Quantum Computing Inc. (QCI) 2025 Strategic Analysis: Bridging the Gap Between Quantum Photonics and Commercial Realities

Date : 2026-03-06

Reading : 148

Quantum Computing Inc. (QCI) is navigating a pivotal transition from pure-play laboratory research to a vertically integrated commercial enterprise. Supported by a staggering $1.475 billion in private financing in 2025, QCI has constructed a formidable liquidity moat. However, an 83% top-line growth to $682,000 juxtaposed against a $51.1 million operating loss underscores a classic early-stage paradigm: survival and expansion are currently dictated by capital allocation efficiency rather than organic operational cash flow.

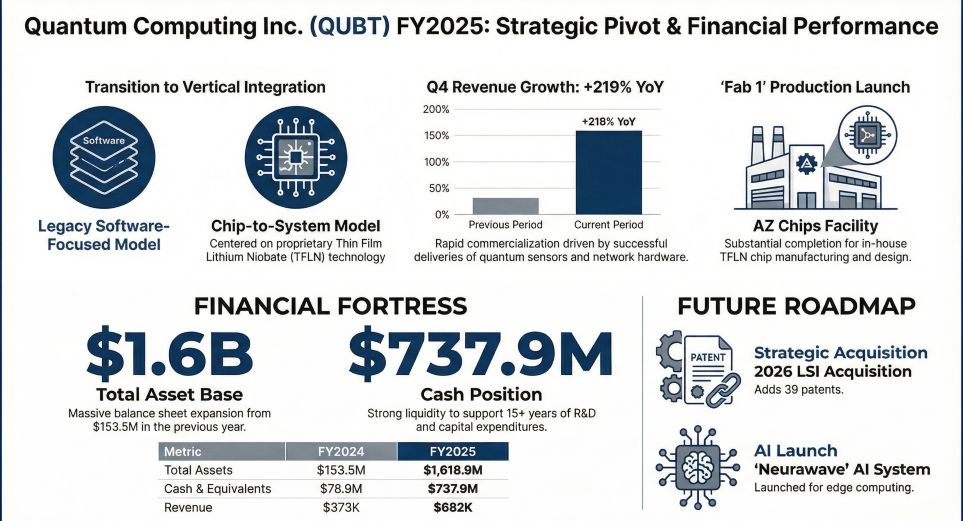

Figure Quantum Computing Inc (QUBT) FY2025 Strategic Pivot & Financial Performance

Financial Health: Capital Allocation Efficiency vs. Operational Cash Burn

Financial Health: Capital Allocation Efficiency vs. Operational Cash Burn

A surface-level reading of QCI’s 2025 financials reveals an optical narrowing of net losses—down to $18.67 million from $68.54 million in 2024. However, the strategic implications beneath the data paint a different picture. This improvement was entirely driven by non-operating mechanisms, specifically $20.7 million in interest income from their massive cash reserves and an $11.75 million gain from derivative liability fair value adjustments.

Operationally, the company is experiencing the friction typical of early hardware scaling. Gross margins compressed dramatically from 30% to 10%, a direct result of the high assembly and testing costs associated with their first-generation hardware deliveries, such as the quantum photonic vibrometers. The sheer magnitude of their cash reserves—totaling approximately $1.5 billion across cash and investments—grants QCI an extended runway. This financial resilience is critical to absorbing the heavy capital expenditures required for the ongoing expansion of their AZ Chips Facility and the planned "Fab 2" mass-production plant.

Strategic Pivots: Building the TFLN Photonics Moat

While industry titans like IBM and Google bet heavily on superconducting technologies requiring complex, cryogenic cooling infrastructure, QCI is carving out a distinct sector positioning. The company's strategic moat is built upon Thin Film Lithium Niobate (TFLN) integrated photonics and Entropy Quantum Computing (EQC). By manipulating photons to solve complex optimization problems, QCI’s Dirac-3 systems can operate at room temperature with minimal power consumption, allowing integration into standard server racks.

To solidify this vertical "chip-to-cloud" ecosystem, QCI executed a highly strategic pivot in February 2026 by acquiring Luminar Semiconductor (LSI) for $110 million. The strategic implication of this M&A activity is twofold: it vertically integrates critical ASIC design and photonic packaging capabilities, and it exponentially expands QCI's intellectual property portfolio. Furthermore, the establishment of the AZ Chips Facility allows QCI to diversify its revenue streams, transforming from a pure systems seller into a B2B TFLN foundry service provider.

Cyclical Headwinds & Geopolitical Supply Chain Risks

Despite its technological differentiation, QCI faces severe macro and geopolitical headwinds. The company's supply chain for critical TFLN chips is highly concentrated in East Asia, specifically China (including Taiwan, China). In an era of escalating trade protectionism, this geographic dependence is a significant vulnerability. Stringent U.S. export controls—such as the BIS regulations enacted in September 2024—and potential tariff escalations present material threats to continuous manufacturing and product development.

