The JBT Marel Merger: Re-engineering Global Food Technology and Navigating the 2025 Financial Pivot

Date : 2026-03-08

Reading : 647

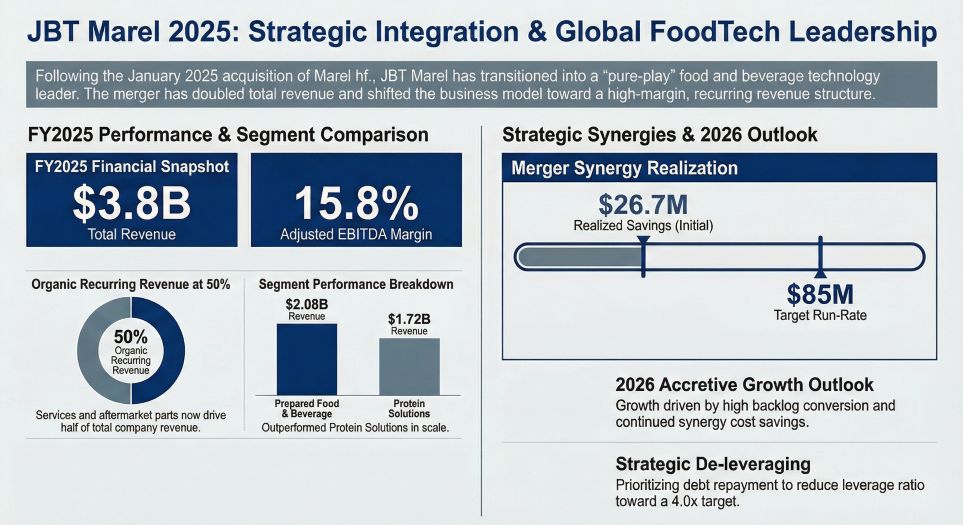

The 2025 strategic acquisition of Marel hf. by JBT Corporation marks a watershed moment in the global food processing technology sector. While surface-level metrics highlight a GAAP net loss of $50.5 million, a deeper penetration of the balance sheet reveals a different narrative. The consolidation catalyzed a 121.3% revenue surge to $3.798 billion, fundamentally redefining the newly formed JBT Marel's sector positioning. By transforming into a "pure-play" food and beverage solutions provider, the company has established formidable strategic moats, utilizing a high-margin recurring revenue model and scale-driven operational efficiencies to offset macroeconomic turbulence.

Figure JBT Marel 2025: Strategic Integration & Global FoodTech Leadership

Sector Positioning and Strategic Pivots

Sector Positioning and Strategic Pivots

Following the divestiture of its AeroTech business, JBT Marel has successfully restructured its operational architecture to achieve full value-chain coverage. The company now operates through two synergistic reporting segments, heavily empowered by the AXIN digital platform and Generative AI technologies:

* Protein Solutions: Generating $1.716 billion (45.2% of total revenue), this segment dominates the primary processing and harvesting of poultry, pork, fish, and beef. The integration of Marel’s advanced robotic sorting and bone-detection technologies has elevated its pricing power in large-scale greenfield projects.

* Prepared Food and Beverage Solutions: Accounting for $2.082 billion (54.8% of revenue), this division focuses on high-elasticity downstream markets. Through advanced automation, sterilization, and robotic Automated Guided Vehicles (AGVs), the segment addresses acute global labor shortages and operational efficiency demands.

Crucially, JBT Marel's global manufacturing footprint—comprising over 50 facilities—has been optimized for localized agility. For instance, the Suzhou facility in China (spanning 78,000 square feet) operates as a critical linchpin for the Protein Solutions segment in the Asia-Pacific, ensuring supply chain resilience and proximity to high-growth emerging markets.

Strategic Moats: The Power of Recurring Revenue

A defining outcome of the merger is the structural shift in the company's revenue quality. In 2025, recurring revenue—comprising aftermarket parts, services, software leases, and consumables—accounted for approximately 50% of total revenue.

*The "So What" Factor:* In the capital goods industry, primary equipment sales are notoriously vulnerable to long sales cycles and macroeconomic shocks. JBT Marel’s massive, active installed base functions as a highly lucrative profit cushion. This 50% recurring revenue stream acts as a vital strategic moat, effectively smoothing out cyclical headwinds, defending gross margins, and ensuring reliable cash flow even during periods of suppressed capital expenditures.

Financial Health and Capital Allocation Efficiency

The reported GAAP net loss of $50.5 million obscures a robust underlying operational vitality, evidenced by a 103.5% spike in Adjusted EBITDA to $600.4 million. The net loss was predominantly driven by a non-recurring $146.9 million pension settlement and a staggering $114.4 million in interest expenses tied to acquisition financing.

Consequently, management’s capital allocation efficiency has aggressively pivoted from share repurchases to deleveraging. With total long-term debt ballooning to $1.91 billion (a 54.5% debt-to-asset ratio), the immediate governance priority is retiring floating-rate debt and maximizing the "JBT Marel 2025 Integration Restructuring Plan." This operational overhaul aims to unlock $65 million to $75 million in annual run-rate cost savings, having already realized $26.7 million by the end of 2025. Furthermore, R&D expenditures have surged by 456.5% to $116.3 million, emphasizing a commitment to long-term technological supremacy over short-term dividend hikes.

Navigating Cyclical Headwinds and Integration Risks

Despite its dominant market share, JBT Marel is navigating a complex matrix of operational and geopolitical risks. The integration of two multinational behemoths brings inherent friction. Notably, pre-acquisition material weaknesses in Marel’s internal IT general controls (ITGC) demand stringent remediation to prevent future financial reporting misstatements.

