NeuroPace FY2025 Analysis: The $100M Inflection Point & 2026 Outlook

Date : 2026-03-10

Reading : 140

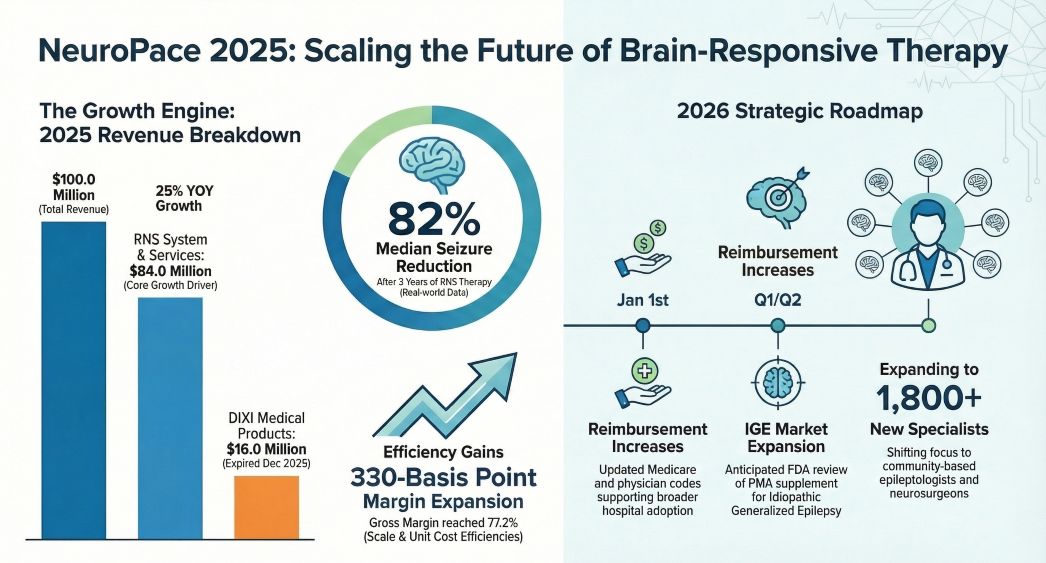

In Fiscal Year 2025, NeuroPace, Inc. achieved a critical commercial milestone, surpassing $100 million in annual revenue (+25.1% YoY) while significantly expanding gross margins to 77.2%. However, the headline growth masks a pivotal strategic shift: the termination of the DIXI Medical distribution agreement. As HDIN Research analyzes below, 2026 will be a definitive year where the company must prove that the organic adoption of its proprietary RNS® System can bridge the 16% revenue gap left by the exited distribution business, all while navigating strict debt covenants.

Figure NeuroPace 2025: Scaling the Future of Brain-Responsive Therapy

Operational Leverage and Capital Efficiency

Operational Leverage and Capital Efficiency

The "So What" behind the 2025 financials is not just top-line growth, but the emergence of genuine operational leverage. The expansion of gross margin by 330 basis points (to 77.2%) indicates that NeuroPace is benefiting from economies of scale, effectively diluting fixed production costs as volume increases.

Furthermore, the company has executed a sophisticated restructuring of its capital stack. By replacing high-interest CRG debt (13.5%) with a SOFR+5.5% facility from MidCap, and raising nearly $70 million in equity to optimize its shareholder base, NeuroPace has extended its cash runway to an estimated 5+ years. This liquidity is crucial, as it provides the buffer needed to absorb the net loss of $21.5 million while the company aggressively invests in R&D for indication expansion.

The Strategic Moat: From Hardware to Data Intelligence

NeuroPace is transitioning its value proposition from a pure-play device manufacturer to a data-driven diagnostic platform. With a cumulative implanted base of over 8,000 patients, the company now holds a proprietary asset of 22 million iEEG records.

* The AI Pivot: The submission of Seizure ID™ to the FDA marks a logical evolution toward AI-assisted diagnostics, increasing the switching costs for clinicians and deepening the competitive moat against open-loop competitors like Medtronic (DBS) and LivaNova (VNS).

* Channel Expansion: The strategic imperative for 2025-2026 is "channel down" expansion. By moving beyond Level 4 Comprehensive Epilepsy Centers (CECs) to target 1,800 community epilepsy specialists, NeuroPace aims to capture a broader segment of the 575,000 adult drug-resistant epilepsy patients in the U.S.

