Metal Packaging 2025: The Race for Green Premiums & Capital Efficiency

Date : 2026-03-05

Reading : 131

The 2025 fiscal landscape for the global metal packaging triumvirate—Ball Corporation, Crown Holdings, and Silgan Holdings—reveals a definitive strategic pivot. Beyond standard volume metrics, the industry is currently defined by a structural "Substrate Shift" from plastic to aluminum and the rigorous application of cost pass-through mechanisms. While macroeconomic headwinds persist, HDIN Research identifies that the true competitive edge has migrated from simple capacity expansion to capital allocation efficiency and the monetization of sustainability.

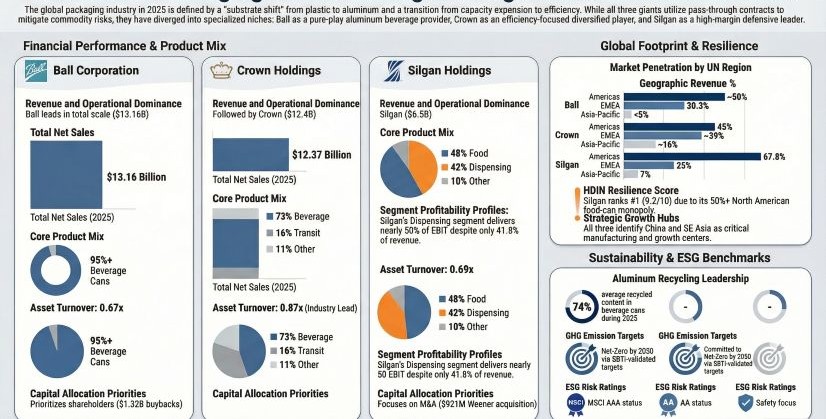

Figure 2025 Global MetalPackaging Giants: Strategic Divergence & Financial Resilience

Strategic Divergence in Asset Allocation

Strategic Divergence in Asset Allocation

While all three giants benefit from the "infinite recyclability" narrative of metal packaging, their 2025 asset structures highlight distinct strategic identities:

* Ball Corporation ( The Pure-Play Scale Operator): Following the divestment of its aerospace division, Ball has doubled down on becoming a pure-play aluminum powerhouse. With over 95% of its core business focused on beverage packaging, Ball is betting entirely on the displacement of PET plastic. However, this focus creates a high sensitivity to volume fluctuations within the beverage sector.

* Crown Holdings (The Efficiency Engine): Crown differentiates itself through asset velocity. With an industry-leading asset turnover ratio (0.87x), Crown leverages a unique mix of consumer beverage cans and industrial "Transit Packaging." This dual engine allows Crown to capture upside during industrial expansion cycles while maintaining a steady baseline in consumer goods.

* Silgan Holdings (The Defensive Compounder): Silgan remains the "Defensive King." By holding a dominant >50% market share in North American metal food cans, Silgan creates a recession-proof cash flow floor. Furthermore, its aggressive M&A strategy—highlighted by the acquisition of Weener Packaging—signals a shift toward high-margin dispensing systems, moving the company up the value chain into beauty and healthcare.

The Pass-Through Shield: Neutralizing Commodity Volatility

A critical analysis of 2025 financials shows that raw material volatility (Aluminum and Steel) is no longer a primary threat to profitability, but rather a liquidity management challenge.

All three entities have successfully institutionalized "Pass-through Mechanisms." Financial disclosures indicate that the surge in nominal revenue for Ball and Crown was largely driven by the mathematical pass-through of higher aluminum costs to customers like Coca-Cola and AB InBev. For institutional investors, the "So What" is clear: Input cost risk is effectively neutralized. The analytical focus must now shift to "Lag Management"—how efficiently these companies manage the 1-3 month delay between cost spikes and contract price adjustments, and the resulting impact on quarterly working capital requirements.

HDIN Research Viewpoint: The Hidden Risks in Balance Sheets

While the operational narratives are robust, HDIN Research advises a more critical examination of the underlying quality of earnings and balance sheet health.

1. The Supply Chain Finance (SCF) "Red Flag": Our analysis flags a growing reliance on SCF programs, particularly within Silgan’s structure (approx. $438M balance). While this optimizes working capital optics, it can mask the true Days Payable Outstanding (DPO) and presents a liquidity risk should credit markets tighten.

2. Concentration Risk vs. Moat Durability: Ball Corporation’s reliance on its top three customers for nearly 40% of revenue presents a significant counterparty risk. In contrast, Silgan’s "Strategic Moat" in the food can sector offers superior downside protection. The high switching costs and long-term contracts (some extending to 2032) in the food sector provide a buffer that the more commoditized beverage can market lacks.

