ARYZTA vs. Flowers Foods: 2025 Strategic Audit

Date : 2026-03-07

Reading : 129

In 2025, the global bakery industry is experiencing a profound structural divergence. Based on an in-depth financial and strategic audit conducted by HDIN Research, ARYZTA AG and Flowers Foods represent two diametrically opposed corporate trajectories. ARYZTA has successfully transitioned into a resilient, "post-restructuring" phase, utilizing organic innovation and aggressive deleveraging to fortify its margins. In stark contrast, Flowers Foods is navigating a painful transformation phase, relying heavily on debt-funded M&A to offset structural declines in its core traditional retail markets. For institutional investors and corporate strategists, understanding the "so what" behind these divergent capital allocation strategies is critical to navigating the sector's macroeconomic headwinds.

Figure 2025 Bakery Giants Face-Off: ARYZTA vs. Flowers Foods

Growth Engines: Organic Resilience vs. Structural M&A Expansion

Growth Engines: Organic Resilience vs. Structural M&A Expansion

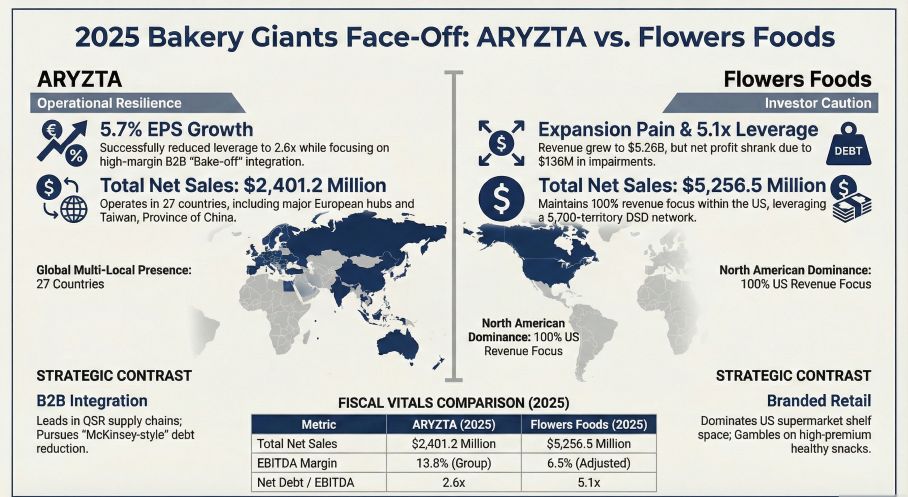

A penetration analysis of both companies' revenue streams reveals a stark contrast in growth quality. ARYZTA’s growth logic is fundamentally rooted in an "innovation premium." By deploying advanced lamination production lines across Europe and focusing on its high-margin "Bake-off" B2B solutions, ARYZTA generated 19% of its annual revenue from innovative new products. This strategy allows its downstream Quick Service Restaurant (QSR) clients to drastically reduce labor costs, thereby granting ARYZTA pricing power and robust organic growth despite inflationary pressures.

Conversely, Flowers Foods' nominal 3.0% revenue growth is largely an accounting illusion. When adjusting for the $214 million revenue contribution from its premium Simple Mills acquisition and the favorable accounting timing of a 53rd week, the company's underlying organic growth is negative, plagued by a 2.0% volume contraction. Traditional packaged bread is losing shelf dominance, forcing Flowers Foods into a high-premium M&A strategy to buy its way into the "Better-for-you" healthy snack corridor. Ultimately, ARYZTA’s endogenous growth model demonstrates superior immunity to macroeconomic volatility compared to Flowers Foods' reliance on inorganic expansion.

Strategic Moats and Cyclical Headwinds

The defensive capabilities of these two baking giants stem from fundamentally different strategic moats, exposing them to unique systemic risks.

ARYZTA has constructed a formidable B2B moat through deep supply chain integration. With 52% of its revenue derived from food service and QSRs, its production facilities are deeply embedded into the operational frameworks of global chains. This creates extraordinarily high switching costs for clients. Furthermore, ARYZTA benefits from geographic hedging. While facing margin pressures in Europe due to labor inflation, its "Rest of World" (ROW) segment—covering regions like Asia-Pacific—acts as a cash cow, boasting a stellar 20.9% EBITDA margin.

Flowers Foods, while commanding unparalleled brand penetration and a dominant Direct Store Delivery (DSD) network in the US, suffers from 100% single-market exposure. This geographical concentration amplifies its vulnerability to domestic cyclical headwinds. The company is actively battling a consumer downgrade shift toward lower-margin private labels. More structurally, Flowers Foods faces an unprecedented threat from the rise of GLP-1 appetite-suppressing medications, which poses a long-term risk of suppressing baseline carbohydrate consumption.

Capital Allocation Efficiency and Financial Health

The most glaring divergence between the two industry leaders lies in their capital allocation efficiency and balance sheet management.

ARYZTA is executing a disciplined, McKinsey-style financial restructuring. By directing its free cash flow toward hybrid bond buybacks, it has successfully driven its net debt-to-EBITDA leverage down to a healthy 2.6x, with a clear trajectory toward 1.5x-2.0x. This asset-light optimization ensures high returns on invested capital (ROIC) and robust interest coverage.

Flowers Foods, however, is executing a high-stakes financial gamble. To fund its Simple Mills acquisition, the company has heavily leveraged its balance sheet, causing its leverage ratio to spike to a precarious 5.1x and its interest expenses to surge by 202%. Despite a 66% drop in net income, management maintained aggressive shareholder dividend payouts ($209 million) and initiated a massive $325 million ERP IT system upgrade. HDIN Research warns of significant impairment landmines: Flowers Foods has already recognized $136 million in regional brand impairments, and its $368 million goodwill from Simple Mills sits at a razor-thin 7.9% fair value premium above book value. Any minor downward revision in earnings could trigger a massive goodwill write-off.

