2025 Semiconductor Sector: Strategic Moats, Cyclical Shifts, and Capital Allocation

Date : 2026-03-08

Reading : 401

The 2025 semiconductor landscape is defined by extreme bifurcation and structural resets. While top-tier players leveraging manufacturing cost advantages and non-overlapping business segments have successfully navigated cyclical headwinds, others overly reliant on singular end-markets are enduring painful financial restructuring. Based on a deep-dive analysis of 2025 annual reports, HDIN Research dissects the financial health, strategic pivots, and capital allocation efficiency of eight global power and analog semiconductor leaders, revealing the underlying logic of sector positioning in the post-shortage era.

Figure 2025 Power Semiconductor Performance: The Great Bifurcation

Strategic Moats: The Integration of Analog and Power

Strategic Moats: The Integration of Analog and Power

In 2025, competitive moats have shifted from mere technological capability to structural cost leadership and ecosystem integration. A clear "Analog + Power" cross-selling strategy is driving profound market stickiness for legacy giants.

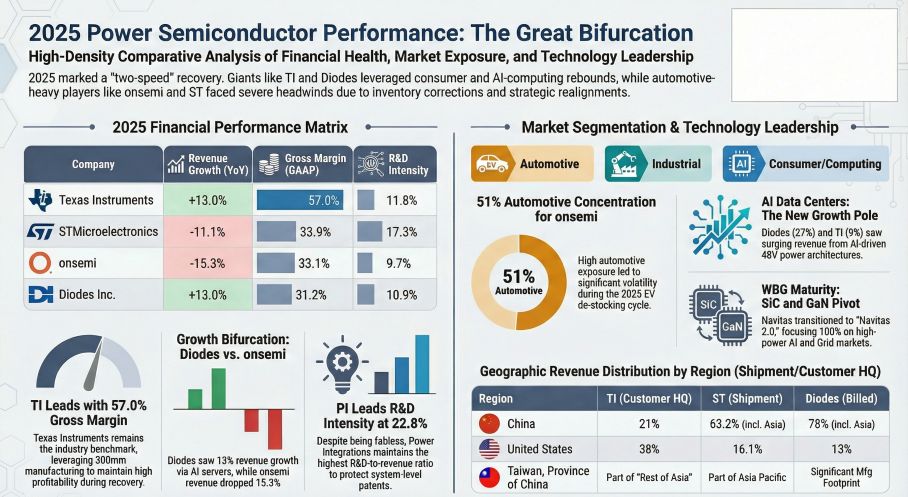

Texas Instruments (TI) remains the absolute benchmark for operational efficiency. By reaching the climax of its six-year CapEx cycle for 300mm wafer fabrication, TI has engineered a structural cost advantage—reducing unpackaged chip costs by approximately 40% compared to 200mm peers. This enables a staggering 57% gross margin despite broader market softness. Similarly, Power Integrations (PI) demonstrates formidable "soft IDM" moats; its system-level integration of PowiGaN technology yields extreme Free Cash Flow (FCF) conversion rates exceeding 300%, insulating it from consumer electronics volatility.

Conversely, a pronounced competitive mismatch has emerged between pure-play innovators and broad-portfolio veterans. Navitas operates as a "cutting-edge island," aggressively pivoting away from low-end consumer electronics to exclusively target 800V AI data centers and grid infrastructure. In stark contrast, Vishay and Diodes function as "full-solution archipelagos." Vishay utilizes its massive passive component portfolio as a high-barrier wedge, effectively capturing long-tail industrial demand that pure-play semiconductor innovators cannot easily address.

Cyclical Headwinds and Terminal Market Pivots

The "Automotive Dependency" trap severely disrupted the financial health of several industry heavyweights in 2025. As the electric vehicle (EV) supply chain entered a brutal destocking cycle, onsemi and STMicroelectronics (ST) experienced acute operational pressure. The automotive slowdown resulted in drastic top-line contractions and prompted "Big Bath" accounting measures, with onsemi recording $496 million in non-cash asset impairments to artificially lower future depreciation burdens and recalibrate its manufacturing footprint.

To hedge against these cyclical headwinds, resilient firms relied on non-overlapping, long-cycle segments. Vishay leveraged the steady demand for its resistors and capacitors in defense and grid infrastructure as a ballast against MOSFET margin compression. Meanwhile, AI server power architectures (48V to 12V/5V transition) emerged as the industry's ultimate growth engine. Diodes successfully offset industrial deceleration through a surge in its computing division, which now accounts for 27% of its revenue, highlighting the crucial role of end-market diversification.

Capital Allocation Efficiency: Expansion vs. Restructuring

Capital allocation in 2025 illustrates a sharp divergence between counter-cyclical expansion and strategic contraction.

* The Cash Cow Paradigm: TI demonstrated unparalleled capital return capabilities, distributing $6.48 billion to shareholders via dividends and buybacks. Its ability to generate robust FCF while sustaining aggressive R&D firmly establishes its long-term compounding model.

* Aggressive Expansion: ST and Vishay are aggressively deploying heavy capital to secure future capacity. ST's joint venture in Chongqing for a 200mm SiC facility exemplifies a preemptive "China-for-China" defensive strategy, embedding itself deeply within the local EV supply chain to mitigate geopolitical friction. Vishay is leveraging its balance sheet to expand its 12-inch and Newport fabs, a high-stakes gamble dependent on a robust 2026 market recovery.

