2025 Global Analytical Instruments: Navigating CapEx Headwinds Through Strategic Pivots and Ecosystem Moats

Date : 2026-03-05

Reading : 253

The global analytical instrument sector has reached a structural inflection point in 2025. Facing macroeconomic uncertainties, cyclical capital expenditure (CapEx) headwinds, and shifting geopolitical landscapes, industry titans are systematically abandoning pure-play hardware strategies. According to comprehensive benchmark analysis by HDIN Research, leading players—including Thermo Fisher, Agilent, Mettler-Toledo, Waters, Bruker, and Avantor—are rapidly adopting an “Analytical + X” paradigm. By anchoring their growth in high-margin recurring revenues, aggressive clinical diagnostics M&A, and advanced bioprocessing, these giants are redefining their strategic moats to ensure sustained profitability in a zero-sum market.

Figure 2025 Global Analytical Instrument Resilience, Innovation, and the Shift to Recurring Revenue

Structural Resilience: The “Analytical + X” Paradigm

Structural Resilience: The “Analytical + X” Paradigm

In an environment where pharmaceutical CapEx budgets are constrained by high financing costs and delayed academic funding, hardware sales are increasingly vulnerable. To neutralize this cyclicality, top-tier firms have successfully pivoted toward ecosystem lock-in through consumables, services, and digital platforms.

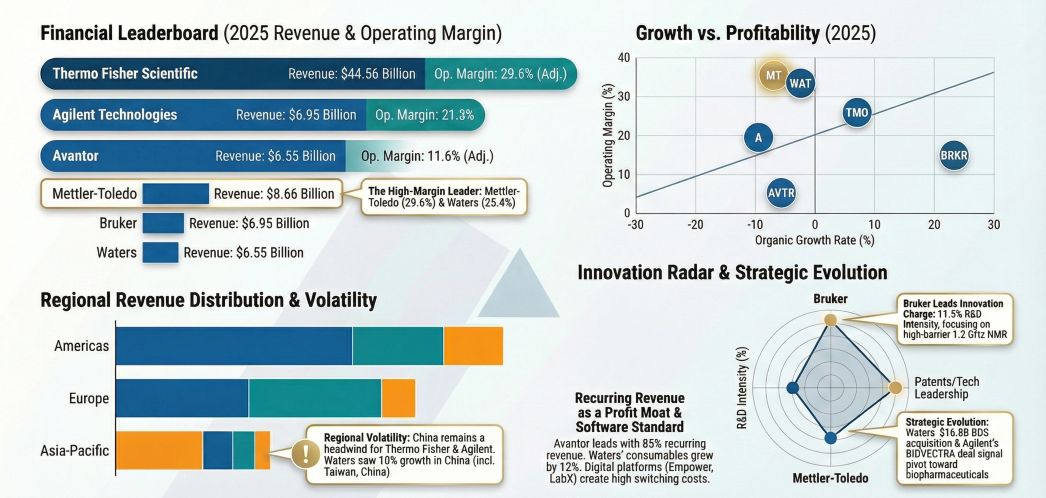

The strategic implication is clear: recurring revenue is no longer just a financial metric; it is the ultimate risk-mitigation tool. Avantor continues to leverage its VWR distribution engine, maintaining a baseline where over 85% of total revenue is recurring. Similarly, Agilent’s CrossLab segment—boasting a 95% non-cyclical revenue profile—acts as an operational stabilizer amidst fluctuating hardware demand. Waters has masterfully executed a “razor-and-blade” strategy, realizing a 12% double-digit surge in chemical consumables, ensuring high client stickiness in QA/QC pharmaceutical laboratories even when new instrument purchases are paused.

Furthermore, the digital transformation of laboratories has created unprecedented switching costs. Proprietary AI-integrated software platforms, such as Agilent’s OpenLab, Waters’ Empower, and Mettler-Toledo’s LabX, have embedded themselves into the rigid compliance workflows of the biopharma industry, virtually eliminating customer churn.

Capital Allocation Efficiency: M&A as a Growth Catalyst

With traditional chromatography and spectroscopy markets approaching maturity, 2025 capital allocation strategies reveal a synchronized, aggressive push into large molecule applications, spatial biology, and therapeutic manufacturing (CDMO).

