Berkshire Hathaway 2025: The Abel Era, Structural Moats, and the $369B Liquidity Fortress

Date : 2026-03-06

Reading : 238

Berkshire Hathaway’s 2025 fiscal year marks a definitive inflection point in corporate governance and capital allocation. With Greg Abel officially assuming the CEO mantle on January 1, 2026, the conglomerate has solidified its transition from a founder-led stock-picking engine to an institutionally managed industrial powerhouse. HDIN Research's deep-dive analysis of the 2025 Annual Report reveals that while extreme macro-caution has driven cash and short-term treasuries to an unprecedented $369 billion, the company's underlying engine—$176 billion in negative-cost insurance float—continues to fuel aggressive capital expenditure in high-barrier infrastructure moats.

Figure Berkshire Hathaway 2025: Financial Performance & The Abel Transition

Capital Allocation Efficiency: The Power of Negative-Cost Leverage

Capital Allocation Efficiency: The Power of Negative-Cost Leverage

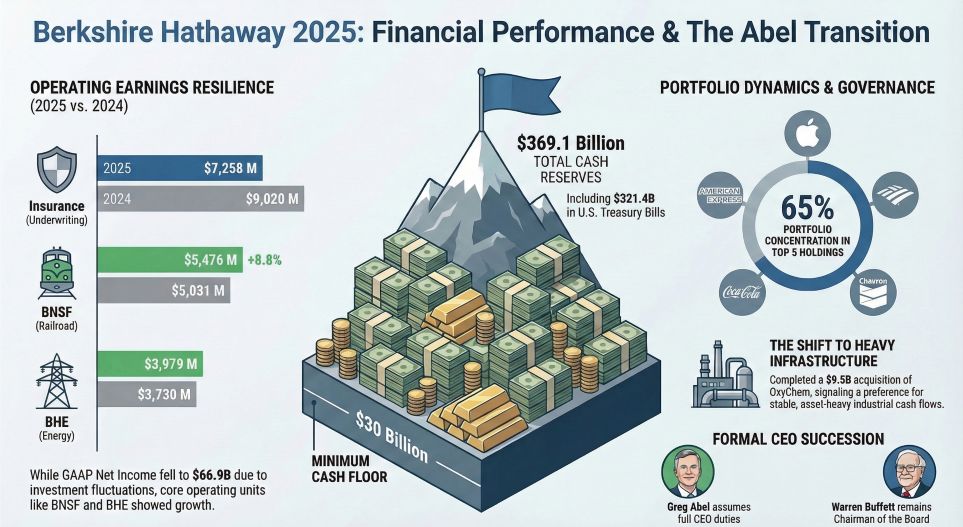

Rather than merely hoarding cash, Berkshire’s balance sheet reflects a highly disciplined response to cyclical headwinds and stretched global asset valuations. By the end of 2025, the company amassed $369.15 billion in cash, cash equivalents, and U.S. Treasury Bills.

The strategic implication here is profound: this liquidity fortress is entirely underwritten by $176 billion in insurance float. Crucially, this capital operates at a *negative cost*. Berkshire recorded $7.25 billion in after-tax underwriting profit in 2025, effectively being paid to hold investable capital. This unique capital structure allows management to maintain absolute financial resilience against catastrophe risks—such as the $360 million hit to GEICO from Hurricanes Helene and Milton—while preserving the "dry powder" necessary for opportunistic acquisitions during potential market dislocations.

Strategic Pivots: Infrastructure and Deterministic Compounding

Under Greg Abel’s leadership, Berkshire’s capital allocation has distinctly pivoted toward "deterministic compounding"—prioritizing heavy-asset, regulated infrastructure over volatile equity markets.

In 2025, capital expenditures surged to $20.92 billion, predominantly channeled into Berkshire Hathaway Energy (BHE) and BNSF Railway. BHE absorbed $10.58 billion to accelerate renewable energy grid modernization, capitalizing on policy tailwinds like the OBBBA tax credits to deepen its regional monopoly. Concurrently, BNSF deployed $3.79 billion to optimize network efficiency. Despite flat freight volumes, BNSF achieved an 8.8% net profit growth through aggressive operating ratio improvements and cost rationalization.

Furthermore, the $9.5 billion acquisition of Occidental Petroleum’s OxyChem business in January 2026 exemplifies Abel’s stringent M&A criteria: acquiring cash-flow-generative, heavy-industrial assets with insurmountable industry entry barriers.

Sector Positioning and Systemic Risk Exposure

Despite its fortified balance sheet, Berkshire’s 2025 financials expose vulnerabilities to systemic risks and extreme asset concentration. While GAAP net income stood at $66.96 billion (down from $88.99 billion in 2024), this metric was heavily distorted by $8.25 billion in non-temporary impairments related to Kraft Heinz and Occidental, alongside unrealized equity losses.

