Redwire 2025 Financial Review: Strategic M&A Masks Operational Headwinds in Space Infrastructure

Date : 2026-03-09

Reading : 562

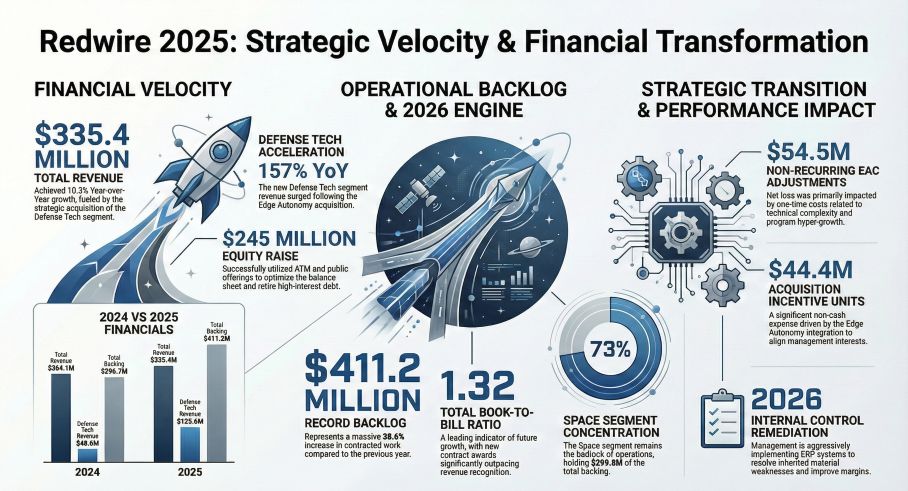

Redwire Corporation (RDW) closed Fiscal Year 2025 with a headline revenue increase of 10.3%, reaching $335.4 million. However, a deeper forensic analysis by HDIN Research reveals a bifurcated narrative: while the acquisition of Edge Autonomy successfully diversified the company into the high-velocity defense sector, the core space infrastructure business faced significant operational friction. The resulting gross margin compression—plummeting to 5.2%—underscores the volatility inherent in fixed-price government contracting during inflationary periods.

Figure Redwire 2025: Strategic Velocity & Financial Transformation

The "Profitless Prosperity" of Fixed-Price Contracts

The "Profitless Prosperity" of Fixed-Price Contracts

The most critical takeaway for investors is not the top-line growth, but the cost of achieving it. Redwire’s financial health was heavily impacted by a substantial $54.5 million negative Estimate at Completion (EAC) adjustment.

This metric serves as a barometer for operational efficiency. The adjustment indicates that the technical complexity of long-term space projects (such as solar arrays and docking mechanisms) led to cost overruns that the company could not pass on to customers due to rigid Fixed-Price (FFP) contract structures. Consequently, despite a revenue surge, the gross margin contracted by 9.4 percentage points year-over-year. For stakeholders, this highlights a structural risk: without improved pricing power or supply chain hedging, revenue expansion in the Space Segment may continue to yield diminishing returns on invested capital.

Strategic Pivot: The Defense Technology Hedge

Redwire’s restructuring into two distinct segments—Space and Defense Tech—marks a deliberate move to mitigate the risks of long-cycle R&D.

* Space Segment: Remains the heritage core, recognizing 97% of revenue "over-time." While organic revenue in this segment actually contracted, it retains a strong moat through "Flight Heritage" assets like the iROSA solar arrays and PIL-BOX pharmaceutical labs.

* Defense Tech Segment: Driven by the Edge Autonomy acquisition, this segment contributed $107 million in revenue. Crucially, 85% of this revenue is recognized at a "point-in-time."

The Strategic Implication: HDIN Research identifies this as a shift toward productization. By selling standardized Stalker and Penguin Unmanned Aerial Systems (UAS), Redwire is attempting to balance the lumpy, unpredictable cash flows of space exploration with the faster inventory turnover of defense hardware.

Forward Indicators: Book-to-Bill and Backlog

Despite profitability challenges, the demand signal remains robust. Redwire reported a total Book-to-Bill ratio of 1.32, with a record backlog of $411 million.

* Space Segment Book-to-Bill: 1.13

* Defense Tech Book-to-Bill: 1.62

These metrics suggest that Redwire’s technology—particularly its proprietary iROSA and new docking systems for commercial space stations—retains high market desirability. The challenge for 2026 will not be winning contracts, but executing them within budget.

