Roland Corporation FY25 Analysis: Navigating Cyclical Headwinds and Forging Digital Strategic Moats

Date : 2026-03-10

Reading : 113

Roland Corporation’s fiscal 2025 results mark a critical inflection point. While top-line revenue edged up 1.5% year-over-year to $674.95 million, the underlying narrative is not one of mere stagnation, but of aggressive restructuring. A significant non-recurring impairment masks a highly resilient operational core, as the company pivots from a traditional hardware manufacturer into a high-margin, digital music experience provider. HDIN Research’s deep-dive analysis reveals that operational efficiency and ecosystem expansion, rather than unit volume, are the true drivers of Roland’s future sector positioning.

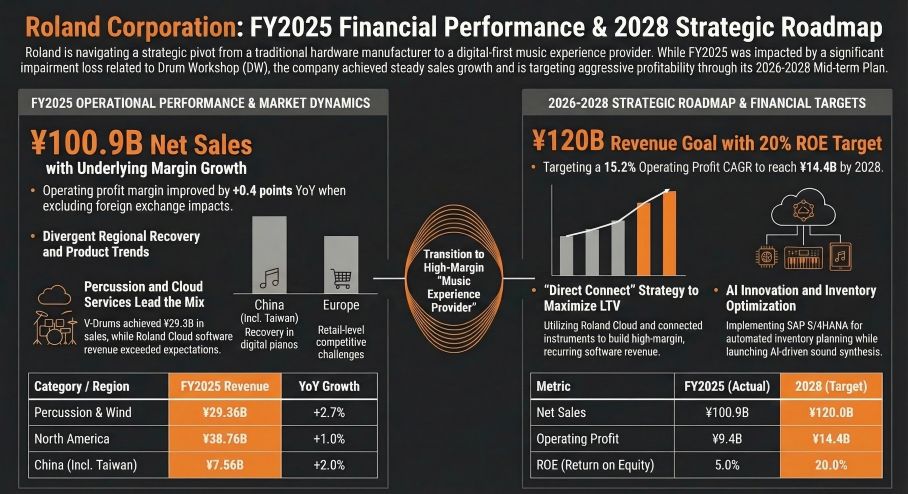

Figure Roland Corporation: FY2025 Financial Performance & 2028 Strategic Roadmap

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

On the surface, Roland’s net profit plummeted by 63.7% to $14.5 million in FY25. However, this contraction was primarily driven by a $25.81 million non-recurring impairment on goodwill and fixed assets related to its 2022 acquisition of the U.S. drum brand, Drum Workshop (DW). This "Big Bath" accounting maneuver effectively clears the balance sheet of legacy M&A synergy shortfalls, allowing the company to enter its 2026-2028 strategic cycle unencumbered.

Beneath the statutory profit drop, Roland’s capital allocation efficiency remains robust. Operating Cash Flow (OCF) surged by 16.9% to $91.59 million. This strong internal cash generation easily covered the company's $36.36 million R&D expenditure (a 2.5x coverage ratio) and sustained a solid dividend payout. Furthermore, Roland’s SG&A efficiency is exceptionally stable: for every additional dollar spent on sales and administrative expenses in FY25, the company generated $2.48 in marginal revenue, underscoring the success of its Direct-to-Professional (DTP) channel strategy.

Supply Chain Realignment & Operational Efficiency

Facing cyclical headwinds from post-pandemic demand saturation—particularly in the ProAV segment, which saw a 4.4% revenue decline—and geopolitical tariff pressures, Roland demonstrated remarkable supply chain agility. The company accelerated the migration of critical production lines from its Suzhou, China facility to its primary manufacturing hub in Malaysia to circumvent U.S. reciprocal tariffs.

Coupled with a stringent "Zero-base cost review," this geographic repositioning largely neutralized inflation and tariff impacts, keeping gross margins relatively stable at 42.2%. Simultaneously, Roland’s digital transformation of its supply chain, anchored by a new SAP S/4HANA system, automated demand forecasting and optimized inventory turnover to 2.06 times. This lean operational framework significantly mitigated excess inventory risks and bolstered free cash flow.

Strategic Moats & The 2028 Industry Outlook

Looking ahead to the 2026-2028 medium-term management plan, Roland is aggressively repositioning its strategic moats. The company is targeting $802 million in revenue and a highly ambitious 20% Return on Equity (ROE) by 2028. This growth is anchored in three foundational pillars:

1. The "Direct Connect" Ecosystem: Roland is transitioning from one-off hardware sales to a recurring revenue model driven by Customer Lifetime Value (LTV). By embedding Wi-Fi as a standard feature across instruments (like the robustly growing V-Drums series) and linking them to the Roland Cloud, the company is locking users into a high-margin software and subscription ecosystem.

