Harley-Davidson 2025: Defensive Destocking, Financial Engineering, and the Pain of Structural Transition

Date : 2026-03-09

Reading : 557

Harley-Davidson’s (H-D) 2025 fiscal year represents a profound period of "defensive clearing" and structural reconstitution. While top-line metrics indicate a 13.8% contraction in total revenue to $4.47 billion, the underlying strategic narrative reveals a company deliberately sacrificing short-term manufacturing profitability to enforce channel health. However, beneath the surface of aggressive dealer inventory destocking lies a heavy reliance on financial engineering—specifically the divestiture of retail loan assets—to mask the severe margin compression within its core motorcycle operations.

Figure Harley-Davidson 2025 Performance: Financial Pivot & Strategic Shift

Financial Health: The Illusion of HDFS and Core Margin Contraction

Financial Health: The Illusion of HDFS and Core Margin Contraction

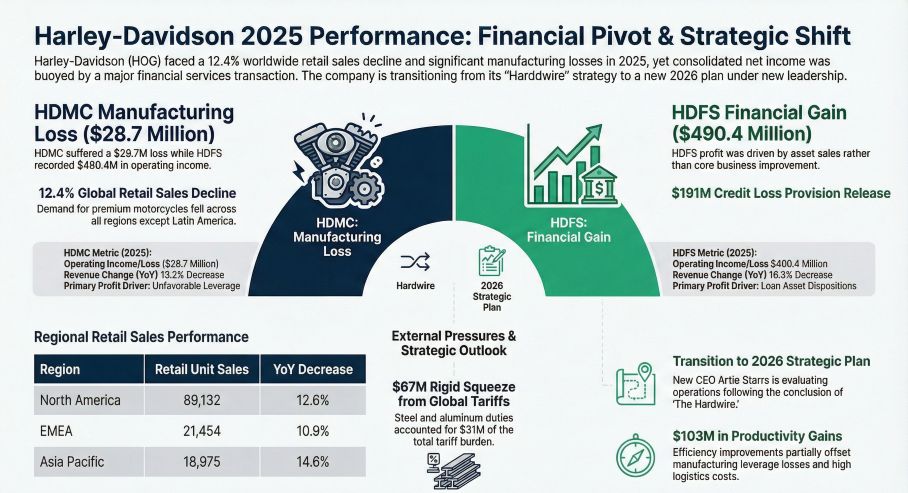

The most critical takeaway from Harley-Davidson’s 2025 financial performance is the stark divergence between its manufacturing and financial services divisions. The core Harley-Davidson Motor Company (HDMC) business swung from a $278 million operating profit in 2024 to a $28.7 million operating loss in 2025.

This deterioration was not merely a symptom of softening consumer demand, but rather the direct result of severe negative operating leverage. By strategically curtailing wholesale shipments by 16.4% (dropping to 124,477 units) in a high-fixed-cost manufacturing environment, the company triggered a spike in per-unit fixed costs, wiping out $189 million in gross profit. Compounding this operational squeeze were cyclical headwinds in the form of rigid supply chain costs and an estimated $67 million in new global tariffs (particularly steel and aluminum).

Conversely, the Harley-Davidson Financial Services (HDFS) segment reported a staggering 97.4% year-over-year increase in operating profit, reaching $490 million. However, HDIN Research notes this is largely an accounting illusion. The profit surge was driven by a strategic deleveraging transaction—selling $4.1 billion in retail loans to partners like KKR and PIMCO—which triggered a one-time release of $191 million in credit loss provisions. While this transition to an "asset-light" service operator provides immediate liquidity and mitigates macroeconomic high-interest-rate risks, it inherently compresses future interest income streams.

Strategic Pivots: Channel Destocking and Capital Allocation Efficiency

Management's core objective in 2025 was clear: absorb the balance sheet pain to repair the dealer network. By enforcing a "shipments trailing retail" strategy, the company successfully reduced global dealer new-bike inventory by 17%, bringing it down to approximately 40,000 units by year-end.

To achieve this, Harley-Davidson leaned heavily into selective promotional incentives, particularly on its high-margin Grand American Touring models. While this degraded the brand's traditional premium pricing power, it successfully corrected the inventory mismatch.

From a capital allocation perspective, the company returned approximately $433.9 million to shareholders via dividends and accelerated share repurchases (ASR). Yet, the "So What" behind this metric is cautionary: with 2025 operating cash flow nearly halving to $569 million, these shareholder returns were heavily subsidized by the $3.78 billion net cash inflow from the HDFS asset liquidation, rather than organic business growth. This raises questions regarding the long-term sustainability of current capital allocation efficiencies without a rebound in core manufacturing profitability.

Sector Positioning: Demographic Shifts and EV Regulatory Challenges

Looking beyond the balance sheet, Harley-Davidson faces entrenched structural hurdles. The aging demographic of its core rider base threatens long-term volume, prompting a necessary but capital-intensive pivot toward lighter, more urban-centric mobility solutions.

This shift is spearheaded by the LiveWire EV division, which, despite reducing its operating loss to $75 million, remains deeply in the red. LiveWire's strategic pivot toward "Concept Mini-motorcycles" aims to bridge the gap to younger consumers, but the division faces intense regulatory headwinds. Subsidy phase-outs, evolving EU battery compliance mandates, and shifting emissions standards create a highly volatile regulatory environment that threatens the commercial viability of EV expansion.

