Lucid 2025 Financial Analysis: Strategic Moats and Capital Allocation Challenges

Date : 2026-03-09

Reading : 432

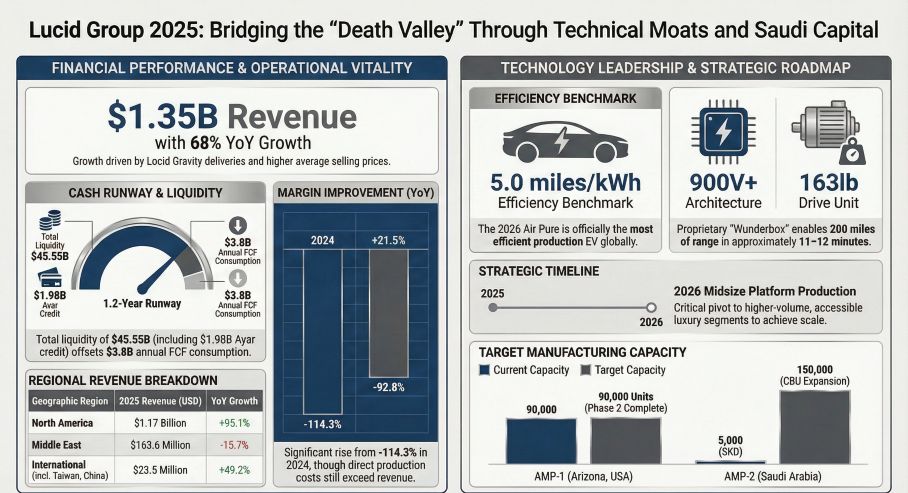

In fiscal year 2025, Lucid Group demonstrated a dual narrative of aggressive top-line expansion and profound capital dependency. While operational efficiency and the highly anticipated launch of the Lucid Gravity SUV drove a 68% revenue surge to $1.35 billion, the company's financial fundamentals remain heavily anchored by severe cash burn and structural manufacturing costs. HDIN Research’s deep-dive analysis of Lucid’s 2025 annual report reveals an enterprise at a critical inflection point, actively pivoting from a niche luxury automaker to a high-volume technology provider, all while navigating intense cyclical headwinds.

Figure Lucid Group 2025: Bridging the Death Valley Through Technical Moats and Saudi Capital

Financial Health: Scale Expansion Met with Structural Friction

Financial Health: Scale Expansion Met with Structural Friction

Lucid’s 2025 financial performance highlights the friction between market expansion and manufacturing realities. Gross margins witnessed a notable marginal improvement—climbing 21.5 percentage points from -114.3% in 2024 to -92.8% in 2025. This was primarily fueled by economies of scale from increased delivery volumes and regulatory credit sales. Furthermore, capital allocation efficiency in research and development improved significantly; R&D intensity dropped from 145.6% of revenue in 2024 to 89.5% in 2025 as the growing revenue base began to dilute fixed innovation costs.

However, the "So What" factor lies beneath the top-line growth. The company reported a net loss of $2.69 billion, nearly flat year-over-year. More alarmingly, Lucid recorded $816 million in inventory and firm purchase commitment write-downs (LCNRV)—representing over 60% of total revenue. This exceptionally high impairment underscores acute capacity underutilization at its AMP-1 facility (which boasts a 90,000-vehicle capacity) and severe supply chain cost pressures, proving that actual manufacturing output remains far below the critical breakeven threshold.

Strategic Pivots: From Luxury OEM to Technology Provider

To counter the demand bottleneck in the ultra-luxury sedan segment, Lucid is engineering a strategic paradigm shift. The company's core competitive advantage—its Strategic Moat—lies in its unmatched powertrain efficiency and miniaturization. Achieving an industry-leading 5.0 miles/kWh and a drive unit power density of 9.0 hp/kg, Lucid is leveraging its 900V+ electrical architecture to diversify its monetization channels.

This transition from a traditional OEM to a tier-one technology licensor is already materializing. The ongoing technology integration partnership with Aston Martin—yielding over $115 million in deferred revenue—and the strategic pact with Uber and Nuro to deploy 20,000 Level-4 Robotaxis over the next six years, serve as powerful validations of Lucid’s intellectual property. Furthermore, the company's sector positioning will undergo a massive shift in late 2026 with the introduction of its Midsize Platform, designed to penetrate the higher-volume, mass-market EV segment and achieve critical economies of scale.

Capital Allocation Efficiency and Geopolitical Headwinds

Operating an asset-heavy, vertically integrated model requires immense liquidity. Lucid's 2025 free cash flow (FCF) burn rate accelerated to approximately $3.8 billion, driven by Gravity production ramp-ups and broader capital expenditures. Consequently, Lucid’s survival is inextricably linked to its controlling shareholder, Saudi Arabia’s Public Investment Fund (PIF).

Through its affiliate Ayar, PIF provided a critical financial lifeline in 2025, including a $1.98 billion Delayed Draw Term Loan (DDTL) and continuous prepaid forward stock purchases. While Lucid maintains a total liquidity buffer of $4.55 billion—equating to a financial runway of roughly 1.2 years—this capital structure heavily dilutes minority shareholder equity.

