Hyundai ADM Bio FY2025 Diagnosis: A Precarious Pivot from Clinical CRO to Oncology Biotech

Date : 2026-03-08

Reading : 491

Hyundai ADM Bio is navigating a brutal transitional phase, attempting to evolve from a pure-play clinical Contract Research Organization (CRO) into an innovative, high-reward biopharmaceutical developer. While the recent Phase 1 IND approval for its proprietary oncology platform marks a critical developmental milestone, shrinking legacy revenues and an alarming 13-month cash runway expose the company to severe liquidity risks. The firm is currently racing against time to monetize its pipeline before its capital reserves evaporate.

Figure Hyundai ADM Bio 2025: The Strategic Pivot from CRo to Biotech

Financial Health: Deteriorating Operating Leverage and Liquidity Squeeze

Financial Health: Deteriorating Operating Leverage and Liquidity Squeeze

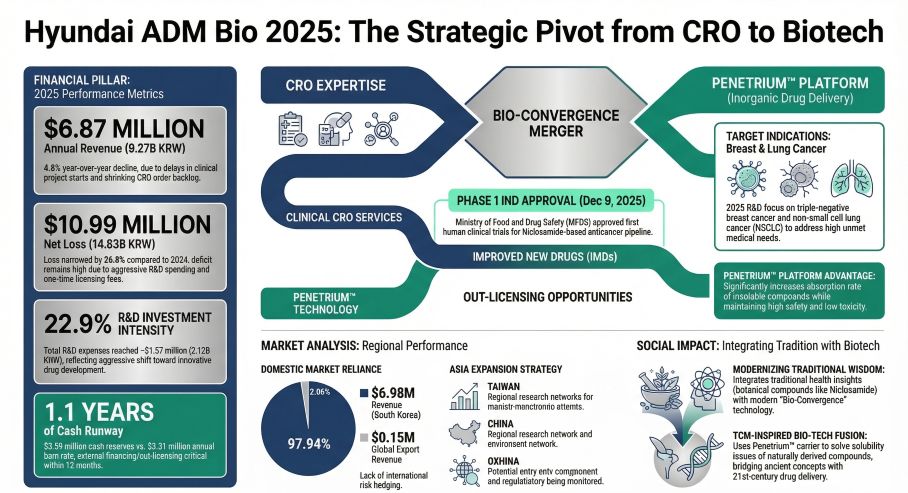

In FY2025, Hyundai ADM Bio reported a 4.8% top-line contraction, generating approximately $6.87 million in revenue. However, the strategic implication lies beneath the surface: the company’s gross margin has collapsed to an exceptionally vulnerable 0.36%. As a human-capital-intensive CRO where labor constitutes 70-80% of costs, the inability to scale down fixed expenses in tandem with declining project volumes has severely damaged its operating leverage.

The liquidity profile presents a pressing structural risk. With only about $3.59 million in available cash and equivalents, against an annual operating cash burn of roughly $3.31 million, the company’s cash runway is limited to merely 1.1 years. While debt-to-equity swaps via convertible bonds have optically deleveraged the balance sheet, the firm fundamentally lacks the internal cash generation required to sustain its capital-intensive R&D ambitions.

Strategic Pivots: The High-Stakes Penetrium™ Bet

The company’s future is now entirely tethered to its Penetrium™ platform—an inorganic-based drug delivery system (DDS) designed to improve the bioavailability and lower the toxicity of insoluble drugs like Niclosamide. In December 2025, the company successfully secured a Phase 1 IND approval from the MFDS, targeting solid tumors such as breast and non-small cell lung cancer (NSCLC).

While this proprietary technology aims to establish long-term strategic moats, the abrupt liquidation of its microneedle patch subsidiary in late 2024 highlights poor historical capital allocation efficiency. This previous failure has forced management into a singular, concentrated bet on the Penetrium™ platform. The ultimate commercial strategy is not direct manufacturing, but rather securing lucrative out-licensing agreements. Therefore, generating early efficacy and safety signals in Phase 1 is a non-negotiable prerequisite for survival.

Industry Outlook and Sector Positioning

Hyundai ADM Bio’s sector positioning is currently precarious as it straddles two distinct business models. The legacy CRO division—historically the company's "cash cow"—is experiencing significant erosion, evidenced by a 14% year-over-year drop in its order backlog (down to $14.17 million).

Furthermore, the CRO landscape is facing cyclical headwinds and a structural shift toward Decentralized Clinical Trials (DCTs) and AI-driven remote monitoring. Although Hyundai ADM Bio is attempting to integrate digital solutions into its Phase 4 (LPS) offerings to defend its domestic market share (which accounts for nearly 98% of its revenue), its lack of an international footprint restricts its bargaining power against global pharmaceutical giants.

