Nokia and ZTE 2025 Financial Insights: Navigating the AI Supercycle and Structural Divergence

Date : 2026-03-11

Reading : 322

The 2025 fiscal year marked a definitive strategic bifurcation in the global telecommunications equipment market. As cyclical headwinds constrained traditional carrier capital expenditures (CAPEX), industry leaders radically repositioned their portfolios to capture the "AI Supercycle." According to HDIN Research's latest fundamental analysis, Nokia and ZTE are executing diametrically opposed survival strategies. While Nokia leveraged aggressive inorganic expansion and patent monetization to establish a highly profitable AI infrastructure moat in the West, ZTE anchored itself on a volume-driven, domestic compute and server expansion. For institutional investors, the narrative is no longer about 5G base station parity, but rather the stark contrast in capital allocation efficiency and cash flow resilience.

Financial Health: Cash Conversion vs. Volume Expansion

In 2025, the underlying quality of earnings between the two telecom giants diverged significantly, reflecting different structural priorities.

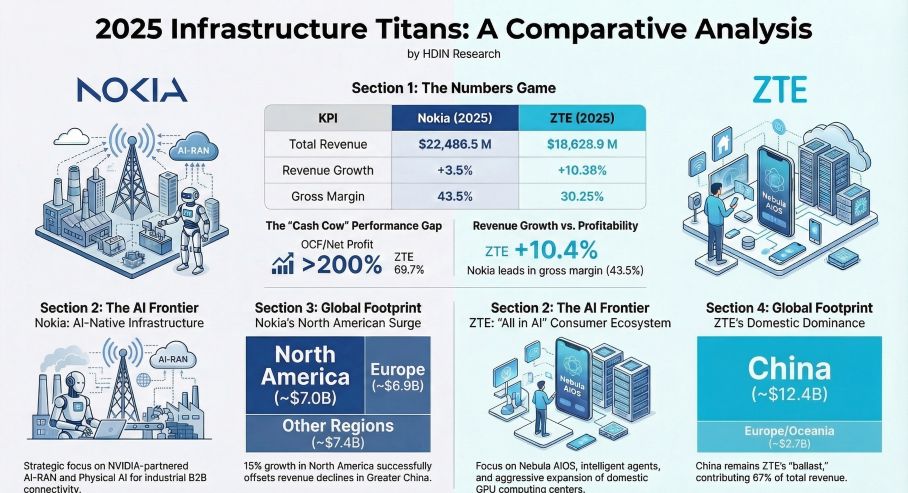

Nokia demonstrated robust operational resilience. While net profit optically declined by 48.6% to $746.2 million—largely a base-effect distortion stemming from 2024's retroactive patent payments and the TD Tech divestment—top-line revenue grew 3.5% to $22.48 billion. More importantly, Nokia maintained a formidable capital allocation efficiency, generating over $1.65 billion in Free Cash Flow (FCF). This high cash conversion rate (>200% of net profit) comfortably funded $7.05 million in stock buybacks and sustained dividend distributions, cementing its status as a reliable yield play.

Conversely, ZTE achieved a double-digit revenue surge of 10.38%, propelled by a massive 100.49% growth in its domestic enterprise and compute server business. However, this growth came at a steep cost to profitability. By adopting an aggressive pricing strategy to capture market share in China’s digital transformation build-out, ZTE's enterprise margin hovered at a low 10.97%. Furthermore, its Operating Cash Flow (OCF) dropped by nearly 65.86% year-over-year, indicating that ZTE's top-line expansion is currently trading margin and cash liquidity for raw scale.

Strategic Pivots: The Infinera Acquisition and AI-RAN

The most critical takeaway from 2025 is the transition from "connecting people" to "connecting intelligence."

Nokia executed a masterclass in portfolio restructuring by simplifying into two core segments: Network Infrastructure (NI) and Mobile Infrastructure (MI). The $2.8 billion acquisition of optical networking leader Infinera was the linchpin of this pivot. This strategic moat allowed Nokia to vertically integrate its supply chain with proprietary Indium Phosphide (InP) wafer fabs, successfully capturing surging 800G optical pluggable demand from North American hyperscalers. Consequently, North American revenues spiked by 15%, effectively hedging against a 19% revenue contraction in Greater China. Furthermore, Nokia’s $1 billion strategic partnership with NVIDIA to co-develop GPU-accelerated AI-RAN platforms positions the company at the vanguard of the 6G and AI-native network standards.

ZTE, facing international export controls and geopolitical headwinds, pivoted inward. The company doubled down on a "Connectivity + Compute" framework, heavily participating in China’s "East Data West Compute" initiative. By rolling out AI-enabled smartphones (such as the Nebula AIOS-powered Nubia series) and cloud PCs, ZTE is attempting to build an end-to-end AI ecosystem—from backend server compute to front-end consumer terminals.

HDIN Viewpoint: Sector Positioning and Latent Risks

From the perspective of HDIN Research, Nokia currently holds the superior defensive posture against telecom cyclical headwinds. Nokia’s ultimate strategic moat is its Technologies division; operating at a staggering 70.6% margin, this patent licensing segment provides a non-CAPEX-sensitive cash cow that funds high-risk R&D and M&A activities.