HDIN Viewpoint: Navigating the Industry's Growth Ceiling

From the perspective of HDIN Research, the bakery sector's competition has evolved from mere capacity expansion to a dual battle for "supply chain depth" and "digital/ESG compliance." Both companies are forced to pivot their CapEx toward automation and green infrastructure to combat structural labor shortages and stringent environmental regulations (such as ARYZTA's carbon pricing risks under EU frameworks).

While a hypothetical cross-border M&A synergy between ARYZTA’s global B2B capabilities and Flowers Foods' North American DSD retail dominance would theoretically create an unassailable vertical giant, the financial realities prohibit it. Flowers Foods' heavy debt burden and looming intangible asset impairments fundamentally clash with ARYZTA's strategic deleveraging mandate. Moving forward into late 2025 and 2026, sector winners will be defined not by top-line M&A volume, but by the ability to execute rigorous cost optimization and maintain organic pricing power in the face of shifting dietary habits.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Bakery Giants Face-Off: ARYZTA vs. Flowers Foods

Growth Engines: Organic Resilience vs. Structural M&A ExpansionA penetration analysis of both companies' revenue streams reveals a stark contrast in growth quality. ARYZTA’s growth logic is fundamentally rooted in an "innovation premium." By deploying advanced lamination production lines across Europe and focusing on its high-margin "Bake-off" B2B solutions, ARYZTA generated 19% of its annual revenue from innovative new products. This strategy allows its downstream Quick Service Restaurant (QSR) clients to drastically reduce labor costs, thereby granting ARYZTA pricing power and robust organic growth despite inflationary pressures.

Conversely, Flowers Foods' nominal 3.0% revenue growth is largely an accounting illusion. When adjusting for the $214 million revenue contribution from its premium Simple Mills acquisition and the favorable accounting timing of a 53rd week, the company's underlying organic growth is negative, plagued by a 2.0% volume contraction. Traditional packaged bread is losing shelf dominance, forcing Flowers Foods into a high-premium M&A strategy to buy its way into the "Better-for-you" healthy snack corridor. Ultimately, ARYZTA’s endogenous growth model demonstrates superior immunity to macroeconomic volatility compared to Flowers Foods' reliance on inorganic expansion.

Strategic Moats and Cyclical Headwinds

The defensive capabilities of these two baking giants stem from fundamentally different strategic moats, exposing them to unique systemic risks.

ARYZTA has constructed a formidable B2B moat through deep supply chain integration. With 52% of its revenue derived from food service and QSRs, its production facilities are deeply embedded into the operational frameworks of global chains. This creates extraordinarily high switching costs for clients. Furthermore, ARYZTA benefits from geographic hedging. While facing margin pressures in Europe due to labor inflation, its "Rest of World" (ROW) segment—covering regions like Asia-Pacific—acts as a cash cow, boasting a stellar 20.9% EBITDA margin.

Flowers Foods, while commanding unparalleled brand penetration and a dominant Direct Store Delivery (DSD) network in the US, suffers from 100% single-market exposure. This geographical concentration amplifies its vulnerability to domestic cyclical headwinds. The company is actively battling a consumer downgrade shift toward lower-margin private labels. More structurally, Flowers Foods faces an unprecedented threat from the rise of GLP-1 appetite-suppressing medications, which poses a long-term risk of suppressing baseline carbohydrate consumption.

Capital Allocation Efficiency and Financial Health

The most glaring divergence between the two industry leaders lies in their capital allocation efficiency and balance sheet management.

ARYZTA is executing a disciplined, McKinsey-style financial restructuring. By directing its free cash flow toward hybrid bond buybacks, it has successfully driven its net debt-to-EBITDA leverage down to a healthy 2.6x, with a clear trajectory toward 1.5x-2.0x. This asset-light optimization ensures high returns on invested capital (ROIC) and robust interest coverage.

Flowers Foods, however, is executing a high-stakes financial gamble. To fund its Simple Mills acquisition, the company has heavily leveraged its balance sheet, causing its leverage ratio to spike to a precarious 5.1x and its interest expenses to surge by 202%. Despite a 66% drop in net income, management maintained aggressive shareholder dividend payouts ($209 million) and initiated a massive $325 million ERP IT system upgrade. HDIN Research warns of significant impairment landmines: Flowers Foods has already recognized $136 million in regional brand impairments, and its $368 million goodwill from Simple Mills sits at a razor-thin 7.9% fair value premium above book value. Any minor downward revision in earnings could trigger a massive goodwill write-off.

HDIN Viewpoint: Navigating the Industry's Growth Ceiling

From the perspective of HDIN Research, the bakery sector's competition has evolved from mere capacity expansion to a dual battle for "supply chain depth" and "digital/ESG compliance." Both companies are forced to pivot their CapEx toward automation and green infrastructure to combat structural labor shortages and stringent environmental regulations (such as ARYZTA's carbon pricing risks under EU frameworks).

While a hypothetical cross-border M&A synergy between ARYZTA’s global B2B capabilities and Flowers Foods' North American DSD retail dominance would theoretically create an unassailable vertical giant, the financial realities prohibit it. Flowers Foods' heavy debt burden and looming intangible asset impairments fundamentally clash with ARYZTA's strategic deleveraging mandate. Moving forward into late 2025 and 2026, sector winners will be defined not by top-line M&A volume, but by the ability to execute rigorous cost optimization and maintain organic pricing power in the face of shifting dietary habits.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com