HDIN Viewpoint: The Liquidity & Governance Tightrope

At HDIN Research, we advise clients to look beyond the backlog and focus on capital structure sustainability. Redwire’s 2025 operations resulted in a free cash flow deficit exceeding $200 million, driven by operating losses and M&A costs.

While the company successfully utilized At-The-Market (ATM) equity offerings to retire high-interest debt (including the Adams Street facility), this "funding operations via dilution" strategy is highly sensitive to market sentiment. Furthermore, the disclosed material weaknesses in internal controls—specifically regarding the integration of European and Defense units—pose a governance risk that could complicate future financial reporting.

The Verdict: Redwire has successfully built a defensive moat through Flight Heritage and diversified into drone autonomy. However, until the company stabilizes its EAC adjustments and repairs its internal controls, it remains an execution-heavy turnaround play rather than a stable compounding asset.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Video Analysis

Click this link to watch the YouTube video for a visual breakdown of Redwire’s 2025 financial performance.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Redwire 2025: Strategic Velocity & Financial Transformation

The "Profitless Prosperity" of Fixed-Price ContractsThe most critical takeaway for investors is not the top-line growth, but the cost of achieving it. Redwire’s financial health was heavily impacted by a substantial $54.5 million negative Estimate at Completion (EAC) adjustment.

This metric serves as a barometer for operational efficiency. The adjustment indicates that the technical complexity of long-term space projects (such as solar arrays and docking mechanisms) led to cost overruns that the company could not pass on to customers due to rigid Fixed-Price (FFP) contract structures. Consequently, despite a revenue surge, the gross margin contracted by 9.4 percentage points year-over-year. For stakeholders, this highlights a structural risk: without improved pricing power or supply chain hedging, revenue expansion in the Space Segment may continue to yield diminishing returns on invested capital.

Strategic Pivot: The Defense Technology Hedge

Redwire’s restructuring into two distinct segments—Space and Defense Tech—marks a deliberate move to mitigate the risks of long-cycle R&D.

* Space Segment: Remains the heritage core, recognizing 97% of revenue "over-time." While organic revenue in this segment actually contracted, it retains a strong moat through "Flight Heritage" assets like the iROSA solar arrays and PIL-BOX pharmaceutical labs.

* Defense Tech Segment: Driven by the Edge Autonomy acquisition, this segment contributed $107 million in revenue. Crucially, 85% of this revenue is recognized at a "point-in-time."

The Strategic Implication: HDIN Research identifies this as a shift toward productization. By selling standardized Stalker and Penguin Unmanned Aerial Systems (UAS), Redwire is attempting to balance the lumpy, unpredictable cash flows of space exploration with the faster inventory turnover of defense hardware.

Forward Indicators: Book-to-Bill and Backlog

Despite profitability challenges, the demand signal remains robust. Redwire reported a total Book-to-Bill ratio of 1.32, with a record backlog of $411 million.

* Space Segment Book-to-Bill: 1.13

* Defense Tech Book-to-Bill: 1.62

These metrics suggest that Redwire’s technology—particularly its proprietary iROSA and new docking systems for commercial space stations—retains high market desirability. The challenge for 2026 will not be winning contracts, but executing them within budget.

HDIN Viewpoint: The Liquidity & Governance Tightrope

At HDIN Research, we advise clients to look beyond the backlog and focus on capital structure sustainability. Redwire’s 2025 operations resulted in a free cash flow deficit exceeding $200 million, driven by operating losses and M&A costs.

While the company successfully utilized At-The-Market (ATM) equity offerings to retire high-interest debt (including the Adams Street facility), this "funding operations via dilution" strategy is highly sensitive to market sentiment. Furthermore, the disclosed material weaknesses in internal controls—specifically regarding the integration of European and Defense units—pose a governance risk that could complicate future financial reporting.

The Verdict: Redwire has successfully built a defensive moat through Flight Heritage and diversified into drone autonomy. However, until the company stabilizes its EAC adjustments and repairs its internal controls, it remains an execution-heavy turnaround play rather than a stable compounding asset.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Video Analysis

Click this link to watch the YouTube video for a visual breakdown of Redwire’s 2025 financial performance.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com