Sensor Sector 2026: Navigating EV Headwinds & A&D Growth

Date : 2026-03-07

Reading : 66

The global precision electronics and sensor industry has reached a critical inflection point of structural bifurcation. According to HDIN Research’s comprehensive FY2025 financial analysis of four sector leaders—CTS, Ralliant, Sensata, and VPG—the highly anticipated Electric Vehicle (EV) boom is facing severe cyclical headwinds, triggering massive valuation resets. Conversely, the Aerospace and Defense (A&D) sector has entered a resilient supercycle. For institutional investors and industry stakeholders, the data reveals a stark reality: survival and growth in 2026 will depend not on broad market tailwinds, but on meticulous capital allocation efficiency, strategic moats, and the agility to navigate geopolitical supply chain fragmentation.

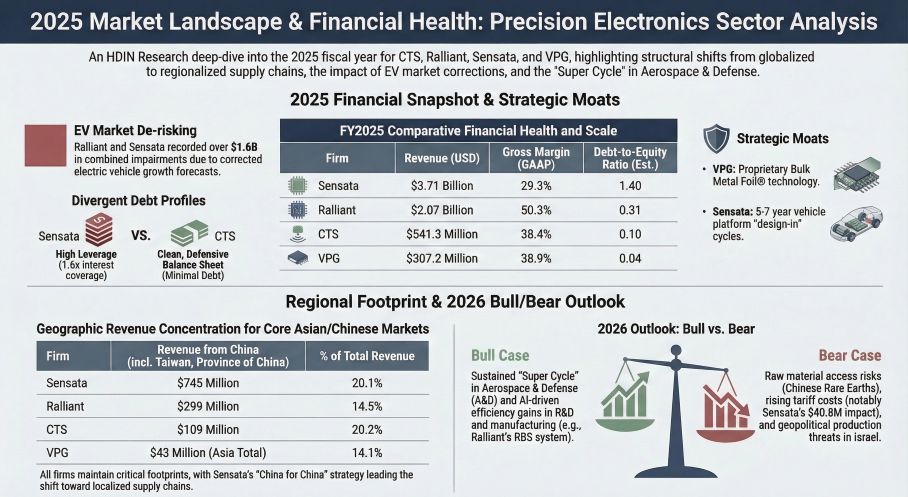

Figure 2025 Market Landscape & Financial Health: Precision Electronics Sector Analysis

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

A deep dive into the FY2025 balance sheets exposes profound disparities in financial elasticity and earnings quality across the sector. Rather than mere top-line fluctuations, the underlying narrative is driven by how management teams are allocating capital amidst macroeconomic volatility.

* The Valuation Reset: Both Ralliant and Sensata absorbed heavy blows from downward revisions in EV market forecasts. Ralliant recognized a staggering $1.44 billion goodwill impairment related to its EA Elektro-Automatik acquisition, while Sensata took a $226 million write-down on Dynapower. However, these "paper losses" mask robust core cash generation; Ralliant still delivered $398 million in operating cash flow (OCF), highlighting the underlying strength of its test and measurement (T&M) operations.

* The Deleveraging Mandate vs. Shareholder Returns: Sensata’s capital allocation is currently constrained by its $2.87 billion debt load, resulting in a precarious interest coverage ratio of 1.6x. In stark contrast, CTS emerges as the benchmark for financial health. Boasting an operating margin of 15.3% and a 5.2% revenue growth ($541 million), CTS maintains an exceptionally clean balance sheet, allowing it to aggressively execute a $100 million share repurchase program while expanding its high-margin medical and A&D portfolios.

Strategic Moats & Sector Positioning

In an era of commoditization, the competitive barriers in the precision electronics industry are heavily anchored in proprietary technology, extreme switching costs, and rigorous certification requirements.

* Vertical Monopolies: VPG continues to defend its niche ecosystem with its proprietary Bulk Metal® Foil technology, commanding a robust 38.9% gross margin despite flat top-line growth (+0.2%). Its design-in cycles, which often require 12-24 months of co-development, create formidable customer stickiness.

* The T&M Infrastructure Play: Ralliant’s sector positioning via brands like Tektronix and Keithley secures its role as a "pick-and-shovel" provider for the energy transition and semiconductor testing. Its industry-leading 50.3% gross margin is a direct reflection of knowledge-intensive pricing power, backed by 8.0% R&D intensity and an arsenal of over 2,200 patents.

* Transitioning from Components to Systems: Sensata is navigating a brutal transition from a traditional automotive component supplier to an EV power management systems integrator. The company leverages long 5-7 year platform lifecycles with OEMs, effectively locking in future revenue streams despite current margin compression (29.3% gross margin) driven by fierce OEM pricing pressures.

Cyclical Headwinds & Geopolitical Supply Chain Risks

Beyond cyclical EV demand shifts, geopolitical turbulence has morphed from a margin-eroding nuisance into an existential threat requiring structural supply chain decoupling.

* Strategic Decoupling: The "global factory" model is obsolete. Sensata is pioneering a highly localized "In China, for China" strategy—even shifting its functional currency to the RMB for local subsidiaries—to insulate its 20.1% revenue exposure in the region from US-China trade frictions.

* Vulnerabilities in the Supply Chain: Heavy reliance on Chinese rare earth elements (REEs) and specialized materials leaves companies like Ralliant and CTS exposed to single-source bottlenecks. Simultaneously, physical production risks are escalating; VPG’s core manufacturing footprint in Israel and CTS's exposure to European energy shocks stemming from the Russia-Ukraine conflict require massive investments in safety stock and redundant facilities.

