Lindsay vs. Valmont FY2025: Sector Positioning, Capital Allocation, and Strategic Moats

Date : 2026-03-09

Reading : 127

In FY2025, the global mechanized irrigation and agricultural infrastructure sectors navigated a complex matrix of cyclical headwinds, characterized by fluctuating crop prices, high interest rates, and geopolitical supply chain shifts. Based on a comprehensive look-through analysis of the latest annual reports, HDIN Research reveals a stark divergence in the operational logic and strategic pivots of the industry’s two titans: Lindsay Corporation (NYSE: LNN) and Valmont Industries, Inc. (NYSE: VMI).

Rather than engaging in direct, symmetric competition, both companies have cultivated highly distinct strategic moats. Valmont is leveraging global grid electrification to offset agricultural cyclicality, while Lindsay is doubling down on international mega-projects and proprietary AgTech data ecosystems.

Figure 2025 Strategic Duel: Lindsay vs. Valmont Comparative Analysis

Sector Positioning and Structural Asymmetry

Sector Positioning and Structural Asymmetry

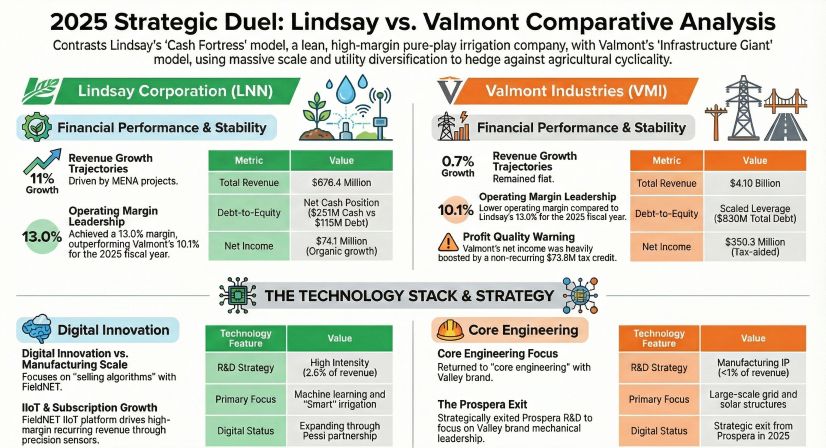

The fundamental difference between the two entities lies in their scale and revenue architecture. Valmont operates with an absolute scale advantage, generating $4.1 billion in FY2025 revenue—roughly six times that of Lindsay’s $676.4 million. However, their structural dependencies dictate entirely different risk profiles.

Valmont has successfully engineered a "dual-pillar" model, acting primarily as an infrastructure behemoth (75% of revenue) rather than a pure agricultural play. In FY2025, a 10.4% surge in its utility support structures effectively absorbed a 5.8% revenue contraction in its agricultural division. This infrastructure dominance provides a critical counter-cyclical hedge against volatile farm economics. Conversely, Lindsay remains a highly concentrated agricultural pure-play (84% irrigation revenue). While it lacks Valmont’s macroeconomic buffer, Lindsay's agility and aggressive international expansion—highlighted by a massive 39% growth in international irrigation driven by over $100 million in MENA (Middle East and North Africa) government food security projects—demonstrate its formidable ability to capture concentrated global demand.

Capital Allocation Efficiency and Financial Health

When analyzing the balance sheets, HDIN Research identifies a sharp contrast in capital allocation efficiency and earnings purity.

Lindsay operates as a quintessential "cash flow fortress." The company maintains a pristine net-cash position, holding $251 million in cash reserves against a mere $115 million in total debt. Its operating cash flow (OCF) covers net income by an impressive 1.79x, underscoring exceptional earnings quality. Lindsay’s capital allocation is decidedly conservative and organic, prioritizing modernization CapEx ($42.5 million) over massive shareholder payouts to secure future manufacturing productivity.