Instead of organic incrementalism, market leaders are utilizing massive free cash flows for transformative acquisitions to elevate their growth ceilings:

* Waters fundamentally altered its trajectory with a monumental $16.8 billion acquisition of BD’s BDS business, immediately securing a dominant foothold in flow cytometry and clinical molecular diagnostics.

* Thermo Fisher, acting as the industry's ultimate consolidator, is utilizing its robust $6.33 billion free cash flow to expand its end-to-end biopharma value chain, highlighted by the integration of Solventum’s filtration business.

* Agilent is actively crossing the boundary from analysis to therapeutics. Through its $915 million acquisition of BIOVECTRA, Agilent is capturing the high-growth dividends of the CDMO sector, specifically targeting oligonucleotides and peptides.

* Bruker, maintaining an industry-high R&D intensity of 11.5%, has focused its capital on acquiring high-barrier niche innovators (e.g., NanoString, ELITechGroup) to establish first-mover advantages in the spatial biology gold rush.

Navigating Cyclical Headwinds: Tariffs and Geographic Volatility

Sector positioning in 2025 is heavily dictated by a company’s ability to absorb or pass on macroeconomic shocks. Rising global tariffs and domestic procurement policies ("Buy Local") in regions like China have stress-tested global supply chains.

Operational excellence has separated the resilient from the vulnerable. Mettler-Toledo stands out as a benchmark for margin preservation; leveraging its sophisticated "Spinnaker" data-driven pricing initiative, the company effectively neutralized an estimated $50 million tariff hit, sustaining an industry-leading gross margin of 59.4%.

Meanwhile, geographic performance showed stark bifurcation. While some firms faced contraction in China due to delayed government stimulus, Waters defied regional headwinds, delivering a 10% localized growth driven by its deeply entrenched pharmaceutical consumable footprint. To ensure long-term regional compliance, companies like Thermo Fisher and Agilent are accelerating their localized manufacturing footprints to align with shifting domestic supply mandates.

Financial Health & Risk Monitoring

While top-line strategies are evolving, HDIN Research urges institutional investors to monitor hidden balance sheet risks stemming from the current transition phase:

1. Goodwill Impairment Risks: The era of high-premium acquisitions under lower interest rates is maturing. In 2025, Avantor recorded a staggering $785 million non-cash goodwill impairment, while Bruker booked $96.5 million. Investors must scrutinize the cash-flow realization of recent mega-deals.

2. Inventory Overhangs: Proactive supply chain defense against tariffs has led to bloated safety stocks. Waters, for instance, reported $572 million in total inventory, carrying inherent markdown risks if demand recovery lags.

3. DSO and Deferred Revenue: Rising Days Sales Outstanding (DSO) and flattening deferred revenue growth serve as early warning indicators for tightening academic budgets and softening service contract renewals.

HDIN Viewpoint: The Era of High-Quality Operations

HDIN Research assesses that the analytical instrument sector has definitively moved past the era of hardware-driven hyper-growth, entering a phase of "high-quality operations." Valuation premiums over the next 36 months will disproportionately reward companies demonstrating operational leverage, unyielding pricing power, and efficient M&A integration.

Firms like Mettler-Toledo and Waters exemplify defensive operational excellence, while Thermo Fisher and Agilent represent offensive structural repositioning. Moving forward, the true winners will be those who successfully translate their clinical and large-molecule capital deployments into high-margin, recurring cash flow engines.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global Analytical Instrument Resilience, Innovation, and the Shift to Recurring Revenue

Structural Resilience: The “Analytical + X” Paradigm In an environment where pharmaceutical CapEx budgets are constrained by high financing costs and delayed academic funding, hardware sales are increasingly vulnerable. To neutralize this cyclicality, top-tier firms have successfully pivoted toward ecosystem lock-in through consumables, services, and digital platforms.

The strategic implication is clear: recurring revenue is no longer just a financial metric; it is the ultimate risk-mitigation tool. Avantor continues to leverage its VWR distribution engine, maintaining a baseline where over 85% of total revenue is recurring. Similarly, Agilent’s CrossLab segment—boasting a 95% non-cyclical revenue profile—acts as an operational stabilizer amidst fluctuating hardware demand. Waters has masterfully executed a “razor-and-blade” strategy, realizing a 12% double-digit surge in chemical consumables, ensuring high client stickiness in QA/QC pharmaceutical laboratories even when new instrument purchases are paused.