* Supply Chain & Transparency Risks: Navitas faces acute supply chain redesign risks. Following TSMC's announced 2027 exit from GaN production, Navitas must rapidly migrate its foundries, risking temporary market share erosion and inflated R&D costs. Meanwhile, Prisemi boasts exceptional operating margins (29.1%) driven by aggressive cost controls, but its reliance on "commercial secret" exemptions regarding top supplier disclosures raises red flags concerning supply chain transparency and corporate governance.

HDIN Viewpoint

From the perspective of HDIN Research, 2025 is a definitive "shakeout" year that rewards structural resilience over cyclical beta. The true determiners of 2026-2027 market leadership are not merely top-line revenue growth, but rather the fortification of 300mm cost structures, the closure of Silicon Carbide (SiC) supply chains, and the agility to pivot into AI data center infrastructure without destroying free cash flow margins. For strategic planners and institutional investors, the mandate is clear: prioritize capital allocation efficiency and scrutinize the hidden risks within aggressively restructured asset bases.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Power Semiconductor Performance: The Great Bifurcation

Strategic Moats: The Integration of Analog and PowerIn 2025, competitive moats have shifted from mere technological capability to structural cost leadership and ecosystem integration. A clear "Analog + Power" cross-selling strategy is driving profound market stickiness for legacy giants.

Texas Instruments (TI) remains the absolute benchmark for operational efficiency. By reaching the climax of its six-year CapEx cycle for 300mm wafer fabrication, TI has engineered a structural cost advantage—reducing unpackaged chip costs by approximately 40% compared to 200mm peers. This enables a staggering 57% gross margin despite broader market softness. Similarly, Power Integrations (PI) demonstrates formidable "soft IDM" moats; its system-level integration of PowiGaN technology yields extreme Free Cash Flow (FCF) conversion rates exceeding 300%, insulating it from consumer electronics volatility.

Conversely, a pronounced competitive mismatch has emerged between pure-play innovators and broad-portfolio veterans. Navitas operates as a "cutting-edge island," aggressively pivoting away from low-end consumer electronics to exclusively target 800V AI data centers and grid infrastructure. In stark contrast, Vishay and Diodes function as "full-solution archipelagos." Vishay utilizes its massive passive component portfolio as a high-barrier wedge, effectively capturing long-tail industrial demand that pure-play semiconductor innovators cannot easily address.

Cyclical Headwinds and Terminal Market Pivots

The "Automotive Dependency" trap severely disrupted the financial health of several industry heavyweights in 2025. As the electric vehicle (EV) supply chain entered a brutal destocking cycle, onsemi and STMicroelectronics (ST) experienced acute operational pressure. The automotive slowdown resulted in drastic top-line contractions and prompted "Big Bath" accounting measures, with onsemi recording $496 million in non-cash asset impairments to artificially lower future depreciation burdens and recalibrate its manufacturing footprint.

To hedge against these cyclical headwinds, resilient firms relied on non-overlapping, long-cycle segments. Vishay leveraged the steady demand for its resistors and capacitors in defense and grid infrastructure as a ballast against MOSFET margin compression. Meanwhile, AI server power architectures (48V to 12V/5V transition) emerged as the industry's ultimate growth engine. Diodes successfully offset industrial deceleration through a surge in its computing division, which now accounts for 27% of its revenue, highlighting the crucial role of end-market diversification.

Capital Allocation Efficiency: Expansion vs. Restructuring

Capital allocation in 2025 illustrates a sharp divergence between counter-cyclical expansion and strategic contraction.

* The Cash Cow Paradigm: TI demonstrated unparalleled capital return capabilities, distributing $6.48 billion to shareholders via dividends and buybacks. Its ability to generate robust FCF while sustaining aggressive R&D firmly establishes its long-term compounding model.

* Aggressive Expansion: ST and Vishay are aggressively deploying heavy capital to secure future capacity. ST's joint venture in Chongqing for a 200mm SiC facility exemplifies a preemptive "China-for-China" defensive strategy, embedding itself deeply within the local EV supply chain to mitigate geopolitical friction. Vishay is leveraging its balance sheet to expand its 12-inch and Newport fabs, a high-stakes gamble dependent on a robust 2026 market recovery.

* Supply Chain & Transparency Risks: Navitas faces acute supply chain redesign risks. Following TSMC's announced 2027 exit from GaN production, Navitas must rapidly migrate its foundries, risking temporary market share erosion and inflated R&D costs. Meanwhile, Prisemi boasts exceptional operating margins (29.1%) driven by aggressive cost controls, but its reliance on "commercial secret" exemptions regarding top supplier disclosures raises red flags concerning supply chain transparency and corporate governance.

HDIN Viewpoint

From the perspective of HDIN Research, 2025 is a definitive "shakeout" year that rewards structural resilience over cyclical beta. The true determiners of 2026-2027 market leadership are not merely top-line revenue growth, but rather the fortification of 300mm cost structures, the closure of Silicon Carbide (SiC) supply chains, and the agility to pivot into AI data center infrastructure without destroying free cash flow margins. For strategic planners and institutional investors, the mandate is clear: prioritize capital allocation efficiency and scrutinize the hidden risks within aggressively restructured asset bases.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com