3. The "Green Premium" Reality: Sustainability is no longer just a compliance cost; it is a revenue driver. Ball and Crown’s aggressive Science-Based Targets (SBTi) and "Twentyby30" initiatives are securing them preferred supplier status with global FMCG giants. Investors should view R&D spend on lightweighting and circularity not as expenses, but as defensive capex against future carbon taxation.

HDIN Research Conclusion: For 2025-2026, the investment logic varies by risk appetite. Crown Holdings offers the best balance of efficiency and industrial upside; Silgan Holdings provides the strongest defensive shield against recessionary pressures; and Ball Corporation remains the high-beta play on the global adoption of aluminum.

Presentation Download

For a comprehensive breakdown of the financial ratios, regional growth engines, and our proprietary "Resilience Scoring" of these three giants:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global MetalPackaging Giants: Strategic Divergence & Financial Resilience

Strategic Divergence in Asset AllocationWhile all three giants benefit from the "infinite recyclability" narrative of metal packaging, their 2025 asset structures highlight distinct strategic identities:

* Ball Corporation ( The Pure-Play Scale Operator): Following the divestment of its aerospace division, Ball has doubled down on becoming a pure-play aluminum powerhouse. With over 95% of its core business focused on beverage packaging, Ball is betting entirely on the displacement of PET plastic. However, this focus creates a high sensitivity to volume fluctuations within the beverage sector.

* Crown Holdings (The Efficiency Engine): Crown differentiates itself through asset velocity. With an industry-leading asset turnover ratio (0.87x), Crown leverages a unique mix of consumer beverage cans and industrial "Transit Packaging." This dual engine allows Crown to capture upside during industrial expansion cycles while maintaining a steady baseline in consumer goods.

* Silgan Holdings (The Defensive Compounder): Silgan remains the "Defensive King." By holding a dominant >50% market share in North American metal food cans, Silgan creates a recession-proof cash flow floor. Furthermore, its aggressive M&A strategy—highlighted by the acquisition of Weener Packaging—signals a shift toward high-margin dispensing systems, moving the company up the value chain into beauty and healthcare.

The Pass-Through Shield: Neutralizing Commodity Volatility

A critical analysis of 2025 financials shows that raw material volatility (Aluminum and Steel) is no longer a primary threat to profitability, but rather a liquidity management challenge.

All three entities have successfully institutionalized "Pass-through Mechanisms." Financial disclosures indicate that the surge in nominal revenue for Ball and Crown was largely driven by the mathematical pass-through of higher aluminum costs to customers like Coca-Cola and AB InBev. For institutional investors, the "So What" is clear: Input cost risk is effectively neutralized. The analytical focus must now shift to "Lag Management"—how efficiently these companies manage the 1-3 month delay between cost spikes and contract price adjustments, and the resulting impact on quarterly working capital requirements.

HDIN Research Viewpoint: The Hidden Risks in Balance Sheets

While the operational narratives are robust, HDIN Research advises a more critical examination of the underlying quality of earnings and balance sheet health.

1. The Supply Chain Finance (SCF) "Red Flag": Our analysis flags a growing reliance on SCF programs, particularly within Silgan’s structure (approx. $438M balance). While this optimizes working capital optics, it can mask the true Days Payable Outstanding (DPO) and presents a liquidity risk should credit markets tighten.

2. Concentration Risk vs. Moat Durability: Ball Corporation’s reliance on its top three customers for nearly 40% of revenue presents a significant counterparty risk. In contrast, Silgan’s "Strategic Moat" in the food can sector offers superior downside protection. The high switching costs and long-term contracts (some extending to 2032) in the food sector provide a buffer that the more commoditized beverage can market lacks.

3. The "Green Premium" Reality: Sustainability is no longer just a compliance cost; it is a revenue driver. Ball and Crown’s aggressive Science-Based Targets (SBTi) and "Twentyby30" initiatives are securing them preferred supplier status with global FMCG giants. Investors should view R&D spend on lightweighting and circularity not as expenses, but as defensive capex against future carbon taxation.

HDIN Research Conclusion: For 2025-2026, the investment logic varies by risk appetite. Crown Holdings offers the best balance of efficiency and industrial upside; Silgan Holdings provides the strongest defensive shield against recessionary pressures; and Ball Corporation remains the high-beta play on the global adoption of aluminum.

Presentation Download

For a comprehensive breakdown of the financial ratios, regional growth engines, and our proprietary "Resilience Scoring" of these three giants:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com