2. AI and Continuous Innovation: With the completion of the "Roland Inspiration Hub" and the establishment of the Roland Future Design Lab, capital expenditure is being funneled into integrating Artificial Intelligence into music creation, ensuring long-term product differentiation.

3. Emerging Market Penetration: While North America remains the primary profit pool (38.4% of revenue), Roland is strategically targeting the expanding "hobbyist" and educational markets in China, India, and Latin America to capture demographic dividends.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Roland’s FY25 performance as a necessary consolidation phase. While the DW acquisition impairment underscores the risks of miscalculated M&A synergies, the company’s core cash-generating engine remains highly dependable.

However, achieving the aggressive 20% ROE target by 2028 will require flawless execution. Roland must rapidly scale its asset-light software services (Roland Cloud) to offset the cyclicality of its hardware divisions. Investors and industry stakeholders should closely monitor Roland's ability to navigate ongoing geopolitical supply chain vulnerabilities in Asia, as well as its capacity to translate its impressive R&D pipeline into sticky, high-LTV digital subscriptions. Ultimately, Roland's transition from a legacy instrument vendor to an integrated digital platform will dictate its leadership premium in the coming decade.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Roland Corporation: FY2025 Financial Performance & 2028 Strategic Roadmap

Financial Health & Capital Allocation EfficiencyOn the surface, Roland’s net profit plummeted by 63.7% to $14.5 million in FY25. However, this contraction was primarily driven by a $25.81 million non-recurring impairment on goodwill and fixed assets related to its 2022 acquisition of the U.S. drum brand, Drum Workshop (DW). This "Big Bath" accounting maneuver effectively clears the balance sheet of legacy M&A synergy shortfalls, allowing the company to enter its 2026-2028 strategic cycle unencumbered.

Beneath the statutory profit drop, Roland’s capital allocation efficiency remains robust. Operating Cash Flow (OCF) surged by 16.9% to $91.59 million. This strong internal cash generation easily covered the company's $36.36 million R&D expenditure (a 2.5x coverage ratio) and sustained a solid dividend payout. Furthermore, Roland’s SG&A efficiency is exceptionally stable: for every additional dollar spent on sales and administrative expenses in FY25, the company generated $2.48 in marginal revenue, underscoring the success of its Direct-to-Professional (DTP) channel strategy.

Supply Chain Realignment & Operational Efficiency

Facing cyclical headwinds from post-pandemic demand saturation—particularly in the ProAV segment, which saw a 4.4% revenue decline—and geopolitical tariff pressures, Roland demonstrated remarkable supply chain agility. The company accelerated the migration of critical production lines from its Suzhou, China facility to its primary manufacturing hub in Malaysia to circumvent U.S. reciprocal tariffs.

Coupled with a stringent "Zero-base cost review," this geographic repositioning largely neutralized inflation and tariff impacts, keeping gross margins relatively stable at 42.2%. Simultaneously, Roland’s digital transformation of its supply chain, anchored by a new SAP S/4HANA system, automated demand forecasting and optimized inventory turnover to 2.06 times. This lean operational framework significantly mitigated excess inventory risks and bolstered free cash flow.

Strategic Moats & The 2028 Industry Outlook

Looking ahead to the 2026-2028 medium-term management plan, Roland is aggressively repositioning its strategic moats. The company is targeting $802 million in revenue and a highly ambitious 20% Return on Equity (ROE) by 2028. This growth is anchored in three foundational pillars:

1. The "Direct Connect" Ecosystem: Roland is transitioning from one-off hardware sales to a recurring revenue model driven by Customer Lifetime Value (LTV). By embedding Wi-Fi as a standard feature across instruments (like the robustly growing V-Drums series) and linking them to the Roland Cloud, the company is locking users into a high-margin software and subscription ecosystem.

2. AI and Continuous Innovation: With the completion of the "Roland Inspiration Hub" and the establishment of the Roland Future Design Lab, capital expenditure is being funneled into integrating Artificial Intelligence into music creation, ensuring long-term product differentiation.

3. Emerging Market Penetration: While North America remains the primary profit pool (38.4% of revenue), Roland is strategically targeting the expanding "hobbyist" and educational markets in China, India, and Latin America to capture demographic dividends.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Roland’s FY25 performance as a necessary consolidation phase. While the DW acquisition impairment underscores the risks of miscalculated M&A synergies, the company’s core cash-generating engine remains highly dependable.

However, achieving the aggressive 20% ROE target by 2028 will require flawless execution. Roland must rapidly scale its asset-light software services (Roland Cloud) to offset the cyclicality of its hardware divisions. Investors and industry stakeholders should closely monitor Roland's ability to navigate ongoing geopolitical supply chain vulnerabilities in Asia, as well as its capacity to translate its impressive R&D pipeline into sticky, high-LTV digital subscriptions. Ultimately, Roland's transition from a legacy instrument vendor to an integrated digital platform will dictate its leadership premium in the coming decade.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com