Ophthalmic Sector 2025: Unpacking STAAR Surgical’s Structural Headwinds and the Strategic Moats of Industry Giants

Date : 2026-03-10

Reading : 204

The 2025 financial disclosures of global ophthalmic medical giants reveal a profound divergence in industry resilience. While comprehensive players like Alcon and Carl Zeiss Meditec successfully leveraged their diversified ecosystems to weather macroeconomic volatility, pure-play ICL manufacturer STAAR Surgical faced a severe structural contraction. A 23.7% revenue plunge and negative free cash flow at STAAR underscore a critical industry transition: the era of explosive, single-market growth is giving way to an environment where closed-loop platforms and robust capital management dictate long-term survival.

Based on HDIN Research’s proprietary analysis frameworks, we dissect the underlying financial health, channel strategies, and competitive paradigms defining the implantable lens market in 2025.

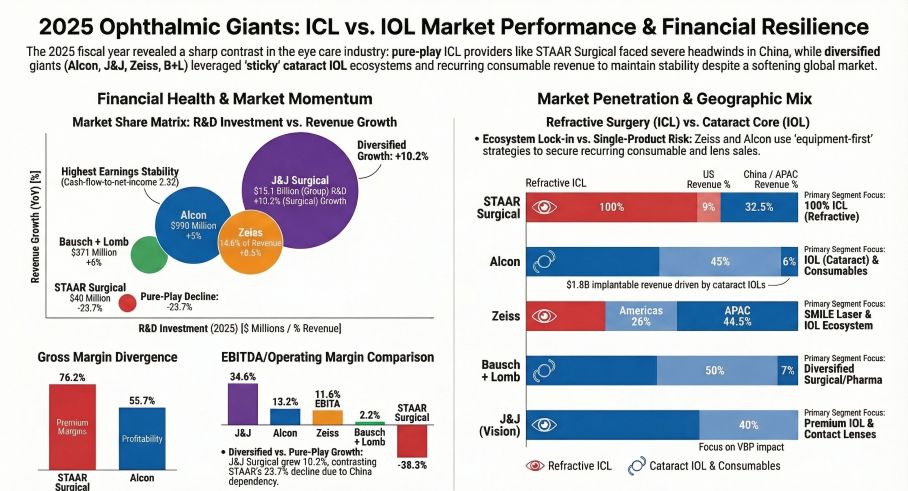

Figure 2025 Ophthalmic Giants: lCL vs. lOL Market Performance & Financial Resilience

Sector Positioning: Single-Product Vulnerability Amid Cyclical Headwinds

Sector Positioning: Single-Product Vulnerability Amid Cyclical Headwinds

In 2025, the refractive surgery market—historically an engine of high-margin growth—collided with severe cyclical headwinds. STAAR Surgical’s performance highlights the acute vulnerability of a single-product, highly concentrated business model.

STAAR’s overexposure to the Chinese market (which previously accounted for a massive share of its revenue) triggered a structural collapse in its marketing efficiency. As consumer spending downgraded and distributors entered a painful destocking phase, STAAR’s Sales, General, and Administrative (SG&A) expenses surged to an unsustainable 114.5% of revenue. In essence, the marginal revenue generated per dollar of marketing spend turned negative. Unlike cataract surgeries, which are driven by aging demographics and represent non-discretionary medical needs, ICL procedures are elective and out-of-pocket, making STAAR’s sector positioning highly susceptible to macroeconomic fluctuations.

Conversely, comprehensive giants demonstrated remarkable defensive capabilities. Johnson & Johnson’s Surgical Vision unit recorded a 10.2% growth, while Alcon maintained flat top-line stability in a soft market. By utilizing non-discretionary cataract operations to subsidize and stabilize their elective refractive portfolios, these market leaders effectively mitigated downside risks.

Financial Health & Capital Allocation Efficiency

A "dehydrated" analysis of earnings quality exposes stark contrasts in capital allocation efficiency and cash flow generation across the top five ophthalmic players.

STAAR Surgical reported an $80.4 million net loss, accompanied by a negative Free Cash Flow (FCF) of -$40 million. A deeper forensic look reveals significant distress in working capital, exacerbated by $55.5 million in bloated inventory and erratic Days Sales Outstanding (DSO) metrics. The sharp drop in DSO from 145 days in 2024 to 85 days in 2025 masks a strategic delay in Chinese shipment revenue recognition—a maneuver that artificially inflated gross margins while failing to conceal underlying operational "bleeding." Furthermore, a pivot from aggressive expansion to maintenance CapEx indicates looming depreciation pressures from its Swiss manufacturing facility.

In stark contrast, Alcon emerged as the industry benchmark for earnings purity. With an Operating Cash Flow to Net Income (OCF/NI) ratio of 2.32, Alcon generates profound cash liquidity. Its surgical consumables segment, functioning as a high-margin cash cow, funds an aggressive $990 million R&D budget while simultaneously supporting shareholder returns through a $750 million stock buyback program. Carl Zeiss Meditec mirrored this stability, with a 1.47 OCF/NI ratio, reflecting a disciplined capital approach despite the interest burden from its DORC acquisition.

Strategic Moats: Ecosystem Synergy vs. Material Exclusivity

The competitive landscape of 2025 is fundamentally a battle of strategic moats.

STAAR Surgical’s primary defense remains its proprietary Collamer biocompatible material and its deep clinical training network (EVO Experience Centers). While this material exclusivity secures high gross margins (76.2%), it lacks cross-segment synergy.

