparency is Key

At HDIN Research, we caution investors to look beyond "Adjusted EBITDA" metrics. A recurring trend in 2025 is the normalization of "restructuring charges" by legacy giants like Teva and Viatris. When one-off costs become annual occurrences, they must be viewed as operational expenses rather than strategic pivots.

Furthermore, the winners of the next cycle will be determined by Compliance Governance. As the FDA intensifies scrutiny under GDUFA III, the ability to maintain a "clean" manufacturing network is no longer just a regulatory requirement—it is a competitive advantage that directly correlates with market share stability and gross margin preservation.

Download Presentation

Click the PDF download link under “Related Topics” to access the presentation of this report.

Watch Video

Click this link to watch the YouTube video summarizing the 2025 Generics Industry trends.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com