Joby vs. Archer: Unpacking the Financial and Strategic Realities of the eVTOL Duopoly

Date : 2026-03-10

Reading : 780

The global Advanced Air Mobility (AAM) market has officially exited its conceptual phase and entered a grueling capital marathon. Based on the 2025 10-K filings of industry frontrunners Joby Aviation (NYSE: JOBY) and Archer Aviation (NYSE: ACHR), the narrative has shifted from prototype testing to rigorous FAA certification and high-volume manufacturing. Behind the flashy headlines of zero-emission flight, a profound structural divergence is unfolding. Ultimately, survival in this duopoly will not be dictated merely by flight hours, but by robust capital allocation efficiency, the mitigation of cyclical headwinds, and the ability to build impenetrable strategic moats.

Figure eVTOL Titans: The 2025 Financial and operational Duel

Sector Positioning: Vertical Integration vs. Asset-Light Ecosystems

Sector Positioning: Vertical Integration vs. Asset-Light Ecosystems

The "So What" Factor: Revenue in the eVTOL sector currently masks the underlying business models. Investors must look past top-line growth to understand how these companies are positioning themselves for the commercialization phase.

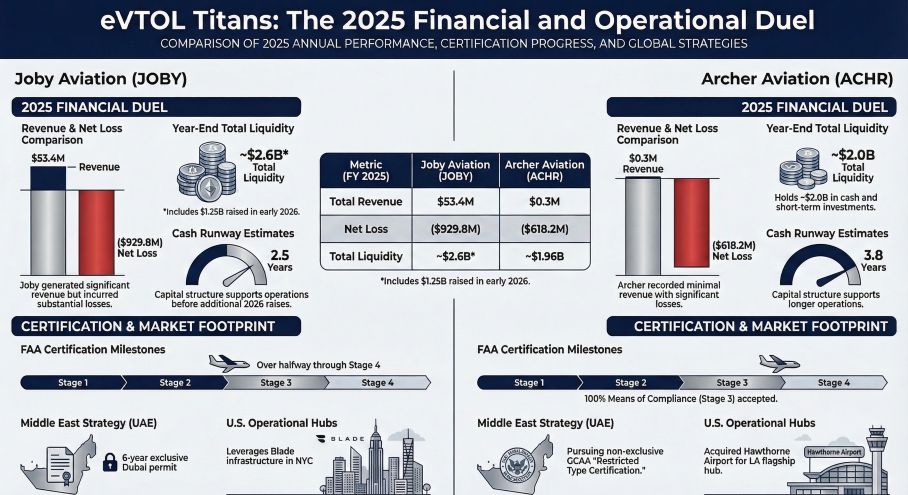

Joby Aviation is aggressively pursuing a vertically integrated, "operator-first" model. The company reported a substantial revenue surge to $53.4 million in 2025, up from just $136,000 in 2024. However, this was almost entirely driven by its acquisition of Blade Urban Air Mobility's passenger operations ($34.8 million) and government flight services. Joby is building an end-to-end ecosystem, developing its proprietary Elevate OS software, and securing exclusive operator rights—most notably a six-year exclusive commercial mandate in Dubai. While this strategy promises superior pricing power and SaaS-like margins at maturity, it requires intense, long-cycle capital expenditure (CapEx) today.

Conversely, Archer Aviation is adopting an asset-light, OEM-focused strategy built on ecosystem collaboration. Generating just $300,000 in revenue in 2025 (primarily from hangar subleasing at Hawthorne Airport), Archer remains in the pre-revenue phase for its core operations. Instead of funding vertical integration, Archer relies on deep manufacturing synergies with Stellantis and has structured its go-to-market strategy around massive B2B sales, highlighted by a conditional $1 billion order from United Airlines. This OEM approach allows Archer to shift manufacturing risk to its partners, achieving faster asset turnover and lowering its proprietary CapEx burden.