Simultaneously, cyclical headwinds persist. Global trade tariffs and project execution inefficiencies within the Prepared Food division compressed overall gross margins by 140 basis points to 35.1% in 2025. Furthermore, the company's high leverage exposes it to interest rate volatility, where a mere 10% shift in rates could inflate annual interest burdens by over $5.3 million. Geopolitically, the ongoing crisis in Ukraine continues to exert upward pressure on European energy costs, testing the resilience of the company's EMEA operations.

HDIN Viewpoint

From an institutional perspective, HDIN Research views 2025 not as a year of structural decline, but as a necessary transitional trough for JBT Marel. The optical GAAP loss is a temporary byproduct of aggressive M&A accounting. The true leading indicator for 2026 is the company’s robust order backlog of $1.372 billion, of which 85% to 95% is projected to convert into actual revenue within the next twelve months.

If management successfully executes its post-merger integration—particularly by rectifying internal control deficiencies and unleashing projected cost synergies—JBT Marel is uniquely positioned to monopolize the "full-line provider" premium. The combination of its digital ecosystem (AXIN), high-margin aftermarket service model, and proactive deleveraging strategy provides a clear roadmap to profitability and sustained global dominance in 2026.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure JBT Marel 2025: Strategic Integration & Global FoodTech Leadership

Sector Positioning and Strategic PivotsFollowing the divestiture of its AeroTech business, JBT Marel has successfully restructured its operational architecture to achieve full value-chain coverage. The company now operates through two synergistic reporting segments, heavily empowered by the AXIN digital platform and Generative AI technologies:

* Protein Solutions: Generating $1.716 billion (45.2% of total revenue), this segment dominates the primary processing and harvesting of poultry, pork, fish, and beef. The integration of Marel’s advanced robotic sorting and bone-detection technologies has elevated its pricing power in large-scale greenfield projects.

* Prepared Food and Beverage Solutions: Accounting for $2.082 billion (54.8% of revenue), this division focuses on high-elasticity downstream markets. Through advanced automation, sterilization, and robotic Automated Guided Vehicles (AGVs), the segment addresses acute global labor shortages and operational efficiency demands.

Crucially, JBT Marel's global manufacturing footprint—comprising over 50 facilities—has been optimized for localized agility. For instance, the Suzhou facility in China (spanning 78,000 square feet) operates as a critical linchpin for the Protein Solutions segment in the Asia-Pacific, ensuring supply chain resilience and proximity to high-growth emerging markets.

Strategic Moats: The Power of Recurring Revenue

A defining outcome of the merger is the structural shift in the company's revenue quality. In 2025, recurring revenue—comprising aftermarket parts, services, software leases, and consumables—accounted for approximately 50% of total revenue.

*The "So What" Factor:* In the capital goods industry, primary equipment sales are notoriously vulnerable to long sales cycles and macroeconomic shocks. JBT Marel’s massive, active installed base functions as a highly lucrative profit cushion. This 50% recurring revenue stream acts as a vital strategic moat, effectively smoothing out cyclical headwinds, defending gross margins, and ensuring reliable cash flow even during periods of suppressed capital expenditures.

Financial Health and Capital Allocation Efficiency

The reported GAAP net loss of $50.5 million obscures a robust underlying operational vitality, evidenced by a 103.5% spike in Adjusted EBITDA to $600.4 million. The net loss was predominantly driven by a non-recurring $146.9 million pension settlement and a staggering $114.4 million in interest expenses tied to acquisition financing.

Consequently, management’s capital allocation efficiency has aggressively pivoted from share repurchases to deleveraging. With total long-term debt ballooning to $1.91 billion (a 54.5% debt-to-asset ratio), the immediate governance priority is retiring floating-rate debt and maximizing the "JBT Marel 2025 Integration Restructuring Plan." This operational overhaul aims to unlock $65 million to $75 million in annual run-rate cost savings, having already realized $26.7 million by the end of 2025. Furthermore, R&D expenditures have surged by 456.5% to $116.3 million, emphasizing a commitment to long-term technological supremacy over short-term dividend hikes.

Navigating Cyclical Headwinds and Integration Risks

Despite its dominant market share, JBT Marel is navigating a complex matrix of operational and geopolitical risks. The integration of two multinational behemoths brings inherent friction. Notably, pre-acquisition material weaknesses in Marel’s internal IT general controls (ITGC) demand stringent remediation to prevent future financial reporting misstatements.

Simultaneously, cyclical headwinds persist. Global trade tariffs and project execution inefficiencies within the Prepared Food division compressed overall gross margins by 140 basis points to 35.1% in 2025. Furthermore, the company's high leverage exposes it to interest rate volatility, where a mere 10% shift in rates could inflate annual interest burdens by over $5.3 million. Geopolitically, the ongoing crisis in Ukraine continues to exert upward pressure on European energy costs, testing the resilience of the company's EMEA operations.

HDIN Viewpoint

From an institutional perspective, HDIN Research views 2025 not as a year of structural decline, but as a necessary transitional trough for JBT Marel. The optical GAAP loss is a temporary byproduct of aggressive M&A accounting. The true leading indicator for 2026 is the company’s robust order backlog of $1.372 billion, of which 85% to 95% is projected to convert into actual revenue within the next twelve months.

If management successfully executes its post-merger integration—particularly by rectifying internal control deficiencies and unleashing projected cost synergies—JBT Marel is uniquely positioned to monopolize the "full-line provider" premium. The combination of its digital ecosystem (AXIN), high-margin aftermarket service model, and proactive deleveraging strategy provides a clear roadmap to profitability and sustained global dominance in 2026.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com