Furthermore, internal governance remains a friction point. Management has acknowledged material weaknesses in internal controls over financial reporting (ICFR), specifically regarding risk assessment and IT protocols. As QCI aggressively targets a highly ambitious executive compensation milestone of $30 million in revenue for 2026, mitigating these internal and external risks will be paramount to preventing execution failure.

HDIN Viewpoint

From an institutional perspective, HDIN Research views QCI as a high-beta play on non-cryogenic quantum architectures. The company has successfully weaponized its equity to build a fortress balance sheet, effectively eliminating short-term liquidity risks. However, the aggressive 2026 revenue target of $30 million—representing an astronomical leap from 2025's $682,000 baseline—suggests management is relying heavily on inorganic growth via M&A integration and front-loaded, multi-month contracts. For QCI to mature from a capital-consuming disruptor into a sustainable tech leader, it must flawlessly execute the commercial scaling of its TFLN chips while aggressively diversifying its concentrated supply chain to insulate against inevitable geopolitical shocks.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Quantum Computing Inc (QUBT) FY2025 Strategic Pivot & Financial Performance

Financial Health: Capital Allocation Efficiency vs. Operational Cash BurnA surface-level reading of QCI’s 2025 financials reveals an optical narrowing of net losses—down to $18.67 million from $68.54 million in 2024. However, the strategic implications beneath the data paint a different picture. This improvement was entirely driven by non-operating mechanisms, specifically $20.7 million in interest income from their massive cash reserves and an $11.75 million gain from derivative liability fair value adjustments.

Operationally, the company is experiencing the friction typical of early hardware scaling. Gross margins compressed dramatically from 30% to 10%, a direct result of the high assembly and testing costs associated with their first-generation hardware deliveries, such as the quantum photonic vibrometers. The sheer magnitude of their cash reserves—totaling approximately $1.5 billion across cash and investments—grants QCI an extended runway. This financial resilience is critical to absorbing the heavy capital expenditures required for the ongoing expansion of their AZ Chips Facility and the planned "Fab 2" mass-production plant.

Strategic Pivots: Building the TFLN Photonics Moat

While industry titans like IBM and Google bet heavily on superconducting technologies requiring complex, cryogenic cooling infrastructure, QCI is carving out a distinct sector positioning. The company's strategic moat is built upon Thin Film Lithium Niobate (TFLN) integrated photonics and Entropy Quantum Computing (EQC). By manipulating photons to solve complex optimization problems, QCI’s Dirac-3 systems can operate at room temperature with minimal power consumption, allowing integration into standard server racks.

To solidify this vertical "chip-to-cloud" ecosystem, QCI executed a highly strategic pivot in February 2026 by acquiring Luminar Semiconductor (LSI) for $110 million. The strategic implication of this M&A activity is twofold: it vertically integrates critical ASIC design and photonic packaging capabilities, and it exponentially expands QCI's intellectual property portfolio. Furthermore, the establishment of the AZ Chips Facility allows QCI to diversify its revenue streams, transforming from a pure systems seller into a B2B TFLN foundry service provider.

Cyclical Headwinds & Geopolitical Supply Chain Risks

Despite its technological differentiation, QCI faces severe macro and geopolitical headwinds. The company's supply chain for critical TFLN chips is highly concentrated in East Asia, specifically China (including Taiwan, China). In an era of escalating trade protectionism, this geographic dependence is a significant vulnerability. Stringent U.S. export controls—such as the BIS regulations enacted in September 2024—and potential tariff escalations present material threats to continuous manufacturing and product development.

Furthermore, internal governance remains a friction point. Management has acknowledged material weaknesses in internal controls over financial reporting (ICFR), specifically regarding risk assessment and IT protocols. As QCI aggressively targets a highly ambitious executive compensation milestone of $30 million in revenue for 2026, mitigating these internal and external risks will be paramount to preventing execution failure.

HDIN Viewpoint

From an institutional perspective, HDIN Research views QCI as a high-beta play on non-cryogenic quantum architectures. The company has successfully weaponized its equity to build a fortress balance sheet, effectively eliminating short-term liquidity risks. However, the aggressive 2026 revenue target of $30 million—representing an astronomical leap from 2025's $682,000 baseline—suggests management is relying heavily on inorganic growth via M&A integration and front-loaded, multi-month contracts. For QCI to mature from a capital-consuming disruptor into a sustainable tech leader, it must flawlessly execute the commercial scaling of its TFLN chips while aggressively diversifying its concentrated supply chain to insulate against inevitable geopolitical shocks.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com