Furthermore, the brand's sector positioning is increasingly threatened by used motorcycle residuals. As the company pushes out technologically updated models, the influx of older models into the secondary market depresses residual values, effectively cannibalizing the MSRP acceptance for new models and trapping the brand in a cyclical zero-sum game.

HDIN Viewpoint

HDIN Research views Harley-Davidson’s 2026 outlook as a period of "structural bottoming out." Management’s exceptionally narrow 2026 HDMC operating margin guidance of -$40 million to +$10 million, paired with marginal shipment growth forecasts (130k-135k units), indicates that the operational headwinds of tariff normalizations and shifting demographics will persist.

While the 2025 inventory purge was a painful necessity that successfully cleansed the channel, the company cannot rely on asset divestitures to subsidize operations indefinitely. The strategic moats of the past are eroding. The true catalyst for long-term value creation now rests entirely on the impending strategic roadmap slated for Q2 2026 under the new CEO, Artie Starrs. Investors and industry stakeholders must closely monitor whether this upcoming strategy can pivot the company from defensive contraction back to organic market expansion.

Presentation Download & Media

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Harley-Davidson 2025 Performance: Financial Pivot & Strategic Shift

Financial Health: The Illusion of HDFS and Core Margin ContractionThe most critical takeaway from Harley-Davidson’s 2025 financial performance is the stark divergence between its manufacturing and financial services divisions. The core Harley-Davidson Motor Company (HDMC) business swung from a $278 million operating profit in 2024 to a $28.7 million operating loss in 2025.

This deterioration was not merely a symptom of softening consumer demand, but rather the direct result of severe negative operating leverage. By strategically curtailing wholesale shipments by 16.4% (dropping to 124,477 units) in a high-fixed-cost manufacturing environment, the company triggered a spike in per-unit fixed costs, wiping out $189 million in gross profit. Compounding this operational squeeze were cyclical headwinds in the form of rigid supply chain costs and an estimated $67 million in new global tariffs (particularly steel and aluminum).

Conversely, the Harley-Davidson Financial Services (HDFS) segment reported a staggering 97.4% year-over-year increase in operating profit, reaching $490 million. However, HDIN Research notes this is largely an accounting illusion. The profit surge was driven by a strategic deleveraging transaction—selling $4.1 billion in retail loans to partners like KKR and PIMCO—which triggered a one-time release of $191 million in credit loss provisions. While this transition to an "asset-light" service operator provides immediate liquidity and mitigates macroeconomic high-interest-rate risks, it inherently compresses future interest income streams.

Strategic Pivots: Channel Destocking and Capital Allocation Efficiency

Management's core objective in 2025 was clear: absorb the balance sheet pain to repair the dealer network. By enforcing a "shipments trailing retail" strategy, the company successfully reduced global dealer new-bike inventory by 17%, bringing it down to approximately 40,000 units by year-end.

To achieve this, Harley-Davidson leaned heavily into selective promotional incentives, particularly on its high-margin Grand American Touring models. While this degraded the brand's traditional premium pricing power, it successfully corrected the inventory mismatch.

From a capital allocation perspective, the company returned approximately $433.9 million to shareholders via dividends and accelerated share repurchases (ASR). Yet, the "So What" behind this metric is cautionary: with 2025 operating cash flow nearly halving to $569 million, these shareholder returns were heavily subsidized by the $3.78 billion net cash inflow from the HDFS asset liquidation, rather than organic business growth. This raises questions regarding the long-term sustainability of current capital allocation efficiencies without a rebound in core manufacturing profitability.

Sector Positioning: Demographic Shifts and EV Regulatory Challenges

Looking beyond the balance sheet, Harley-Davidson faces entrenched structural hurdles. The aging demographic of its core rider base threatens long-term volume, prompting a necessary but capital-intensive pivot toward lighter, more urban-centric mobility solutions.

This shift is spearheaded by the LiveWire EV division, which, despite reducing its operating loss to $75 million, remains deeply in the red. LiveWire's strategic pivot toward "Concept Mini-motorcycles" aims to bridge the gap to younger consumers, but the division faces intense regulatory headwinds. Subsidy phase-outs, evolving EU battery compliance mandates, and shifting emissions standards create a highly volatile regulatory environment that threatens the commercial viability of EV expansion.

Furthermore, the brand's sector positioning is increasingly threatened by used motorcycle residuals. As the company pushes out technologically updated models, the influx of older models into the secondary market depresses residual values, effectively cannibalizing the MSRP acceptance for new models and trapping the brand in a cyclical zero-sum game.

HDIN Viewpoint

HDIN Research views Harley-Davidson’s 2026 outlook as a period of "structural bottoming out." Management’s exceptionally narrow 2026 HDMC operating margin guidance of -$40 million to +$10 million, paired with marginal shipment growth forecasts (130k-135k units), indicates that the operational headwinds of tariff normalizations and shifting demographics will persist.

While the 2025 inventory purge was a painful necessity that successfully cleansed the channel, the company cannot rely on asset divestitures to subsidize operations indefinitely. The strategic moats of the past are eroding. The true catalyst for long-term value creation now rests entirely on the impending strategic roadmap slated for Q2 2026 under the new CEO, Artie Starrs. Investors and industry stakeholders must closely monitor whether this upcoming strategy can pivot the company from defensive contraction back to organic market expansion.

Presentation Download & Media

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com