Governance and Structural Dependencies

From a governance perspective, the company exhibits extreme strategic and financial reliance on its parent company and largest shareholder, Hyundai Bioscience. The core intellectual property driving the Penetrium™ pipeline is licensed exclusively from the parent, obligating Hyundai ADM Bio to up to $12.22 million in future milestone payments—a figure that drastically exceeds its current liquidity. To mitigate the flight risk of key scientific personnel during this critical Phase 1 window, the board has implemented aggressive stock option grants (over 1 million shares), utilizing equity as "golden handcuffs" to enforce talent retention.

HDIN Viewpoint

HDIN Research categorizes Hyundai ADM Bio as a highly speculative entity navigating a dangerous "valley of death." The underlying strategic rationale—leveraging steady CRO cash flows to fund high-margin drug discovery—is theoretically sound, but the execution window is rapidly closing as the legacy business contracts.

The firm's technical moats remain untested in human trials, and its survival is inextricably linked to the upcoming Phase 1 clinical readouts. We advise institutional investors and strategic partners to closely monitor the company's ability to execute a near-term out-licensing deal or secure substantial equity financing within the next 12 months. Without a rapid infusion of capital or external validation of the Penetrium™ platform, the company's operational continuity will face critical systemic failure.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Hyundai ADM Bio 2025: The Strategic Pivot from CRo to Biotech

Financial Health: Deteriorating Operating Leverage and Liquidity SqueezeIn FY2025, Hyundai ADM Bio reported a 4.8% top-line contraction, generating approximately $6.87 million in revenue. However, the strategic implication lies beneath the surface: the company’s gross margin has collapsed to an exceptionally vulnerable 0.36%. As a human-capital-intensive CRO where labor constitutes 70-80% of costs, the inability to scale down fixed expenses in tandem with declining project volumes has severely damaged its operating leverage.

The liquidity profile presents a pressing structural risk. With only about $3.59 million in available cash and equivalents, against an annual operating cash burn of roughly $3.31 million, the company’s cash runway is limited to merely 1.1 years. While debt-to-equity swaps via convertible bonds have optically deleveraged the balance sheet, the firm fundamentally lacks the internal cash generation required to sustain its capital-intensive R&D ambitions.

Strategic Pivots: The High-Stakes Penetrium™ Bet

The company’s future is now entirely tethered to its Penetrium™ platform—an inorganic-based drug delivery system (DDS) designed to improve the bioavailability and lower the toxicity of insoluble drugs like Niclosamide. In December 2025, the company successfully secured a Phase 1 IND approval from the MFDS, targeting solid tumors such as breast and non-small cell lung cancer (NSCLC).

While this proprietary technology aims to establish long-term strategic moats, the abrupt liquidation of its microneedle patch subsidiary in late 2024 highlights poor historical capital allocation efficiency. This previous failure has forced management into a singular, concentrated bet on the Penetrium™ platform. The ultimate commercial strategy is not direct manufacturing, but rather securing lucrative out-licensing agreements. Therefore, generating early efficacy and safety signals in Phase 1 is a non-negotiable prerequisite for survival.

Industry Outlook and Sector Positioning

Hyundai ADM Bio’s sector positioning is currently precarious as it straddles two distinct business models. The legacy CRO division—historically the company's "cash cow"—is experiencing significant erosion, evidenced by a 14% year-over-year drop in its order backlog (down to $14.17 million).

Furthermore, the CRO landscape is facing cyclical headwinds and a structural shift toward Decentralized Clinical Trials (DCTs) and AI-driven remote monitoring. Although Hyundai ADM Bio is attempting to integrate digital solutions into its Phase 4 (LPS) offerings to defend its domestic market share (which accounts for nearly 98% of its revenue), its lack of an international footprint restricts its bargaining power against global pharmaceutical giants.

Governance and Structural Dependencies

From a governance perspective, the company exhibits extreme strategic and financial reliance on its parent company and largest shareholder, Hyundai Bioscience. The core intellectual property driving the Penetrium™ pipeline is licensed exclusively from the parent, obligating Hyundai ADM Bio to up to $12.22 million in future milestone payments—a figure that drastically exceeds its current liquidity. To mitigate the flight risk of key scientific personnel during this critical Phase 1 window, the board has implemented aggressive stock option grants (over 1 million shares), utilizing equity as "golden handcuffs" to enforce talent retention.

HDIN Viewpoint

HDIN Research categorizes Hyundai ADM Bio as a highly speculative entity navigating a dangerous "valley of death." The underlying strategic rationale—leveraging steady CRO cash flows to fund high-margin drug discovery—is theoretically sound, but the execution window is rapidly closing as the legacy business contracts.

The firm's technical moats remain untested in human trials, and its survival is inextricably linked to the upcoming Phase 1 clinical readouts. We advise institutional investors and strategic partners to closely monitor the company's ability to execute a near-term out-licensing deal or secure substantial equity financing within the next 12 months. Without a rapid infusion of capital or external validation of the Penetrium™ platform, the company's operational continuity will face critical systemic failure.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com