Valmont, contrastingly, utilizes leveraged operations ($830 million in debt) to optimize shareholder returns, deploying an aggressive $198.1 million in stock buybacks. While Valmont boasts superior supply chain efficiency—evidenced by an inventory turnover rate of 4.95x compared to Lindsay’s 3.20x—its FY2025 profitability requires stringent scrutiny. Valmont’s reported net income was heavily distorted by non-recurring financial maneuvers, notably a $73.8 million tax deduction stemming from the exit of its Prospera business, which artificially plummeted its effective tax rate to 6.3%. Stripping away these paper benefits and accounting for a steep $91.3 million asset impairment in its infrastructure division, Valmont's organic profitability faced tangible pressure in a high-rate environment.

Strategic Pivots: AgTech Algorithms vs. Heavy Engineering

A defining divergence in FY2025 is how both companies approach technological research and development.

Lindsay is aggressively transitioning from a hardware manufacturer to an AgTech data provider. Maintaining a high R&D intensity (2.6% of revenue), Lindsay’s growth engine is powered by "Smart Agriculture" tech spillovers, leveraging its FieldNET® IIoT platform and strategic investments in Pessl Instruments to lock in recurring subscription revenue.

In a stark strategic reversal, Valmont has signaled a retreat from digital agriculture. Following its exit from the Prospera digital venture, Valmont slashed its R&D expenditure from $59 million down to $33 million (less than 1% of revenue). Instead of algorithms, Valmont is reinforcing its heavy manufacturing IP, focusing on the "Electrification Revolution." Its strategic moat now firmly rests on scaling single-axis solar trackers, telecom structures, and utility poles to feed the voracious energy demands of AI data centers and renewable grid integrations.

Cyclical Headwinds and Macro Defensibility

Both companies are navigating an agricultural "false boom." While the USDA projected a 41% increase in 2025 net farm income, this is heavily skewed by government disaster relief rather than organic crop cash receipts. Consequently, North American farmers remain hesitant to commit to large-scale capital expenditures.

Furthermore, global supply chain resilience remains a critical test. Both Lindsay and Valmont rely on highly distributed manufacturing footprints—spanning the United States, Brazil, and regions across Greater China (including operations in Taiwan, Province of China)—to mitigate tariff risks and raw material cost inflation. Lindsay has demonstrated superior pricing power, successfully passing tariff-induced supply chain premiums onto the end market and maintaining a robust 13.0% operating margin, outperforming Valmont’s 10.1%.

HDIN Viewpoint

From an institutional investment perspective, Lindsay’s valuation premium is structurally justified. Its balance sheet is entirely insulated from goodwill impairment risks, its earnings growth is driven by transparent margin expansion, and its ability to secure national-level MENA food security projects highlights robust international market penetration.

Valmont, while offering an unmatched proxy for global grid resilience and electrification, carries a valuation discount risk in the near term. Investors must look past the headline EPS to account for the $91.3 million in restructuring impairments and the artificial boost from tax write-offs. Ultimately, the mechanization of agriculture is bifurcating: Lindsay is winning the battle for the "smart farm," while Valmont has successfully pivoted to become a dominant force in the global energy transition.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Rather than engaging in direct, symmetric competition, both companies have cultivated highly distinct strategic moats. Valmont is leveraging global grid electrification to offset agricultural cyclicality, while Lindsay is doubling down on international mega-projects and proprietary AgTech data ecosystems.

Figure 2025 Strategic Duel: Lindsay vs. Valmont Comparative Analysis

Sector Positioning and Structural AsymmetryThe fundamental difference between the two entities lies in their scale and revenue architecture. Valmont operates with an absolute scale advantage, generating $4.1 billion in FY2025 revenue—roughly six times that of Lindsay’s $676.4 million. However, their structural dependencies dictate entirely different risk profiles.

Valmont has successfully engineered a "dual-pillar" model, acting primarily as an infrastructure behemoth (75% of revenue) rather than a pure agricultural play. In FY2025, a 10.4% surge in its utility support structures effectively absorbed a 5.8% revenue contraction in its agricultural division. This infrastructure dominance provides a critical counter-cyclical hedge against volatile farm economics. Conversely, Lindsay remains a highly concentrated agricultural pure-play (84% irrigation revenue). While it lacks Valmont’s macroeconomic buffer, Lindsay's agility and aggressive international expansion—highlighted by a massive 39% growth in international irrigation driven by over $100 million in MENA (Middle East and North Africa) government food security projects—demonstrate its formidable ability to capture concentrated global demand.