Meanwhile, Alcon and Zeiss have successfully constructed formidable "One-Stop Shop" ecosystems. Their moat lies in equipment lock-in. Alcon’s Centurion and Unity VCS systems, alongside Zeiss’s SMILE and VISUMAX 800 platforms, dictate the surgical workflow. Once a clinic installs these capital-intensive platforms (which operate on a 7-to-10-year replacement cycle), the switching costs become prohibitive. This ecosystem synergy guarantees a continuous, recurring revenue stream from high-margin consumables, which now accounts for over 50% of Alcon and Zeiss's surgical divisions.

HDIN Viewpoint

HDIN Research believes that the valuation premium in the ophthalmic medical device sector has permanently shifted from volatile, single-product disruptors to diversified, platform-driven incumbents. STAAR Surgical is currently navigating the "hard landing" of its post-pandemic boom. To regain investor confidence, management must urgently address the 32.2% employee turnover rate threatening its clinic relationships, clear channel inventory in China, and accelerate the commercialization of its next-generation presbyopia lenses.

For institutional investors, the definitive takeaway from 2025 is clear: the ability to generate pure, consumable-driven cash flow—immunized against VBP (Volume-Based Procurement) pricing pressures and consumer cyclicality—is the ultimate indicator of a resilient enterprise. As digitalization reshapes clinical workflows, the companies dominating the operating room ecosystem will capture the lion's share of future profitability.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on HDIN Research’s proprietary analysis frameworks, we dissect the underlying financial health, channel strategies, and competitive paradigms defining the implantable lens market in 2025.

Figure 2025 Ophthalmic Giants: lCL vs. lOL Market Performance & Financial Resilience

Sector Positioning: Single-Product Vulnerability Amid Cyclical HeadwindsIn 2025, the refractive surgery market—historically an engine of high-margin growth—collided with severe cyclical headwinds. STAAR Surgical’s performance highlights the acute vulnerability of a single-product, highly concentrated business model.

STAAR’s overexposure to the Chinese market (which previously accounted for a massive share of its revenue) triggered a structural collapse in its marketing efficiency. As consumer spending downgraded and distributors entered a painful destocking phase, STAAR’s Sales, General, and Administrative (SG&A) expenses surged to an unsustainable 114.5% of revenue. In essence, the marginal revenue generated per dollar of marketing spend turned negative. Unlike cataract surgeries, which are driven by aging demographics and represent non-discretionary medical needs, ICL procedures are elective and out-of-pocket, making STAAR’s sector positioning highly susceptible to macroeconomic fluctuations.

Conversely, comprehensive giants demonstrated remarkable defensive capabilities. Johnson & Johnson’s Surgical Vision unit recorded a 10.2% growth, while Alcon maintained flat top-line stability in a soft market. By utilizing non-discretionary cataract operations to subsidize and stabilize their elective refractive portfolios, these market leaders effectively mitigated downside risks.

Financial Health & Capital Allocation Efficiency

A "dehydrated" analysis of earnings quality exposes stark contrasts in capital allocation efficiency and cash flow generation across the top five ophthalmic players.

STAAR Surgical reported an $80.4 million net loss, accompanied by a negative Free Cash Flow (FCF) of -$40 million. A deeper forensic look reveals significant distress in working capital, exacerbated by $55.5 million in bloated inventory and erratic Days Sales Outstanding (DSO) metrics. The sharp drop in DSO from 145 days in 2024 to 85 days in 2025 masks a strategic delay in Chinese shipment revenue recognition—a maneuver that artificially inflated gross margins while failing to conceal underlying operational "bleeding." Furthermore, a pivot from aggressive expansion to maintenance CapEx indicates looming depreciation pressures from its Swiss manufacturing facility.

In stark contrast, Alcon emerged as the industry benchmark for earnings purity. With an Operating Cash Flow to Net Income (OCF/NI) ratio of 2.32, Alcon generates profound cash liquidity. Its surgical consumables segment, functioning as a high-margin cash cow, funds an aggressive $990 million R&D budget while simultaneously supporting shareholder returns through a $750 million stock buyback program. Carl Zeiss Meditec mirrored this stability, with a 1.47 OCF/NI ratio, reflecting a disciplined capital approach despite the interest burden from its DORC acquisition.

Strategic Moats: Ecosystem Synergy vs. Material Exclusivity

The competitive landscape of 2025 is fundamentally a battle of strategic moats.

STAAR Surgical’s primary defense remains its proprietary Collamer biocompatible material and its deep clinical training network (EVO Experience Centers). While this material exclusivity secures high gross margins (76.2%), it lacks cross-segment synergy.

Meanwhile, Alcon and Zeiss have successfully constructed formidable "One-Stop Shop" ecosystems. Their moat lies in equipment lock-in. Alcon’s Centurion and Unity VCS systems, alongside Zeiss’s SMILE and VISUMAX 800 platforms, dictate the surgical workflow. Once a clinic installs these capital-intensive platforms (which operate on a 7-to-10-year replacement cycle), the switching costs become prohibitive. This ecosystem synergy guarantees a continuous, recurring revenue stream from high-margin consumables, which now accounts for over 50% of Alcon and Zeiss's surgical divisions.

HDIN Viewpoint

HDIN Research believes that the valuation premium in the ophthalmic medical device sector has permanently shifted from volatile, single-product disruptors to diversified, platform-driven incumbents. STAAR Surgical is currently navigating the "hard landing" of its post-pandemic boom. To regain investor confidence, management must urgently address the 32.2% employee turnover rate threatening its clinic relationships, clear channel inventory in China, and accelerate the commercialization of its next-generation presbyopia lenses.

For institutional investors, the definitive takeaway from 2025 is clear: the ability to generate pure, consumable-driven cash flow—immunized against VBP (Volume-Based Procurement) pricing pressures and consumer cyclicality—is the ultimate indicator of a resilient enterprise. As digitalization reshapes clinical workflows, the companies dominating the operating room ecosystem will capture the lion's share of future profitability.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com