HDIN Research notes three primary cyclical and structural headwinds:

1. Equity Concentration Risk: 65% of Berkshire’s $297.78 billion equity portfolio is concentrated in just five mega-caps (American Express, Apple, Bank of America, Coca-Cola, Chevron), exposing the conglomerate to immense beta risk in a high-interest-rate environment.

2. Climate Litigation Liabilities: Environmental risks have materialized into severe financial burdens. BHE’s PacifiCorp has accrued $2.85 billion in estimated wildfire-related litigation losses, highlighting the escalating regulatory and legal costs of operating western U.S. utilities.

3. Retail Consumer Softness: Sustained high interest rates have compressed consumer durables demand, resulting in a 1.1% revenue contraction across Berkshire's retail and services segments.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Berkshire Hathaway's 2025 performance as a masterclass in downside protection. The official commencement of the "Abel Era" signals a strategic shift from pure equity arbitrage to the meticulous operational optimization of industrial and energy assets. However, the ultimate test for the new leadership will be the efficient deployment of its $369 billion liquidity pool. While utilizing U.S. Treasuries provides peak defensive yields in the short term, holding over 30% of total assets in low-yielding cash equivalents risks diluting long-term Return on Equity (ROE). Investors should look beyond GAAP net income fluctuations and focus strictly on operating earnings and the proactive management of insurance underwriting margins.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Berkshire Hathaway 2025: Financial Performance & The Abel Transition

Capital Allocation Efficiency: The Power of Negative-Cost LeverageRather than merely hoarding cash, Berkshire’s balance sheet reflects a highly disciplined response to cyclical headwinds and stretched global asset valuations. By the end of 2025, the company amassed $369.15 billion in cash, cash equivalents, and U.S. Treasury Bills.

The strategic implication here is profound: this liquidity fortress is entirely underwritten by $176 billion in insurance float. Crucially, this capital operates at a *negative cost*. Berkshire recorded $7.25 billion in after-tax underwriting profit in 2025, effectively being paid to hold investable capital. This unique capital structure allows management to maintain absolute financial resilience against catastrophe risks—such as the $360 million hit to GEICO from Hurricanes Helene and Milton—while preserving the "dry powder" necessary for opportunistic acquisitions during potential market dislocations.

Strategic Pivots: Infrastructure and Deterministic Compounding

Under Greg Abel’s leadership, Berkshire’s capital allocation has distinctly pivoted toward "deterministic compounding"—prioritizing heavy-asset, regulated infrastructure over volatile equity markets.

In 2025, capital expenditures surged to $20.92 billion, predominantly channeled into Berkshire Hathaway Energy (BHE) and BNSF Railway. BHE absorbed $10.58 billion to accelerate renewable energy grid modernization, capitalizing on policy tailwinds like the OBBBA tax credits to deepen its regional monopoly. Concurrently, BNSF deployed $3.79 billion to optimize network efficiency. Despite flat freight volumes, BNSF achieved an 8.8% net profit growth through aggressive operating ratio improvements and cost rationalization.

Furthermore, the $9.5 billion acquisition of Occidental Petroleum’s OxyChem business in January 2026 exemplifies Abel’s stringent M&A criteria: acquiring cash-flow-generative, heavy-industrial assets with insurmountable industry entry barriers.

Sector Positioning and Systemic Risk Exposure

Despite its fortified balance sheet, Berkshire’s 2025 financials expose vulnerabilities to systemic risks and extreme asset concentration. While GAAP net income stood at $66.96 billion (down from $88.99 billion in 2024), this metric was heavily distorted by $8.25 billion in non-temporary impairments related to Kraft Heinz and Occidental, alongside unrealized equity losses.

HDIN Research notes three primary cyclical and structural headwinds:

1. Equity Concentration Risk: 65% of Berkshire’s $297.78 billion equity portfolio is concentrated in just five mega-caps (American Express, Apple, Bank of America, Coca-Cola, Chevron), exposing the conglomerate to immense beta risk in a high-interest-rate environment.

2. Climate Litigation Liabilities: Environmental risks have materialized into severe financial burdens. BHE’s PacifiCorp has accrued $2.85 billion in estimated wildfire-related litigation losses, highlighting the escalating regulatory and legal costs of operating western U.S. utilities.

3. Retail Consumer Softness: Sustained high interest rates have compressed consumer durables demand, resulting in a 1.1% revenue contraction across Berkshire's retail and services segments.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Berkshire Hathaway's 2025 performance as a masterclass in downside protection. The official commencement of the "Abel Era" signals a strategic shift from pure equity arbitrage to the meticulous operational optimization of industrial and energy assets. However, the ultimate test for the new leadership will be the efficient deployment of its $369 billion liquidity pool. While utilizing U.S. Treasuries provides peak defensive yields in the short term, holding over 30% of total assets in low-yielding cash equivalents risks diluting long-term Return on Equity (ROE). Investors should look beyond GAAP net income fluctuations and focus strictly on operating earnings and the proactive management of insurance underwriting margins.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com