MDA Space 2025 Strategic Analysis: The Pivot from Bespoke Engineering to Industrialized Scale

Date : 2026-03-10

Reading : 488

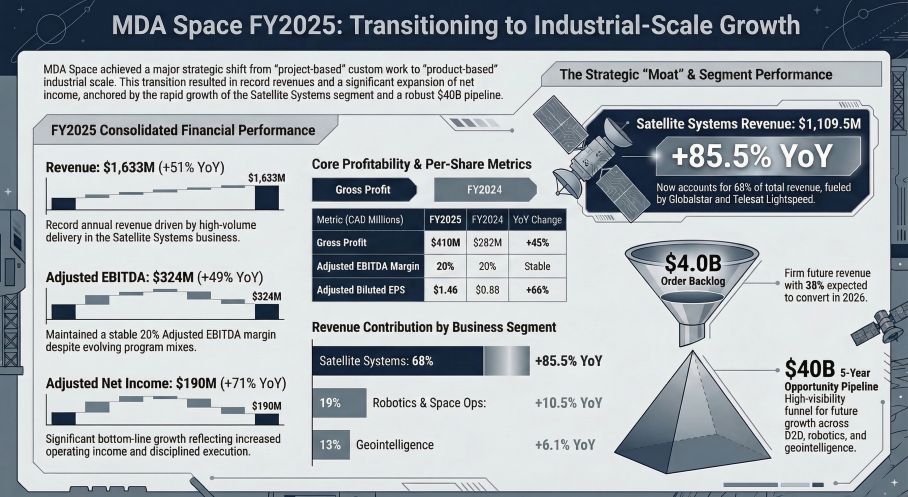

In 2025, MDA Space executed a definitive structural shift from a traditional provider of bespoke space engineering to a globally integrated industrial platform. The company reported a record-breaking revenue of $1.169 billion (USD), representing a 51% year-over-year surge. However, the raw numbers merely reflect a deeper strategic reality: MDA Space has successfully operationalized the "mass production" of low-Earth orbit (LEO) infrastructure, effectively creating a manufacturing moat in a sector previously dominated by high-cost, low-volume fabrication.

Figure MDA Space FY2025: Transitioning to Industrial-Scale Growth

The Industrialization of Satellite Systems

The Industrialization of Satellite Systems

The most significant driver of this expansion was the Satellite Systems segment, which grew by 85.5% and now accounts for 68% of total revenue. This growth is not cyclical but structural, driven by the execution of major LEO constellation contracts for Telesat Lightspeed and Globalstar.

The strategic implication here is the successful deployment of Industry 5.0 manufacturing capabilities. With the completion of the 185,000-square-foot Montreal facility, MDA Space has established a production cadence capable of delivering two satellites per day. This shifts the company's value proposition from "engineering excellence" to "speed-to-market and unit-cost efficiency." Furthermore, the acquisition of SatixFy’s digital payload division has secured a vertical integration advantage, allowing MDA to control the supply chain for critical radiation-hardened ASIC chips—a key differentiator in the burgeoning Direct-to-Device (D2D) market.

Expanding the Defense Perimeter: 49North and C4ISR

While commercial space drives volume, sovereign security drives margin resilience. In early 2026, MDA launched 49North, a strategic brand designed to penetrate the non-space C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) market.

This move signals an intent to capture the full data value chain. By integrating Geointelligence assets (such as the CHORUS™ constellation and dark vessel detection) directly into tactical ground operations, MDA is positioning itself not just as a data provider, but as a mission-critical partner for Canadian and Allied Arctic sovereignty. The Polar Enhanced Satellite Communication Project (ESCP-P) exemplifies this, merging secure military communications with high-latitude strategic dominance.

Robotics: Monetizing Autonomy in Deep Space

The Robotics & Space Operations segment (19% of revenue) continues to provide a stable, high-margin foundation. The transition of Canadarm3 into Phase C/D for the NASA-led Gateway station secures long-term visibility.

More importantly, MDA has successfully productized this government-funded IP into the SKYMAKER™ commercial platform. By securing contracts for commercial space stations like Starlab, MDA is effectively diversifying its revenue mix, reducing reliance on government cycles while capitalizing on the emerging orbital servicing, assembly, and manufacturing (ISAM) market.

HDIN Viewpoint: The Capital Allocation Paradox

At HDIN Research, we maintain a constructive but scrutinized outlook on MDA Space’s capital allocation strategy. While the top-line growth is robust, the company faces a "growth paradox" common in rapidly scaling industrial sectors.

1. Cash Flow Compression: Free Cash Flow (FCF) contracted significantly to $118 million in 2025. This is a direct result of aggressive capital deployment ($208 million in CapEx) required to stand up the Montreal manufacturing capabilities. Investors must view this not as operational inefficiency, but as the necessary "toll" to enter the volume-manufacturing arena.