However, investors must exercise strict financial prudence regarding Nokia's balance sheet. The Infinera acquisition generated approximately $940 million in goodwill. Given that the Infinera unit operated at a loss during its initial consolidation phase in 2025, any failure to realize AI-driven hyperscaler synergies by 2026 could trigger severe goodwill impairment risks.

ZTE, while demonstrating impressive agility in penetrating the domestic AI server market, faces a structural profitability ceiling. Its heavy reliance on capital-intensive, low-margin hardware integration leaves its balance sheet highly sensitive to extended accounts receivable cycles and domestic pricing wars.

Ultimately, 2026 will serve as the crucible for both firms. Nokia must prove that its expensive Western AI-infrastructure acquisitions can generate organic margin accretion, while ZTE must demonstrate that its domestic compute volume can eventually translate into sustainable, high-quality cash flows.

Figure 2025 Infrastructure Titans: A Comparative Analysis

Presentation Download

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Watch the Video Analysis

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Financial Health: Cash Conversion vs. Volume Expansion

In 2025, the underlying quality of earnings between the two telecom giants diverged significantly, reflecting different structural priorities.

Nokia demonstrated robust operational resilience. While net profit optically declined by 48.6% to $746.2 million—largely a base-effect distortion stemming from 2024's retroactive patent payments and the TD Tech divestment—top-line revenue grew 3.5% to $22.48 billion. More importantly, Nokia maintained a formidable capital allocation efficiency, generating over $1.65 billion in Free Cash Flow (FCF). This high cash conversion rate (>200% of net profit) comfortably funded $7.05 million in stock buybacks and sustained dividend distributions, cementing its status as a reliable yield play.

Conversely, ZTE achieved a double-digit revenue surge of 10.38%, propelled by a massive 100.49% growth in its domestic enterprise and compute server business. However, this growth came at a steep cost to profitability. By adopting an aggressive pricing strategy to capture market share in China’s digital transformation build-out, ZTE's enterprise margin hovered at a low 10.97%. Furthermore, its Operating Cash Flow (OCF) dropped by nearly 65.86% year-over-year, indicating that ZTE's top-line expansion is currently trading margin and cash liquidity for raw scale.

Strategic Pivots: The Infinera Acquisition and AI-RAN

The most critical takeaway from 2025 is the transition from "connecting people" to "connecting intelligence."

Nokia executed a masterclass in portfolio restructuring by simplifying into two core segments: Network Infrastructure (NI) and Mobile Infrastructure (MI). The $2.8 billion acquisition of optical networking leader Infinera was the linchpin of this pivot. This strategic moat allowed Nokia to vertically integrate its supply chain with proprietary Indium Phosphide (InP) wafer fabs, successfully capturing surging 800G optical pluggable demand from North American hyperscalers. Consequently, North American revenues spiked by 15%, effectively hedging against a 19% revenue contraction in Greater China. Furthermore, Nokia’s $1 billion strategic partnership with NVIDIA to co-develop GPU-accelerated AI-RAN platforms positions the company at the vanguard of the 6G and AI-native network standards.

ZTE, facing international export controls and geopolitical headwinds, pivoted inward. The company doubled down on a "Connectivity + Compute" framework, heavily participating in China’s "East Data West Compute" initiative. By rolling out AI-enabled smartphones (such as the Nebula AIOS-powered Nubia series) and cloud PCs, ZTE is attempting to build an end-to-end AI ecosystem—from backend server compute to front-end consumer terminals.

HDIN Viewpoint: Sector Positioning and Latent Risks

From the perspective of HDIN Research, Nokia currently holds the superior defensive posture against telecom cyclical headwinds. Nokia’s ultimate strategic moat is its Technologies division; operating at a staggering 70.6% margin, this patent licensing segment provides a non-CAPEX-sensitive cash cow that funds high-risk R&D and M&A activities.

However, investors must exercise strict financial prudence regarding Nokia's balance sheet. The Infinera acquisition generated approximately $940 million in goodwill. Given that the Infinera unit operated at a loss during its initial consolidation phase in 2025, any failure to realize AI-driven hyperscaler synergies by 2026 could trigger severe goodwill impairment risks.

ZTE, while demonstrating impressive agility in penetrating the domestic AI server market, faces a structural profitability ceiling. Its heavy reliance on capital-intensive, low-margin hardware integration leaves its balance sheet highly sensitive to extended accounts receivable cycles and domestic pricing wars.

Ultimately, 2026 will serve as the crucible for both firms. Nokia must prove that its expensive Western AI-infrastructure acquisitions can generate organic margin accretion, while ZTE must demonstrate that its domestic compute volume can eventually translate into sustainable, high-quality cash flows.

Figure 2025 Infrastructure Titans: A Comparative Analysis

Presentation DownloadClick the PDF download link under “Related Topics” to access the presentation of this report.

Watch the Video Analysis

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com