Financial Health & Capital Allocation Efficiency

The "So What" Factor: Net loss figures are heavily distorted by non-cash items. True operational efficiency is revealed only when stripping away stock-based compensation (SBC) and warrant liability fluctuations.

Both companies are navigating a period of maximum cash burn as they race to establish their "golden production lines" in Ohio (Joby) and Georgia (Archer).

* Archer reported a 2025 net loss of $618.2 million. However, after adjusting for $223.5 million in SBC and a $59.5 million warrant appreciation gain, the adjusted EBITDA loss narrows to approximately $454 million. Armed with a $1.96 billion liquidity pool, Archer’s current cash runway extends to roughly 3.8 years, showcasing strong capital elasticity.

* Joby posted a net loss of $929.8 million in 2025. Stripping out $127.9 million in SBC and a severe $211.9 million fair value loss on warrant liabilities, its adjusted EBITDA loss stands at around $550 million. While Joby’s heavy operational footprint initially restricted its cash runway to 2.5 years, a critical $1.25 billion public and convertible debt raise in early 2026 has temporarily alleviated its liquidity constraints.

The fundamental takeaway is that both balance sheets are under pressure. The massive reliance on SBC preserves cash but introduces severe equity dilution risks, acting as a hidden cost to long-term shareholders.

Cyclical Headwinds and Supply Chain Geopolitics

The "So What" Factor: Geopolitical friction is no longer an external risk; it is a direct threat to the eVTOL supply chain, capable of derailing both production timelines and FAA certification targets.

As these companies pivot to mass manufacturing, they face severe cyclical headwinds driven by macroeconomic and geopolitical instability. Both Joby and Archer rely heavily on global supply chains for critical battery minerals (lithium, cobalt, nickel) and electronic components. In 2025, surging tariffs and trade protectionism directly compressed expected manufacturing margins.

Furthermore, because eVTOL platforms hold dual-use defense capabilities (as evidenced by Joby’s Agility Prime DOD contracts and Archer’s dual-use drone development with Anduril), they are tightly bound by EAR and ITAR export controls. Joby’s international footprint, including R&D facilities in Shenzhen, China, exposes it to heightened data security scrutiny and intellectual property risks. Any disruption in this fragile supply web could result in stranded assets and idle manufacturing facilities.

HDIN Viewpoint: The Institutional Perspective

At HDIN Research, our analysis indicates that the eVTOL market is entering a phase of "survival of the best-funded." The true strategic moats in this space will not be built on battery density alone, but on legal certainties and infrastructure lock-ins.

Investors must remain highly skeptical of "paper wealth" on these balance sheets. Archer’s $1 billion United Airlines order is strictly a conditional contract liability dependent on FAA certification, while Joby carries significant goodwill impairment risks from its Blade acquisition. Joby currently holds a definitive first-mover advantage in commercialization due to its advanced Phase 4 FAA certification status and airtight legal monopoly in Dubai, making a 2026 commercial launch highly probable. However, Archer’s OEM-centric model provides a superior defense mechanism against certification delays, as it burns less cash maintaining an active flight infrastructure. Ultimately, the victor will be the firm that successfully transitions from a technology pioneer to an unyielding industrial manufacturer without falling victim to the equity dilution spiral.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure eVTOL Titans: The 2025 Financial and operational Duel

Sector Positioning: Vertical Integration vs. Asset-Light EcosystemsThe "So What" Factor: Revenue in the eVTOL sector currently masks the underlying business models. Investors must look past top-line growth to understand how these companies are positioning themselves for the commercialization phase.

Joby Aviation is aggressively pursuing a vertically integrated, "operator-first" model. The company reported a substantial revenue surge to $53.4 million in 2025, up from just $136,000 in 2024. However, this was almost entirely driven by its acquisition of Blade Urban Air Mobility's passenger operations ($34.8 million) and government flight services. Joby is building an end-to-end ecosystem, developing its proprietary Elevate OS software, and securing exclusive operator rights—most notably a six-year exclusive commercial mandate in Dubai. While this strategy promises superior pricing power and SaaS-like margins at maturity, it requires intense, long-cycle capital expenditure (CapEx) today.