2. Accounting Risks: We note a rise in unbilled receivables ($134 million). Given the reliance on percentage-of-completion accounting for fixed-price contracts, this metric warrants close monitoring. It implies that revenue recognition is outpacing cash collection—a standard feature of ramping production, but a risk factor if supply chain bottlenecks (such as those seen in the Globalstar program) delay milestone payments.

3. Valuation Logic: The 9% decrease in backlog is a mathematical inevitability of faster conversion rates. The market should no longer value MDA based solely on its order book size, but on its book-to-bill velocity and its ability to secure recurring revenue tails (via 15-year support contracts) that follow the hardware delivery.

Conclusion: MDA Space has built a formidable defensive moat through vertical integration and sovereign alignment. The challenge for 2026 will be managing working capital efficiency as they ramp up production to meet the demands of the industrialized space economy.

Download & Media Access:

Presentation Download

To review the full financial data and strategic breakdown discussed in this article, please [Click the PDF download link under “Related Topics” to access the presentation of this report.]

Video Analysis

For a visual summary of MDA Space’s operational pivot and market positioning, Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure MDA Space FY2025: Transitioning to Industrial-Scale Growth

The Industrialization of Satellite SystemsThe most significant driver of this expansion was the Satellite Systems segment, which grew by 85.5% and now accounts for 68% of total revenue. This growth is not cyclical but structural, driven by the execution of major LEO constellation contracts for Telesat Lightspeed and Globalstar.

The strategic implication here is the successful deployment of Industry 5.0 manufacturing capabilities. With the completion of the 185,000-square-foot Montreal facility, MDA Space has established a production cadence capable of delivering two satellites per day. This shifts the company's value proposition from "engineering excellence" to "speed-to-market and unit-cost efficiency." Furthermore, the acquisition of SatixFy’s digital payload division has secured a vertical integration advantage, allowing MDA to control the supply chain for critical radiation-hardened ASIC chips—a key differentiator in the burgeoning Direct-to-Device (D2D) market.

Expanding the Defense Perimeter: 49North and C4ISR

While commercial space drives volume, sovereign security drives margin resilience. In early 2026, MDA launched 49North, a strategic brand designed to penetrate the non-space C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) market.

This move signals an intent to capture the full data value chain. By integrating Geointelligence assets (such as the CHORUS™ constellation and dark vessel detection) directly into tactical ground operations, MDA is positioning itself not just as a data provider, but as a mission-critical partner for Canadian and Allied Arctic sovereignty. The Polar Enhanced Satellite Communication Project (ESCP-P) exemplifies this, merging secure military communications with high-latitude strategic dominance.

Robotics: Monetizing Autonomy in Deep Space

The Robotics & Space Operations segment (19% of revenue) continues to provide a stable, high-margin foundation. The transition of Canadarm3 into Phase C/D for the NASA-led Gateway station secures long-term visibility.

More importantly, MDA has successfully productized this government-funded IP into the SKYMAKER™ commercial platform. By securing contracts for commercial space stations like Starlab, MDA is effectively diversifying its revenue mix, reducing reliance on government cycles while capitalizing on the emerging orbital servicing, assembly, and manufacturing (ISAM) market.

HDIN Viewpoint: The Capital Allocation Paradox

At HDIN Research, we maintain a constructive but scrutinized outlook on MDA Space’s capital allocation strategy. While the top-line growth is robust, the company faces a "growth paradox" common in rapidly scaling industrial sectors.

1. Cash Flow Compression: Free Cash Flow (FCF) contracted significantly to $118 million in 2025. This is a direct result of aggressive capital deployment ($208 million in CapEx) required to stand up the Montreal manufacturing capabilities. Investors must view this not as operational inefficiency, but as the necessary "toll" to enter the volume-manufacturing arena.

2. Accounting Risks: We note a rise in unbilled receivables ($134 million). Given the reliance on percentage-of-completion accounting for fixed-price contracts, this metric warrants close monitoring. It implies that revenue recognition is outpacing cash collection—a standard feature of ramping production, but a risk factor if supply chain bottlenecks (such as those seen in the Globalstar program) delay milestone payments.

3. Valuation Logic: The 9% decrease in backlog is a mathematical inevitability of faster conversion rates. The market should no longer value MDA based solely on its order book size, but on its book-to-bill velocity and its ability to secure recurring revenue tails (via 15-year support contracts) that follow the hardware delivery.

Conclusion: MDA Space has built a formidable defensive moat through vertical integration and sovereign alignment. The challenge for 2026 will be managing working capital efficiency as they ramp up production to meet the demands of the industrialized space economy.

Download & Media Access:

Presentation Download

To review the full financial data and strategic breakdown discussed in this article, please [Click the PDF download link under “Related Topics” to access the presentation of this report.]

Video Analysis

For a visual summary of MDA Space’s operational pivot and market positioning, Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com