Capital Allocation Efficiency and Financial Health

When analyzing the balance sheets, HDIN Research identifies a sharp contrast in capital allocation efficiency and earnings purity.

Lindsay operates as a quintessential "cash flow fortress." The company maintains a pristine net-cash position, holding $251 million in cash reserves against a mere $115 million in total debt. Its operating cash flow (OCF) covers net income by an impressive 1.79x, underscoring exceptional earnings quality. Lindsay’s capital allocation is decidedly conservative and organic, prioritizing modernization CapEx ($42.5 million) over massive shareholder payouts to secure future manufacturing productivity.

Valmont, contrastingly, utilizes leveraged operations ($830 million in debt) to optimize shareholder returns, deploying an aggressive $198.1 million in stock buybacks. While Valmont boasts superior supply chain efficiency—evidenced by an inventory turnover rate of 4.95x compared to Lindsay’s 3.20x—its FY2025 profitability requires stringent scrutiny. Valmont’s reported net income was heavily distorted by non-recurring financial maneuvers, notably a $73.8 million tax deduction stemming from the exit of its Prospera business, which artificially plummeted its effective tax rate to 6.3%. Stripping away these paper benefits and accounting for a steep $91.3 million asset impairment in its infrastructure division, Valmont's organic profitability faced tangible pressure in a high-rate environment.

Strategic Pivots: AgTech Algorithms vs. Heavy Engineering

A defining divergence in FY2025 is how both companies approach technological research and development.

Lindsay is aggressively transitioning from a hardware manufacturer to an AgTech data provider. Maintaining a high R&D intensity (2.6% of revenue), Lindsay’s growth engine is powered by "Smart Agriculture" tech spillovers, leveraging its FieldNET® IIoT platform and strategic investments in Pessl Instruments to lock in recurring subscription revenue.

In a stark strategic reversal, Valmont has signaled a retreat from digital agriculture. Following its exit from the Prospera digital venture, Valmont slashed its R&D expenditure from $59 million down to $33 million (less than 1% of revenue). Instead of algorithms, Valmont is reinforcing its heavy manufacturing IP, focusing on the "Electrification Revolution." Its strategic moat now firmly rests on scaling single-axis solar trackers, telecom structures, and utility poles to feed the voracious energy demands of AI data centers and renewable grid integrations.

Cyclical Headwinds and Macro Defensibility

Both companies are navigating an agricultural "false boom." While the USDA projected a 41% increase in 2025 net farm income, this is heavily skewed by government disaster relief rather than organic crop cash receipts. Consequently, North American farmers remain hesitant to commit to large-scale capital expenditures.

Furthermore, global supply chain resilience remains a critical test. Both Lindsay and Valmont rely on highly distributed manufacturing footprints—spanning the United States, Brazil, and regions across Greater China (including operations in Taiwan, Province of China)—to mitigate tariff risks and raw material cost inflation. Lindsay has demonstrated superior pricing power, successfully passing tariff-induced supply chain premiums onto the end market and maintaining a robust 13.0% operating margin, outperforming Valmont’s 10.1%.

HDIN Viewpoint

From an institutional investment perspective, Lindsay’s valuation premium is structurally justified. Its balance sheet is entirely insulated from goodwill impairment risks, its earnings growth is driven by transparent margin expansion, and its ability to secure national-level MENA food security projects highlights robust international market penetration.

Valmont, while offering an unmatched proxy for global grid resilience and electrification, carries a valuation discount risk in the near term. Investors must look past the headline EPS to account for the $91.3 million in restructuring impairments and the artificial boost from tax write-offs. Ultimately, the mechanization of agriculture is bifurcating: Lindsay is winning the battle for the "smart farm," while Valmont has successfully pivoted to become a dominant force in the global energy transition.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com