Viking Holdings (VIK): Unpacking the Defense Barriers and Growth Drivers in Luxury Travel

Date : 2026-03-06

Reading : 552

At the intersection of demographic shifts and experiential luxury lies Viking Holdings Ltd (VIK). In fiscal 2025, Viking recorded a 21.9% revenue surge to $6.501 billion. However, this top-line expansion is not merely a function of post-pandemic market recovery; it is the direct outcome of a highly disciplined business model. By combining a "thinking person's" demographic focus with unprecedented control over physical port assets, Viking has solidified a commanding 52% market share in the North American-to-Europe river cruise segment, effectively rewriting the economics of luxury travel.

Figure Viking Cruises 2026 Strategic Outlook & Financial Visibility

Sector Positioning and Strategic Moats

Sector Positioning and Strategic Moats

Viking’s sector positioning is distinctively isolated from the commoditized mass-market cruise industry. By eschewing casinos, children's clubs, and massive entertainment facilities in favor of cultural enrichment and all-balcony suites, Viking commands a structural pricing premium. This spatial reallocation and transparent, all-inclusive pricing model generated a robust net yield of $583 and an exceptional total revenue per passenger of $8,213 in 2025.

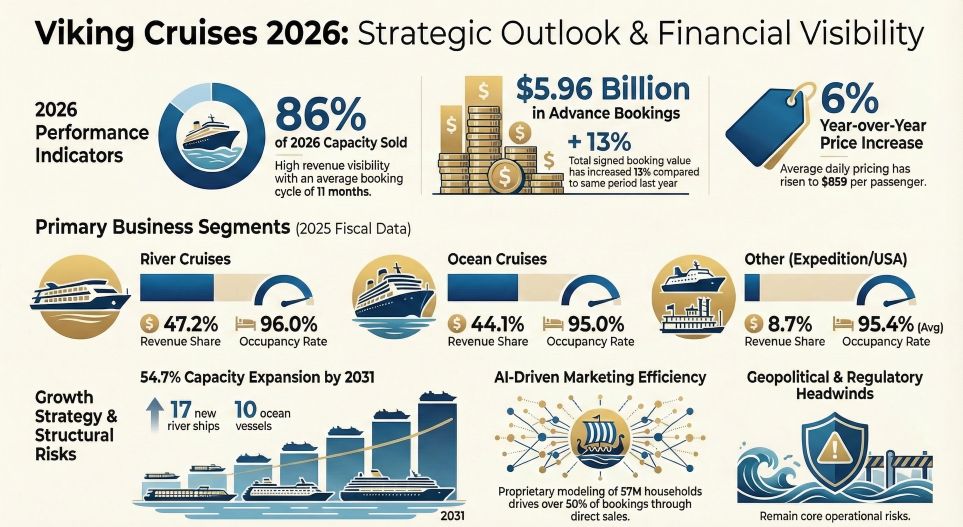

Beyond its targeted brand positioning, Viking's strategic moats are fortified by both data sovereignty and irreplaceable physical infrastructure. On the digital front, its proprietary database of 57 million North American households drives a direct-booking rate of over 50%, fundamentally reducing margin leakage to third-party travel agencies. Physically, the company controls 83 premium berths across Europe and Egypt—a geographic monopoly granting exclusive docking rights steps away from iconic landmarks like the Eiffel Tower and Karnak Temple. Coupled with an industry-leading 54% repeat guest rate, these hard and soft moats severely elevate the barrier to entry for prospective competitors.

Financial Health and Capital Allocation Efficiency

Viking’s financial architecture is engineered around high revenue visibility and a negative working capital model. As of mid-February 2026, Viking had already sold 86% of its 2026 capacity, locking in $5.96 billion in advance bookings at a 6% pricing premium ($859 per passenger cruise day). This extensive 11-month booking lead time generates massive deferred revenue—reaching $4.605 billion at the end of 2025—which serves as a zero-cost liquidity buffer for ongoing operations.

From the lens of capital allocation efficiency, Viking elegantly balances its ambitious growth pipeline with prudent financing. The company plans to expand its berth capacity by 54.7% by 2031. To fund this, Viking leverages 80% LTV financing backed by SACE (the Italian export credit agency) to secure fixed-rate, government-guaranteed loans. Concurrently, it utilizes its robust $2.176 billion in adjusted free cash flow (as of FY2025) to cover the remaining equity portions and operational expenditures, minimizing the need for dilutive capital raises.

Navigating Cyclical Headwinds and Industry Outlook

Despite its premium market dominance, Viking is not immune to cyclical headwinds and macro-environmental friction. The company currently carries $5.67 billion in debt; while its capital structure was optimized post-IPO, future fleet financing remains sensitive to global interest rate volatility and tightening credit conditions.