* The Tariff Toll: The financial impact of trade barriers is immediate. Sensata absorbed and attempted to pass on $40.8 million in tariff-related costs in FY2025 alone. As companies relocate capacities to Mexico, India, or Bulgaria to bypass these tariffs, they face significant severance, startup costs, and temporary productivity losses.

HDIN Viewpoint

The precision electronics landscape is shifting from an era of aggressive M&A expansion to one of "refined operational execution." The $1.6+ billion in combined goodwill impairments across the sector signals that the aggressive premium paid for EV-transition assets was fundamentally mispriced.

HDIN Research posits that the true winners of the 2026 cycle will be those exhibiting structural cycle-hedging. CTS's strategic pivot toward the A&D and medical sectors perfectly offsets automotive cyclical headwinds, proving the efficacy of targeted diversification. Furthermore, as artificial intelligence transitions from a buzzword to an operational necessity, companies that successfully embed AI into their R&D and manufacturing workflows—such as Ralliant’s AI-injected Ralliant Business System (RBS)—will secure a definitive margin advantage. Investors must look beyond GAAP earnings, stripping away restructuring costs and non-cash impairments, to evaluate these companies purely on free cash flow generation and geopolitical resilience.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Market Landscape & Financial Health: Precision Electronics Sector Analysis

Financial Health & Capital Allocation EfficiencyA deep dive into the FY2025 balance sheets exposes profound disparities in financial elasticity and earnings quality across the sector. Rather than mere top-line fluctuations, the underlying narrative is driven by how management teams are allocating capital amidst macroeconomic volatility.

* The Valuation Reset: Both Ralliant and Sensata absorbed heavy blows from downward revisions in EV market forecasts. Ralliant recognized a staggering $1.44 billion goodwill impairment related to its EA Elektro-Automatik acquisition, while Sensata took a $226 million write-down on Dynapower. However, these "paper losses" mask robust core cash generation; Ralliant still delivered $398 million in operating cash flow (OCF), highlighting the underlying strength of its test and measurement (T&M) operations.

* The Deleveraging Mandate vs. Shareholder Returns: Sensata’s capital allocation is currently constrained by its $2.87 billion debt load, resulting in a precarious interest coverage ratio of 1.6x. In stark contrast, CTS emerges as the benchmark for financial health. Boasting an operating margin of 15.3% and a 5.2% revenue growth ($541 million), CTS maintains an exceptionally clean balance sheet, allowing it to aggressively execute a $100 million share repurchase program while expanding its high-margin medical and A&D portfolios.

Strategic Moats & Sector Positioning

In an era of commoditization, the competitive barriers in the precision electronics industry are heavily anchored in proprietary technology, extreme switching costs, and rigorous certification requirements.

* Vertical Monopolies: VPG continues to defend its niche ecosystem with its proprietary Bulk Metal® Foil technology, commanding a robust 38.9% gross margin despite flat top-line growth (+0.2%). Its design-in cycles, which often require 12-24 months of co-development, create formidable customer stickiness.

* The T&M Infrastructure Play: Ralliant’s sector positioning via brands like Tektronix and Keithley secures its role as a "pick-and-shovel" provider for the energy transition and semiconductor testing. Its industry-leading 50.3% gross margin is a direct reflection of knowledge-intensive pricing power, backed by 8.0% R&D intensity and an arsenal of over 2,200 patents.

* Transitioning from Components to Systems: Sensata is navigating a brutal transition from a traditional automotive component supplier to an EV power management systems integrator. The company leverages long 5-7 year platform lifecycles with OEMs, effectively locking in future revenue streams despite current margin compression (29.3% gross margin) driven by fierce OEM pricing pressures.

Cyclical Headwinds & Geopolitical Supply Chain Risks

Beyond cyclical EV demand shifts, geopolitical turbulence has morphed from a margin-eroding nuisance into an existential threat requiring structural supply chain decoupling.

* Strategic Decoupling: The "global factory" model is obsolete. Sensata is pioneering a highly localized "In China, for China" strategy—even shifting its functional currency to the RMB for local subsidiaries—to insulate its 20.1% revenue exposure in the region from US-China trade frictions.

* Vulnerabilities in the Supply Chain: Heavy reliance on Chinese rare earth elements (REEs) and specialized materials leaves companies like Ralliant and CTS exposed to single-source bottlenecks. Simultaneously, physical production risks are escalating; VPG’s core manufacturing footprint in Israel and CTS's exposure to European energy shocks stemming from the Russia-Ukraine conflict require massive investments in safety stock and redundant facilities.

* The Tariff Toll: The financial impact of trade barriers is immediate. Sensata absorbed and attempted to pass on $40.8 million in tariff-related costs in FY2025 alone. As companies relocate capacities to Mexico, India, or Bulgaria to bypass these tariffs, they face significant severance, startup costs, and temporary productivity losses.

HDIN Viewpoint

The precision electronics landscape is shifting from an era of aggressive M&A expansion to one of "refined operational execution." The $1.6+ billion in combined goodwill impairments across the sector signals that the aggressive premium paid for EV-transition assets was fundamentally mispriced.

HDIN Research posits that the true winners of the 2026 cycle will be those exhibiting structural cycle-hedging. CTS's strategic pivot toward the A&D and medical sectors perfectly offsets automotive cyclical headwinds, proving the efficacy of targeted diversification. Furthermore, as artificial intelligence transitions from a buzzword to an operational necessity, companies that successfully embed AI into their R&D and manufacturing workflows—such as Ralliant’s AI-injected Ralliant Business System (RBS)—will secure a definitive margin advantage. Investors must look beyond GAAP earnings, stripping away restructuring costs and non-cash impairments, to evaluate these companies purely on free cash flow generation and geopolitical resilience.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com