Furthermore, the digital transformation of laboratories has created unprecedented switching costs. Proprietary AI-integrated software platforms, such as Agilent’s OpenLab, Waters’ Empower, and Mettler-Toledo’s LabX, have embedded themselves into the rigid compliance workflows of the biopharma industry, virtually eliminating customer churn.

Capital Allocation Efficiency: M&A as a Growth Catalyst

With traditional chromatography and spectroscopy markets approaching maturity, 2025 capital allocation strategies reveal a synchronized, aggressive push into large molecule applications, spatial biology, and therapeutic manufacturing (CDMO).

Instead of organic incrementalism, market leaders are utilizing massive free cash flows for transformative acquisitions to elevate their growth ceilings:

* Waters fundamentally altered its trajectory with a monumental $16.8 billion acquisition of BD’s BDS business, immediately securing a dominant foothold in flow cytometry and clinical molecular diagnostics.

* Thermo Fisher, acting as the industry's ultimate consolidator, is utilizing its robust $6.33 billion free cash flow to expand its end-to-end biopharma value chain, highlighted by the integration of Solventum’s filtration business.

* Agilent is actively crossing the boundary from analysis to therapeutics. Through its $915 million acquisition of BIOVECTRA, Agilent is capturing the high-growth dividends of the CDMO sector, specifically targeting oligonucleotides and peptides.

* Bruker, maintaining an industry-high R&D intensity of 11.5%, has focused its capital on acquiring high-barrier niche innovators (e.g., NanoString, ELITechGroup) to establish first-mover advantages in the spatial biology gold rush.

Navigating Cyclical Headwinds: Tariffs and Geographic Volatility

Sector positioning in 2025 is heavily dictated by a company’s ability to absorb or pass on macroeconomic shocks. Rising global tariffs and domestic procurement policies ("Buy Local") in regions like China have stress-tested global supply chains.

Operational excellence has separated the resilient from the vulnerable. Mettler-Toledo stands out as a benchmark for margin preservation; leveraging its sophisticated "Spinnaker" data-driven pricing initiative, the company effectively neutralized an estimated $50 million tariff hit, sustaining an industry-leading gross margin of 59.4%.

Meanwhile, geographic performance showed stark bifurcation. While some firms faced contraction in China due to delayed government stimulus, Waters defied regional headwinds, delivering a 10% localized growth driven by its deeply entrenched pharmaceutical consumable footprint. To ensure long-term regional compliance, companies like Thermo Fisher and Agilent are accelerating their localized manufacturing footprints to align with shifting domestic supply mandates.

Financial Health & Risk Monitoring

While top-line strategies are evolving, HDIN Research urges institutional investors to monitor hidden balance sheet risks stemming from the current transition phase:

1. Goodwill Impairment Risks: The era of high-premium acquisitions under lower interest rates is maturing. In 2025, Avantor recorded a staggering $785 million non-cash goodwill impairment, while Bruker booked $96.5 million. Investors must scrutinize the cash-flow realization of recent mega-deals.

2. Inventory Overhangs: Proactive supply chain defense against tariffs has led to bloated safety stocks. Waters, for instance, reported $572 million in total inventory, carrying inherent markdown risks if demand recovery lags.

3. DSO and Deferred Revenue: Rising Days Sales Outstanding (DSO) and flattening deferred revenue growth serve as early warning indicators for tightening academic budgets and softening service contract renewals.

HDIN Viewpoint: The Era of High-Quality Operations

HDIN Research assesses that the analytical instrument sector has definitively moved past the era of hardware-driven hyper-growth, entering a phase of "high-quality operations." Valuation premiums over the next 36 months will disproportionately reward companies demonstrating operational leverage, unyielding pricing power, and efficient M&A integration.

Firms like Mettler-Toledo and Waters exemplify defensive operational excellence, while Thermo Fisher and Agilent represent offensive structural repositioning. Moving forward, the true winners will be those who successfully translate their clinical and large-molecule capital deployments into high-margin, recurring cash flow engines.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com