Conversely, Archer Aviation is adopting an asset-light, OEM-focused strategy built on ecosystem collaboration. Generating just $300,000 in revenue in 2025 (primarily from hangar subleasing at Hawthorne Airport), Archer remains in the pre-revenue phase for its core operations. Instead of funding vertical integration, Archer relies on deep manufacturing synergies with Stellantis and has structured its go-to-market strategy around massive B2B sales, highlighted by a conditional $1 billion order from United Airlines. This OEM approach allows Archer to shift manufacturing risk to its partners, achieving faster asset turnover and lowering its proprietary CapEx burden.

Financial Health & Capital Allocation Efficiency

The "So What" Factor: Net loss figures are heavily distorted by non-cash items. True operational efficiency is revealed only when stripping away stock-based compensation (SBC) and warrant liability fluctuations.

Both companies are navigating a period of maximum cash burn as they race to establish their "golden production lines" in Ohio (Joby) and Georgia (Archer).

* Archer reported a 2025 net loss of $618.2 million. However, after adjusting for $223.5 million in SBC and a $59.5 million warrant appreciation gain, the adjusted EBITDA loss narrows to approximately $454 million. Armed with a $1.96 billion liquidity pool, Archer’s current cash runway extends to roughly 3.8 years, showcasing strong capital elasticity.

* Joby posted a net loss of $929.8 million in 2025. Stripping out $127.9 million in SBC and a severe $211.9 million fair value loss on warrant liabilities, its adjusted EBITDA loss stands at around $550 million. While Joby’s heavy operational footprint initially restricted its cash runway to 2.5 years, a critical $1.25 billion public and convertible debt raise in early 2026 has temporarily alleviated its liquidity constraints.

The fundamental takeaway is that both balance sheets are under pressure. The massive reliance on SBC preserves cash but introduces severe equity dilution risks, acting as a hidden cost to long-term shareholders.

Cyclical Headwinds and Supply Chain Geopolitics

The "So What" Factor: Geopolitical friction is no longer an external risk; it is a direct threat to the eVTOL supply chain, capable of derailing both production timelines and FAA certification targets.

As these companies pivot to mass manufacturing, they face severe cyclical headwinds driven by macroeconomic and geopolitical instability. Both Joby and Archer rely heavily on global supply chains for critical battery minerals (lithium, cobalt, nickel) and electronic components. In 2025, surging tariffs and trade protectionism directly compressed expected manufacturing margins.

Furthermore, because eVTOL platforms hold dual-use defense capabilities (as evidenced by Joby’s Agility Prime DOD contracts and Archer’s dual-use drone development with Anduril), they are tightly bound by EAR and ITAR export controls. Joby’s international footprint, including R&D facilities in Shenzhen, China, exposes it to heightened data security scrutiny and intellectual property risks. Any disruption in this fragile supply web could result in stranded assets and idle manufacturing facilities.

HDIN Viewpoint: The Institutional Perspective

At HDIN Research, our analysis indicates that the eVTOL market is entering a phase of "survival of the best-funded." The true strategic moats in this space will not be built on battery density alone, but on legal certainties and infrastructure lock-ins.

Investors must remain highly skeptical of "paper wealth" on these balance sheets. Archer’s $1 billion United Airlines order is strictly a conditional contract liability dependent on FAA certification, while Joby carries significant goodwill impairment risks from its Blade acquisition. Joby currently holds a definitive first-mover advantage in commercialization due to its advanced Phase 4 FAA certification status and airtight legal monopoly in Dubai, making a 2026 commercial launch highly probable. However, Archer’s OEM-centric model provides a superior defense mechanism against certification delays, as it burns less cash maintaining an active flight infrastructure. Ultimately, the victor will be the firm that successfully transitions from a technology pioneer to an unyielding industrial manufacturer without falling victim to the equity dilution spiral.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com