Simultaneously, Lucid faces mounting cyclical and geopolitical headwinds. The implementation of the OBBBA act effectively eliminated the $7,500 U.S. federal EV tax credit, directly suppressing North American consumer demand. Additionally, shifting trade policies resulted in a $120 million new tariff impact in 2025, exposing Lucid’s supply chain vulnerabilities concerning critical minerals and regional export controls.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Lucid currently less as a self-sustaining commercial entity and more as a sovereign-backed, asset-heavy R&D project. The company has successfully established an impenetrable technical moat in EV efficiency, but its capital allocation model remains fragile.

Lucid is navigating a perilous "Valley of Death." The ultimate catalyst for a financial turnaround is not immediate margin parity, but the flawless execution of its 2026 Midsize Platform and the successful scaling of its AMP-2 facility in Saudi Arabia (targeting 150,000 CBU capacity). Investors must look beyond vehicle delivery metrics and focus on Lucid's technology licensing revenue growth and CapEx milestone achievements to gauge its long-term viability.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Lucid Group 2025: Bridging the Death Valley Through Technical Moats and Saudi Capital

Financial Health: Scale Expansion Met with Structural FrictionLucid’s 2025 financial performance highlights the friction between market expansion and manufacturing realities. Gross margins witnessed a notable marginal improvement—climbing 21.5 percentage points from -114.3% in 2024 to -92.8% in 2025. This was primarily fueled by economies of scale from increased delivery volumes and regulatory credit sales. Furthermore, capital allocation efficiency in research and development improved significantly; R&D intensity dropped from 145.6% of revenue in 2024 to 89.5% in 2025 as the growing revenue base began to dilute fixed innovation costs.

However, the "So What" factor lies beneath the top-line growth. The company reported a net loss of $2.69 billion, nearly flat year-over-year. More alarmingly, Lucid recorded $816 million in inventory and firm purchase commitment write-downs (LCNRV)—representing over 60% of total revenue. This exceptionally high impairment underscores acute capacity underutilization at its AMP-1 facility (which boasts a 90,000-vehicle capacity) and severe supply chain cost pressures, proving that actual manufacturing output remains far below the critical breakeven threshold.

Strategic Pivots: From Luxury OEM to Technology Provider

To counter the demand bottleneck in the ultra-luxury sedan segment, Lucid is engineering a strategic paradigm shift. The company's core competitive advantage—its Strategic Moat—lies in its unmatched powertrain efficiency and miniaturization. Achieving an industry-leading 5.0 miles/kWh and a drive unit power density of 9.0 hp/kg, Lucid is leveraging its 900V+ electrical architecture to diversify its monetization channels.

This transition from a traditional OEM to a tier-one technology licensor is already materializing. The ongoing technology integration partnership with Aston Martin—yielding over $115 million in deferred revenue—and the strategic pact with Uber and Nuro to deploy 20,000 Level-4 Robotaxis over the next six years, serve as powerful validations of Lucid’s intellectual property. Furthermore, the company's sector positioning will undergo a massive shift in late 2026 with the introduction of its Midsize Platform, designed to penetrate the higher-volume, mass-market EV segment and achieve critical economies of scale.

Capital Allocation Efficiency and Geopolitical Headwinds

Operating an asset-heavy, vertically integrated model requires immense liquidity. Lucid's 2025 free cash flow (FCF) burn rate accelerated to approximately $3.8 billion, driven by Gravity production ramp-ups and broader capital expenditures. Consequently, Lucid’s survival is inextricably linked to its controlling shareholder, Saudi Arabia’s Public Investment Fund (PIF).

Through its affiliate Ayar, PIF provided a critical financial lifeline in 2025, including a $1.98 billion Delayed Draw Term Loan (DDTL) and continuous prepaid forward stock purchases. While Lucid maintains a total liquidity buffer of $4.55 billion—equating to a financial runway of roughly 1.2 years—this capital structure heavily dilutes minority shareholder equity.

Simultaneously, Lucid faces mounting cyclical and geopolitical headwinds. The implementation of the OBBBA act effectively eliminated the $7,500 U.S. federal EV tax credit, directly suppressing North American consumer demand. Additionally, shifting trade policies resulted in a $120 million new tariff impact in 2025, exposing Lucid’s supply chain vulnerabilities concerning critical minerals and regional export controls.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Lucid currently less as a self-sustaining commercial entity and more as a sovereign-backed, asset-heavy R&D project. The company has successfully established an impenetrable technical moat in EV efficiency, but its capital allocation model remains fragile.

Lucid is navigating a perilous "Valley of Death." The ultimate catalyst for a financial turnaround is not immediate margin parity, but the flawless execution of its 2026 Midsize Platform and the successful scaling of its AMP-2 facility in Saudi Arabia (targeting 150,000 CBU capacity). Investors must look beyond vehicle delivery metrics and focus on Lucid's technology licensing revenue growth and CapEx milestone achievements to gauge its long-term viability.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com