Operationally, geopolitical dislocations present a persistent layer of risk. The permanent suspension of Russian waterways and the rerouting of Mediterranean itineraries due to Middle Eastern conflicts underscore the vulnerability of global maritime routes. Furthermore, intensifying ESG regulations—such as the EU's "Fit for 55"—necessitate ongoing capital expenditure for shore power integration and hybrid fuel technologies. While Viking possesses the youngest fleet in the industry (averaging 8 years), adapting to these climate mandates will test the company's ability to maintain high margins amid tightening environmental compliance.

HDIN Viewpoint

HDIN Research views Viking Holdings as a masterclass in market segmentation and yield maximization. The company's unique "adults-only, destination-focused" model successfully bypasses the hyper-competitive mass-market sector, insulating it from broad consumer discretionary downcycles due to its affluent, highly resilient 55+ demographic.

However, structural vulnerabilities remain. Viking's extreme reliance on the North American source market (accounting for nearly 90% of its guests) and the inherent fragility of European river operations to climate change (such as low water levels) require vigilant operational agility. Moving forward, Viking’s ability to successfully penetrate highly regulated and complex markets—such as the PVSA-restricted Mississippi River and the Asia Outbound segment via its China joint venture—will be the ultimate litmus test for transitioning from a regional powerhouse to a globally diversified luxury travel conglomerate.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Viking Cruises 2026 Strategic Outlook & Financial Visibility

Sector Positioning and Strategic MoatsViking’s sector positioning is distinctively isolated from the commoditized mass-market cruise industry. By eschewing casinos, children's clubs, and massive entertainment facilities in favor of cultural enrichment and all-balcony suites, Viking commands a structural pricing premium. This spatial reallocation and transparent, all-inclusive pricing model generated a robust net yield of $583 and an exceptional total revenue per passenger of $8,213 in 2025.

Beyond its targeted brand positioning, Viking's strategic moats are fortified by both data sovereignty and irreplaceable physical infrastructure. On the digital front, its proprietary database of 57 million North American households drives a direct-booking rate of over 50%, fundamentally reducing margin leakage to third-party travel agencies. Physically, the company controls 83 premium berths across Europe and Egypt—a geographic monopoly granting exclusive docking rights steps away from iconic landmarks like the Eiffel Tower and Karnak Temple. Coupled with an industry-leading 54% repeat guest rate, these hard and soft moats severely elevate the barrier to entry for prospective competitors.

Financial Health and Capital Allocation Efficiency

Viking’s financial architecture is engineered around high revenue visibility and a negative working capital model. As of mid-February 2026, Viking had already sold 86% of its 2026 capacity, locking in $5.96 billion in advance bookings at a 6% pricing premium ($859 per passenger cruise day). This extensive 11-month booking lead time generates massive deferred revenue—reaching $4.605 billion at the end of 2025—which serves as a zero-cost liquidity buffer for ongoing operations.

From the lens of capital allocation efficiency, Viking elegantly balances its ambitious growth pipeline with prudent financing. The company plans to expand its berth capacity by 54.7% by 2031. To fund this, Viking leverages 80% LTV financing backed by SACE (the Italian export credit agency) to secure fixed-rate, government-guaranteed loans. Concurrently, it utilizes its robust $2.176 billion in adjusted free cash flow (as of FY2025) to cover the remaining equity portions and operational expenditures, minimizing the need for dilutive capital raises.

Navigating Cyclical Headwinds and Industry Outlook

Despite its premium market dominance, Viking is not immune to cyclical headwinds and macro-environmental friction. The company currently carries $5.67 billion in debt; while its capital structure was optimized post-IPO, future fleet financing remains sensitive to global interest rate volatility and tightening credit conditions.

Operationally, geopolitical dislocations present a persistent layer of risk. The permanent suspension of Russian waterways and the rerouting of Mediterranean itineraries due to Middle Eastern conflicts underscore the vulnerability of global maritime routes. Furthermore, intensifying ESG regulations—such as the EU's "Fit for 55"—necessitate ongoing capital expenditure for shore power integration and hybrid fuel technologies. While Viking possesses the youngest fleet in the industry (averaging 8 years), adapting to these climate mandates will test the company's ability to maintain high margins amid tightening environmental compliance.

HDIN Viewpoint

HDIN Research views Viking Holdings as a masterclass in market segmentation and yield maximization. The company's unique "adults-only, destination-focused" model successfully bypasses the hyper-competitive mass-market sector, insulating it from broad consumer discretionary downcycles due to its affluent, highly resilient 55+ demographic.

However, structural vulnerabilities remain. Viking's extreme reliance on the North American source market (accounting for nearly 90% of its guests) and the inherent fragility of European river operations to climate change (such as low water levels) require vigilant operational agility. Moving forward, Viking’s ability to successfully penetrate highly regulated and complex markets—such as the PVSA-restricted Mississippi River and the Asia Outbound segment via its China joint venture—will be the ultimate litmus test for transitioning from a regional powerhouse to a globally diversified luxury travel conglomerate.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com