The 2026 Headwind: The DIXI Gap

Investors must rigorously evaluate the impact of the DIXI Medical agreement termination. In 2025, third-party distribution contributed approximately 16% of total revenue. With this stream reaching zero in 2026, NeuroPace is effectively starting the year with a revenue deficit.

The company’s ability to avoid liquidity triggers depends on the RNS System’s organic growth. Specifically, debt covenants with MidCap require the company to maintain specific revenue thresholds (e.g., $90 million in RNS-specific revenue in 2026) to access favorable liquidity tiers. Failure to accelerate core product sales could tighten financial flexibility at a critical juncture.

HDIN Viewpoint: The "Pure-Play" Premium vs. Execution Risk

At HDIN Research, we view the exit from the DIXI distribution business as a short-term pain for long-term gain. While it creates immediate topline pressure, it purifies NeuroPace’s margin profile and focuses resources on its high-barrier IP—the closed-loop RNS System.

However, our analysts flag a specific Execution Risk: The shift from selling to concentrated academic centers (CECs) to a fragmented network of community providers involves higher customer acquisition costs and longer sales cycles. If the community adoption rate lags, the company may face a dangerous intersection of falling revenue velocity and strict debt covenant constraints in mid-2026.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Video Analysis

Click this link to watch the YouTube video summarizing our key findings on NeuroPace.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure NeuroPace 2025: Scaling the Future of Brain-Responsive Therapy

Operational Leverage and Capital EfficiencyThe "So What" behind the 2025 financials is not just top-line growth, but the emergence of genuine operational leverage. The expansion of gross margin by 330 basis points (to 77.2%) indicates that NeuroPace is benefiting from economies of scale, effectively diluting fixed production costs as volume increases.

Furthermore, the company has executed a sophisticated restructuring of its capital stack. By replacing high-interest CRG debt (13.5%) with a SOFR+5.5% facility from MidCap, and raising nearly $70 million in equity to optimize its shareholder base, NeuroPace has extended its cash runway to an estimated 5+ years. This liquidity is crucial, as it provides the buffer needed to absorb the net loss of $21.5 million while the company aggressively invests in R&D for indication expansion.

The Strategic Moat: From Hardware to Data Intelligence

NeuroPace is transitioning its value proposition from a pure-play device manufacturer to a data-driven diagnostic platform. With a cumulative implanted base of over 8,000 patients, the company now holds a proprietary asset of 22 million iEEG records.

* The AI Pivot: The submission of Seizure ID™ to the FDA marks a logical evolution toward AI-assisted diagnostics, increasing the switching costs for clinicians and deepening the competitive moat against open-loop competitors like Medtronic (DBS) and LivaNova (VNS).

* Channel Expansion: The strategic imperative for 2025-2026 is "channel down" expansion. By moving beyond Level 4 Comprehensive Epilepsy Centers (CECs) to target 1,800 community epilepsy specialists, NeuroPace aims to capture a broader segment of the 575,000 adult drug-resistant epilepsy patients in the U.S.

The 2026 Headwind: The DIXI Gap

Investors must rigorously evaluate the impact of the DIXI Medical agreement termination. In 2025, third-party distribution contributed approximately 16% of total revenue. With this stream reaching zero in 2026, NeuroPace is effectively starting the year with a revenue deficit.

The company’s ability to avoid liquidity triggers depends on the RNS System’s organic growth. Specifically, debt covenants with MidCap require the company to maintain specific revenue thresholds (e.g., $90 million in RNS-specific revenue in 2026) to access favorable liquidity tiers. Failure to accelerate core product sales could tighten financial flexibility at a critical juncture.

HDIN Viewpoint: The "Pure-Play" Premium vs. Execution Risk

At HDIN Research, we view the exit from the DIXI distribution business as a short-term pain for long-term gain. While it creates immediate topline pressure, it purifies NeuroPace’s margin profile and focuses resources on its high-barrier IP—the closed-loop RNS System.

However, our analysts flag a specific Execution Risk: The shift from selling to concentrated academic centers (CECs) to a fragmented network of community providers involves higher customer acquisition costs and longer sales cycles. If the community adoption rate lags, the company may face a dangerous intersection of falling revenue velocity and strict debt covenant constraints in mid-2026.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Video Analysis

Click this link to watch the YouTube video summarizing our key findings on NeuroPace.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com